This note was originally published at 8am on May 09, 2013 for Hedgeye subscribers.

“Don't blindly follow me or anyone else into a stock.”

-David Einhorn

Yesterday was a great day for transparency in our profession. Some of the world’s best players stepped up to the podium at the Ira Sohn Foundation’s Conference in NYC and dealt the investing community their best card. Well, sort of.

First, there was Bloomberg Messaging, then there was AOL Instant Messenger, and now there’s Twitter. If you didn’t know that Twitter Is The New Tape, now you know. Watching the #Sohn2013 handle yesterday made you feel like you were right there at the poker table.

If you’ve played the game, you get it. If you haven’t, watching the game and all its subtleties helps. Were these guys throwing up aces, kings, or bluffs? What was already on the table before the game even started? These guys (yes, they were all guys) had to show something. Don’t underestimate the peer pressure to not look dumb. That’s the ante.

Back to the Global Macro Grind…

I love this game, so watching the game within the game like that while the market’s macro clock is ticking is about as exciting as my day in this business can get. I know, nice life.

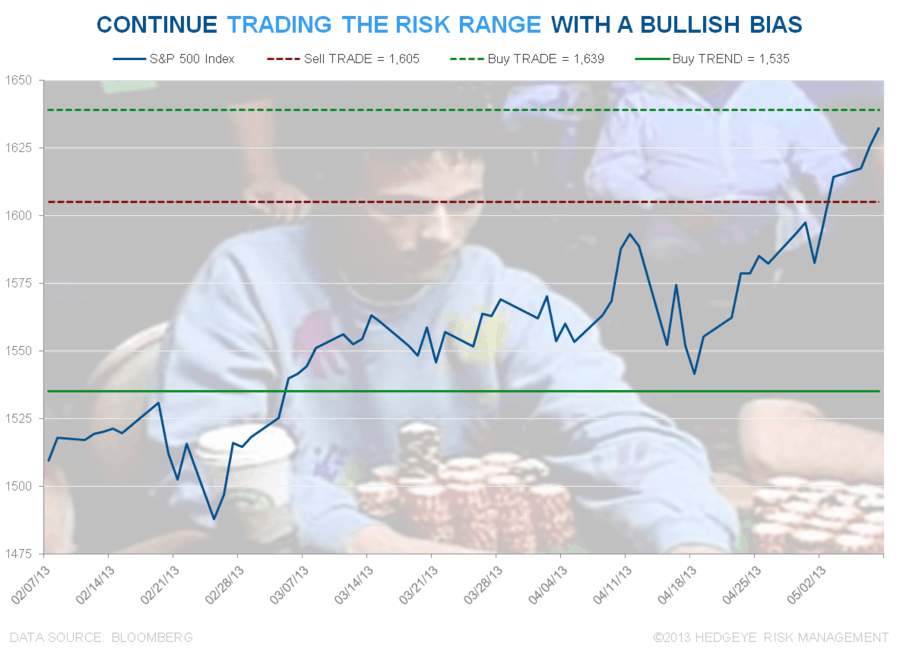

With the SP500 up for the 5th consecutive day, hitting another all-time (which is a long-time) record closing high of 1632 (+14.4% YTD), I was selling all day as I watched the #Sohn2013 ideas roll onto the new tape.

#TimeStamps: 3 days ago I had 18% Cash in the Hedgeye Asset Allocation Model – this morning I have 32%. In other words, from a gross exposure perspective, we are raising some cash now. In terms of a measurable hybrid net exposure, I’ve gone from 12 LONGS, 5 SHORTS (Monday) to 9 LONGS, 7 SHORTS @Hedgeye as of yesterday’s close.

But let’s get real here, who cares about my hand? I don’t run a real-fund anymore. I just run my mouth. So here’s my synthesis of what 5 players at the big boy table (Einhorn’s Table) were doing – what my team would act on, and why:

1. Kyle Bass – pitched a small cap ($284M) stock (DXM) that had already moved (annoying). Then he told some great jokes about the Japanese as he re-hashed what we have been saying since September 2012 when we started shorting the Yen (see our #QuadrillYen Global Macro Theme, it’s hash tagged). The Yen is up this morning; JGBs doing nothing; no impact.

2. Bill Ackman – put in the least impressive performance of the day re-pitching a very well known big cap stock (Procter & Gamble, PG) that hurt him in April (PG went straight down on its earnings report from $82 to $76). He reminded us that it’s a great company. Thanks. Stock acted like market beta on the day. No impact.

3. Stan Druckenmiller – finally brought the thunder with the best macro presentation of the day (because his Global Macro call is the exact same as ours, of course). Long US Stocks. Short Commodities. And Short Ben Bernanke. Druckenmiller’s retirement account (his own money) is bigger than most funds, and he is clearly having a great year. Loves GOOG still – stock looks great.

4. David Stemerman – did two things that we like: 1. Played a short idea (Short South African Retailers) and 2. Played a short idea that is not a consensus amongst hedge funds. If we’re right on #StrongDollar and Down Gold, short South African Equities scores very well. So did Stemerman in taking his first seat at the big boy table. #impact

5. Jim Chanos – Doc brought the thunder for the hedge fund brothers and played the hand we all want to see – a full house idea that you can get big and liquid in (short legacy Personal Computers, Components, etc.). When Seagate (STX) opens this morning, you’ll see why Chanos remains The Man on well researched, high conviction, short selling.

Jacobson (Highfields) said he likes an idea we have been very vocal on (Kevin Kaiser’s Short/Sell call on Linn Energy – LINE, LINCO, BRY). Gundlach said short a stock that we’ll probably buy today if it hits our signal level (Chipotle, CMG – we made that short call last year, it’s stale) and Einhorn played a hand that everyone loves (a value stock that is starting to trade like a bull market momentum stock, in OIS).

All-in it was a great event for a great cause (pediatric cancer). Twitter didn’t sponsor the event, but the transparency/accountability pipe for #WallSt2.0 certainly helped bring the event’s profile to new heights (next to #Bengahzi, #Sohn2013 was the Top Trending Handle in the USA yesterday). That’s cool, and so is any opportunity the world has to eavesdrop on the table of some of the world’s best players.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, VIX, and the SP500 are now $1441-1489, $99.39-106.19, $81.51-82.92, 97.89-99.94, 1.73-1.86%, 12.06-14.01, and 1605-1639, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer