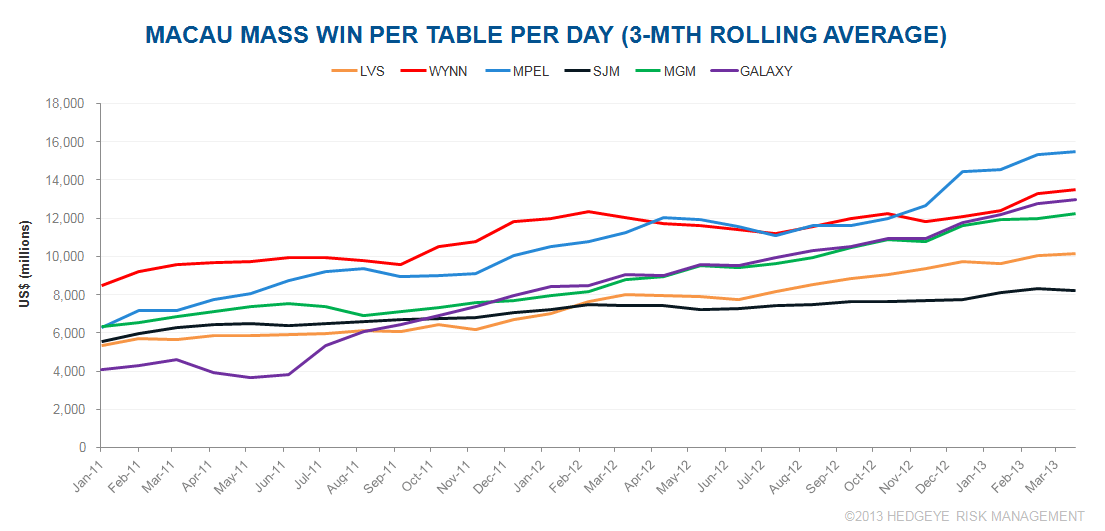

MPEL’s Mass push has been an overwhelming success

- Mass revenue per table still climbing at a fast rate for all operators with the exception of capacity constrained SJM

- MPEL’s Mass business has come a long way in 2 years and the operator is firmly entrenched as the market leader in terms of productivity and growth (along with Galaxy on the growth front)

- Remind us again why MPEL deserves such a valuation discount? It can’t be due to operational prowess. EBITDA is not shown here but MPEL is also the market leader in same-store EBITDA growth over the same period.