This note was originally published May 14, 2013 at 11:15 in Restaurants

A revival of trends in the U.S. is a key pillar of the bull case on MCD. In light of the “menu innovation” year-to-date, we feel confident standing by our bear case.

A few months ago we wrote that McDonald’s was going to abandon its Angus burger and now we read that a new line of quarter pounders is replacing the product in an effort to deliver the top-line growth needed to meet expectations.

Bull Case Crumbling

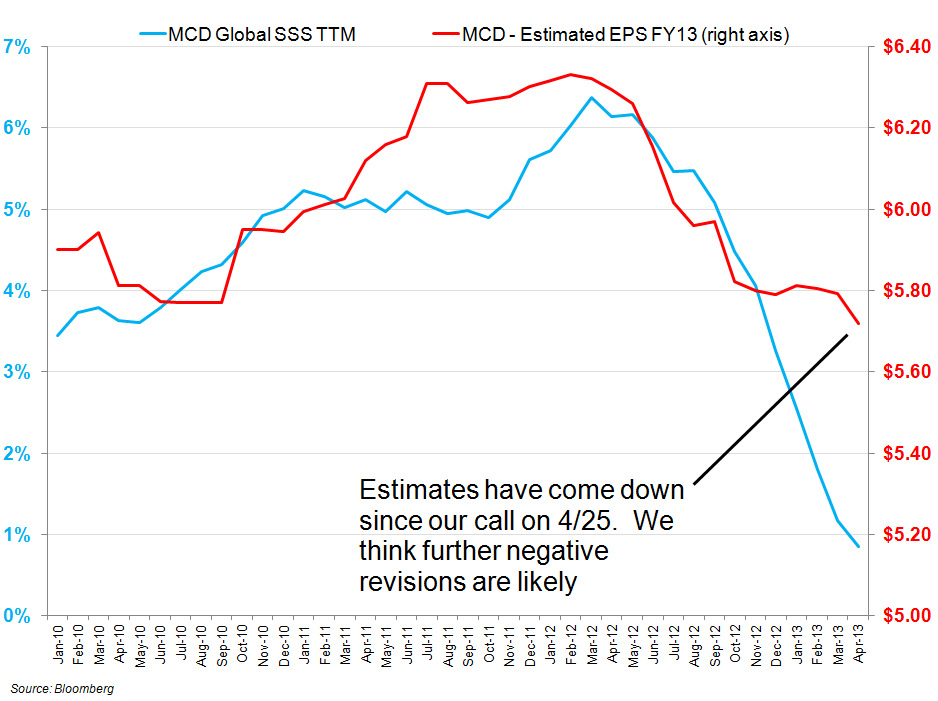

One bullish analyst on the Street has suggested that the company needs a “hero-like lifting” from U.S. consumers as the global macro picture looks mixed. The expectations that comps will reflate seems stretched, given our view on MCD’s pricing flexibility, and we expect U.S. comps to fall short of the level needed to carry the stock higher. We believe the most likely outcome is that the fundamentals of McDonald’s business continue to suggest a lowering of EPS expectations for 2013.

Innovation?

The recent news that McDonald's is adding to its Quarter Pounder line up has spurred a lot of dialogue among the investment community. These additions are not quite as striking as past innovations but are unusual in that they fall on a generally stable part of the McDonald's menu. Greg Watson, McDonald’s USA SVP-Menu Innovation Team said, “we haven’t touched the Quarter Pounder since its inception 40 years ago. We think this is a great way to bring new news to the brand.”

Six months ago, the question on investors’ minds was, “what menu innovation will MCD push through to grow the top line?” Now, we know: premium wraps and a new line of quarter pounders. In light of this, we remain confident in our bearish thesis.

From late May or early June, there will be three new Quarter Pounder varieties offered at McDonald’s with national advertising starting in mid-June.

- MCD is going to take most popular condiments from the Angus line and put them on the Quarter Pounder brand

- The company is creating a third new flavor—Habanero Ranch with white Cheddar, bacon, lettuce, tomato, and habanero ranch sauce tested

- The new quarter pounders will be served on bakery-style buns

What Does the Failure of The Angus Burger Tell Us?

It is difficult to know why the offering failed. It could have been too expensive for the McDonald’s customer or the construct of the burger may have been unpopular. If either of these speculations is true, it could suggest that the new quarter pounder offerings – drawing from the Angus ingredients – are unlikely to resonate or, if pricing was the issue, that McDonald’s has limited pricing flexibility. Neither scenario would be positive for shareholders.

The early August release of July sales will be the day when we gain the most significant insight into the effectiveness of this year’s menu changes. We continue to believe that the Street’s numbers are too high.