This note was originally published at 8am on May 10, 2013 for Hedgeye subscribers.

“They might more than ever in the future engage in hunting beavers.”

-Samuel de Champlain

Samuel de Champlain was most definitely a big game hunter. On a basic level, he lived from the period of 1574 – 1635, so he had to hunt big game to eat. On a broader level, he founded the Canadian province of Quebec and was the first person to map the east coast of Canada. Founding and mapping a large part of Canada is most certainly big game hunting.

In the investment world, this was the week of big game hunting. Earlier in the week we had the Ira Sohn Conference, which Keith went through yesterday in the Early Look, and now we have the Salt Conference. And if you aren’t in the hedge fund industry, you probably don’t know what I’m talking about right now!

The Ira Sohn Conference is a charitable conference at which some of the top money managers come and pitch ideas. Meanwhile the Salt Conference is a for profit conference organized by Anthony “Gucci” Scaramucci at which money managers also talk ideas, for the monetary benefit of the organizers (and the casinos in Vegas!). Incidentally, Gucci was the nickname bestowed upon him by President George W. Bush. (When I met President Bush, he called me the much less creative, “Big D”.)

So, what exactly do I mean by big game hunting? Well, in this industry it is when a money manager with some sizeable funds behind him (aka ammo) comes out and pitches a unique investment idea. More often than not the best and most controversial ideas are those on the short side. Over time, markets go up so if you are going to pitch a short idea, you are best off doing your homework.

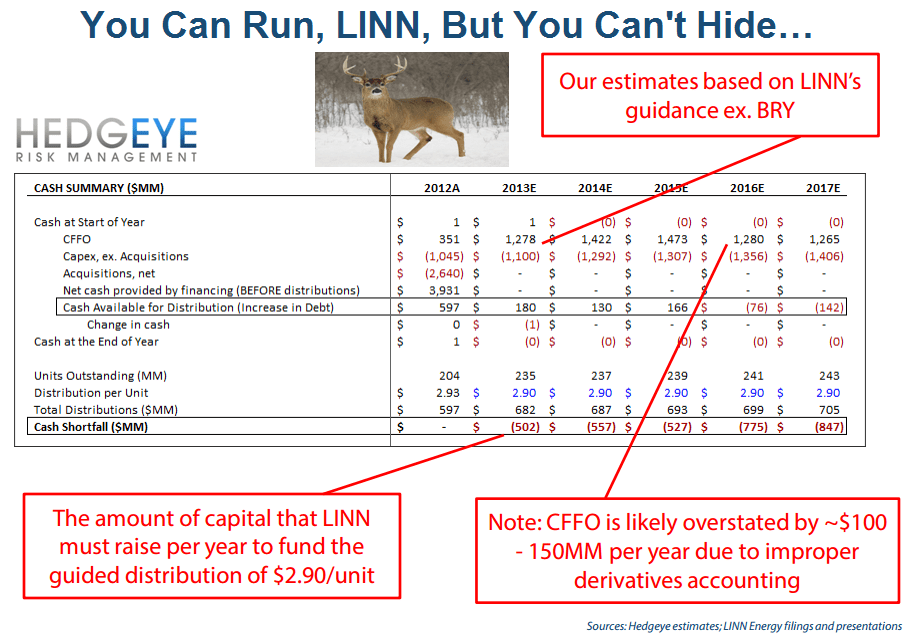

So this morning I’m going to take a break from the global macro grind to talk about a certain big game short idea that we are hunting. This animal goes by the name of LINN Energy and the ticker is $LINE. Our energy analyst Kevin Kaiser has been all over this for the past couple of months and last weekend he gained even more notoriety as his work was highlighted in Barron’s.

The indomitable Jim Cramer then attempted to provide the counter argument to Kaiser by bringing the CEO of Linn on to his nightly show, Mad Money. And it was somewhat apropos from our perspective, as the CEO’s performance in defending himself against our short thesis was a little mad. You can find that video here: http://video.cnbc.com/gallery/?play=1&video=3000166362.

So what was our take on the interview? Overall, we thought Ellis' defenses were weak, which is not a surprise to us (there aren't any good ones). No change in our view here - LNCO/LINE is still one of the best sells/shorts in the energy sector today. In the chart of the day we’ve outlined their cash funding needs and Kaiser’s play-by-play of the Cramer interview is outlined below:

“Jim Cramer: “Are [the bankers advising LINN Energy and Berry Petroleum on the pending merger] saying that [LINE] is worth $18 like Barron’s says?”

Mark Ellis, CEO of LINN Energy: “Absolutely not, Jim. They’ve done a complete independent analysis; we’ve had three different independent analyses done. They are all coming in with valuations in the high 30’s to mid 40’s for the Company. We’ve done our own valuation, it’s in the mid 40’s to as high as $60 per unit depending on how far you go into the 3P reserves.”

Hedgeye: You are citing the fairness opinions of the bankers that are getting paid to work on the merger? Really? We are independent, don’t get paid banking fees from LINN or Berry, and believe that LINE is worth $5 – $18/unit.

Ellis: “Our accounting is in strict adherence to GAAP measures.”

Hedgeye: We agree.

Ellis: “We’ve been very clear and transparent as it relates to our non-GAAP measures that we use to measure the performance of our business. And in our most recent 8-K’s we’ve given total transparency in terms of how those measures are calculated.”

Hedgeye: We disagree. How LINN excludes the cash cost of put options from “distributable cash flow” by amortizing them through the unrealized loss on commodity derivatives line has neither been adequately explained nor justified (it's complex and most LINE investors don't understand it). Further, “maintenance capex” is still very much a mystery; we are not able to calculate or estimate this number on our own. In fact, LINN’s IR team has told us that it’s not possible with publicly available information. This is hardly transparent.

Cramer: “[Kevin Kaiser] says that ‘LINN can’t keep production flat despite $260MM of capital expenditures, yet the amount of capital spending that is deducted from their definition of distributable cash flow was only $110MM.’ He’s saying that your free cash flow was actually negative $40MM…”

Ellis: “Jim, what you have to understand in our business is that one quarter does not make a company. One quarter is not the appropriate measure for determining whether or not your maintaining your asset or not [sic]. You have to look at the body of the work over the course of a full year; so I think he’s taking a pretty short view of our business.”

Hedgeye: This is a weak argument that is not supported by the data. First off, LINN is a pretty standard E&P company – spud-to-sales times are ~30 - 60 days. There are no significant upfront costs to be followed by a large increase in production months or years later. Second, let’s do what Mr. Ellis suggests and look at the Company's performance over a longer duration. LINN says that maintenance capex should be considered on an annual basis, but let’s look at the last two quarters plus the guidance for 2Q13; this is an instructive exercise because the Company did not close any material acquisitions over these three quarters, so we have three straight quarters of organic numbers. Production averaged 800 MMcfe/d in 4Q12, 796 MMcfe/d in 1Q13, and management has guided 2Q13 production to 780 – 820 MMcfe/d. After adjusting the 2Q13 guidance for the Panther divestiture (expected to close on 5/31/13), the midpoint of the 2Q13 guidance is 806 MMcfe/d (by our estimates). So for three consecutive quarters LINN will have essentially no production growth, and total capex will exceed maintenance capex by $491MM. "Distributable cash flow” over these three quarters equals $497MM. In our view, if maintenance capex was anywhere near what it is really costing LINN to maintain production, there would be no distributable cash flow (see table below).

Ellis: "I think many of the facts were misleading.

Hedgeye: Freudian slip?”

If you want to talk to Kaiser in more detail on this name and/or subscribe to his work to get some insight on the next big animal he is going to take down, email sales@hedgeye.com.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, VIX, and the SP500 are now $1441-1479, $100.07-106.05, $82.17-83.12, 98.65-101.78, 1.77-1.88%, 12.12-14.41, and 1610-1642, respectively.

Enjoy the weekend.

Keep your head up and stick on the ice,

Daryl G. Jones

Big Game Hunter