TODAY’S S&P 500 SET-UP – May 21, 2013

As we look at today's setup for the S&P 500, the range is 31 points or 1.16% downside to 1647 and 0.70% upside to 1678.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.72 from 1.73

- VIX closed at 13.02 1 day percent change of 4.58%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: ICSC weekly sales

- 8:55am: Johnson/Redbook weekly sales

- 11am: Fed to purchase $2.75b-$3.5b notes in 2020-2023 sector

- 11:30am: U.S. to sell 4W bills

- 11:30am: Fed’s Bullard speaks in Frankfurt

- 1pm: Fed’s Dudley speaks in New York

- 4:30pm: API energy inventories

GOVERNMENT:

- Apple CEO Cook appears before House Permanent Subcmte on Investigations to talk about offshore profit shifting, tax code alongside Apple CFO Peter Oppenheimer and Tax Operations Head Phillip Bullock; Cook said he’d present tax code simplification ideas at hearing, 9:30am

- IRS Acting Commissioner Steven Miller, Treasury’s IG for tax administration, J. Russell George, Former IRS Commissioner Doug Shulman testify before Senate Finance, 10am

- CME Chairman Terrence Duffy, ICE CEO Jeffrey Sprecher testify before House Agriculture Cmte on future of the CFTC, 10am

- Financial Industry Regulatory Authority annual conf., 9:30am

- Congressional Progressive Caucus holds discussion on wages in federal contracts, 3pm

- Treasury Sec. Jack Lew speaks to Senate Banking Cmte on Financial Stability Oversight Council’s annual report. 10am

- House Financial Svcs panel hearing, “Qualified Mortgages: Examining the Impact of the Ability to Repay Rule,” 10am

- SEC Commissioner Daniel Gallagher speaks at meeting of Women in Housing Finance, 12pm

- House Financial Svcs panel holds hearing on Dodd-Frank’s conflict minerals provision, 2pm

- BSA releases study on piracy’s economic impact on govts

- NIST Director Patrick Gallagher, others testify before House Energy and Commerce Cmte on cyber threats and security, 10am

WHAT TO WATCH

- JPM shareholders vote whether to split chairman, CEO roles

- Apple CEO Cook, other execs testify today in D.C. on taxes

- Sprint to give Dish nonpublic data as Softbank grants waiver

- Clearwire holder vote on Sprint may be postponed: NY Post

- Dish chairman Ergen said to bid $2b for LightSquared assets

- Death toll from Oklahoma tornadoes rises to 91

- Ex-McKinsey exec. Gupta to appeal insider trading conviction

- Boeing open to increasing production rate for 787, CEO says

- Microsoft to unveil new Xbox at event in Redmond, Wash.

- IRS tax-exempt scrutiny to be subject of Senate cmte hearing

- IRS ex-official Shulman withdraws CBOE board candidacy

- Carnival says lower prices forced earnings forecast cut

- Yahoo to expand in NYC with new Times Square office

- NetJets CEO says U.S. leading demand for private flights

- Grifols to buy 35% of Aradigm after latter’s capital increase

EARNINGS: (all times ET, times are approximate)

- Home Depot (HD) 6am, $0.76 - Preview

- AutoZone (AZO) 7am, $7.21

- Medtronic (MDT) 7:15am, $1.03 - Preview

- Dick’s Sporting Goods (DKS) 7:30am, $0.48

- Best Buy (BBY) 7:31am, $0.24

- Tidewater (TDW) 7:51am, $0.61

- Saks (SKS) 8am, $0.18

- TJX (TJX) 8:32am, $0.62

- Intuit (INTU) 4pm, $2.93

- Analog Devices (ADI) 4pm, $0.52

- NetApp (NTAP) 4:01pm, $0.68

- Compuware (CPWR) 4:05pm, $0.05

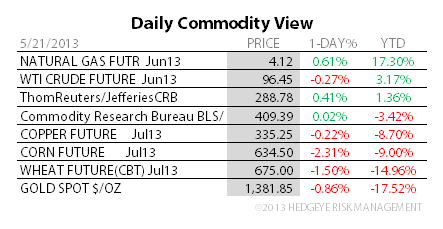

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Declines in London as U.S. Stimulus Outlook Curbs Demand

- Platinum Buying Quickens as Gold Allure Diminishes: Commodities

- WTI Crude Trades Near Seven-Week High as Stockpiles Seen Falling

- Copper Swings Between Gains and Drops Amid Concern About Supply

- Corn Declines for Second Day as U.S. Farmers Accelerate Planting

- Palm Oil Seen Dropping by Mistry as Output, Stockpiles Climb

- Freeport Mine Death Toll Rises to 21 as Indonesia Reviews Mines

- Hunan Rice Sales Plunge as China Probes Cadmium Contamination

- Crude Supplies Decline a Second Week in Survey: Energy Markets

- Brazil Coffee Growers Seek Price Review From ICE Futures U.S.

- Adaro Chief Says Coal at $100 a Ton New Normal: Southeast Asia

- ThyssenKrupp Woes Tarnish 99-Year-Old Steel Baron Beitz’s Legacy

- Gold-Silver Price Suggests Stocks to Snap Gain: Chart of the Day

- Cocoa Gains in London as Pound Nears Six-Week Low; Sugar Falls

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

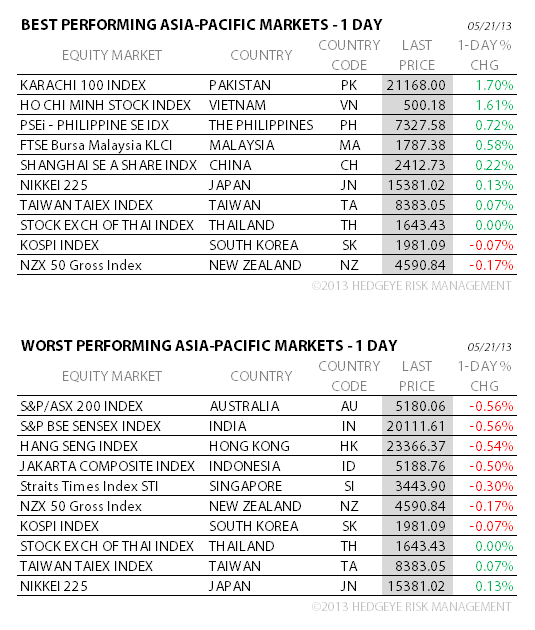

ASIAN MARKETS

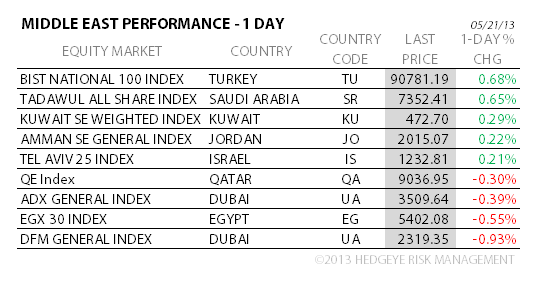

MIDDLE EAST

The Hedgeye Macro Team