This note was originally published at 8am on April 17, 2013 for Hedgeye subscribers.

“Horse manure sprinkled with tobacco.”

-William Silber

That’s what “a cigar aficionado had once told him” (with him being Paul Volcker) about “his favorite A&C Grenadiar cigar.” In 1979, Volcker would take a big pay cut (“earning $57,500 a year rather than the $110,000 salary”) as President of the New York Fed. (Volcker: The Triumph of Persistence, pg 147)

Unlike some of these pretend patriots you see on Political Economy TV today, Volcker took serving his country in the wallet. Like Benjamin Franklin, he was a frugal man. He, like anyone tasked with central planning, had his issues. But one of those wasn’t credibility. The #PoliticalClass didn’t always like him, but history has treated him well, primarily because he earned The People’s trust.

When Bernanke proclaimed that he has “the best inflation track record of anyone since WWII”, it made me sick to my stomach. Today, in 1964, Americans bought their first Ford Mustang for $2,368. That was also a time when JFK explicitly marketed a #StrongDollar. Hopefully, we’re well on our way to deflating Bernanke’s Commodity Bubbles now. Lord knows, we all need a real-world Tax Cut.

Back to the Global Macro Grind…

Within the context of the immediate-term risk I ranted about in yesterday’s Early Look, yesterday’s +1.43% rip in the SP500 was critical on all three fronts that matter in one of my most basic 3-factor models:

- PRICE – what was 1557 immediate-term TRADE resistance, once again became support (no resistance now to 1601)

- VOLUME – up +3.3% versus what I call my TREND average (up days on up volume = good)

- VOLATILITY – VIX smoked for a -19.2% down move, closing back below TRADE resistance (14.27); next support 10.53

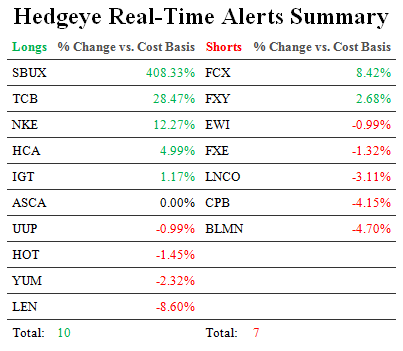

So, I got a little longer (net), going to 10 LONGS, 7 SHORTS @Hedgeye. Process: as beta (SP500) recovered my TRADE line of support (1557), the first moves I made were A) covering consumption shorts and B) buying consumption longs (we’re bullish on US domestic Hospitals, so Tom Tobin had me buyback HCA on sale).

From both a gross and net perspective, I can obviously get a lot longer than this. I have throughout the last 5 months, and I will continue to buy pullbacks, provided that both the Research and Risk Signals tell me to do so. But I will do it at my own pace. Patience is an asset.

What generalist PMs and individual investors alike have to be getting impatient with is more of the same; especially if they aren’t yet positioned LONG CONSUMPTION vs SHORT COMMMODITIES.

Top Down, the YTD score is very straightforward:

- SP500, US Healthcare, and US Consumer Discretionary = +10.4%, +19.7%, and +13.3%, respectively

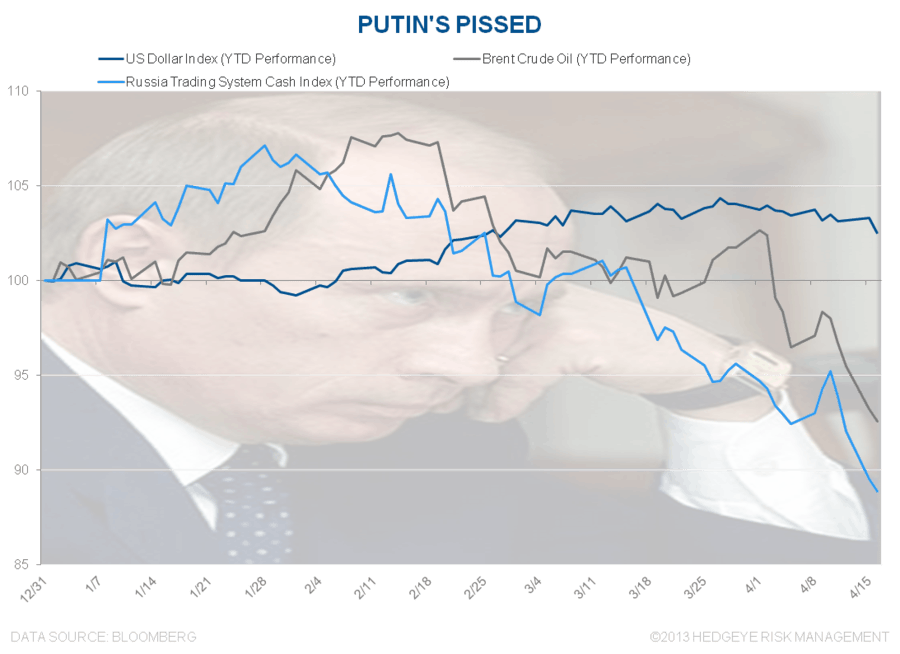

- CRB Commodities Index, Gold, Russia = -4.1%, -17.3%, and -11.5%, respectively

In terms of US Equity Sector performance, so are the month-to-date returns for April at mid-month:

- Healthcare (XLV) +3.76%, Consumer Staples (XLP) +2.62%, Consumer Discretionary (XLY) +1.40%

- Energy (XLE) -4.50%, Basic Materials (XLB) -3.04%, Industrials (XLI) -1.72%

In other words, the performance divergence between CONSUMPTION and COMMODITY related investments is accelerating at an accelerating rate. We like that. It’s called convexity.

To be clear, like the conflicted and compromised bureaucrats that Volcker and Thatcher had to take head on in the early 1980s, people who don’t get paid by #CommodityDeflation do not like this. Neither do the dudes who get paid to market Gold commercials.

But, like I said on yesterday’s Global Macro Themes call for Q2 2013 (ping Sales@Hedgeye.com if you want the slides/replay), it’s not my job to pander to fear-based advertising for bitcoins. Neither is it to live a regressive life. What’s happening to Gold and Oil in particular is potentially one of the most progressive economic developments in the last 20 years.

Risk Management Questions I addressed on our Q2 Macro Themes call:

- Can the US Dollar Index go to $88, then $98?

- Can the Japanese Yen (vs USD) go to 110, then 150?

- Can the price of crude Oil drop to $19-56/barrel?

It’s all interconnected. And if the answer to all three of those questions were to become yes, all I can say is that A) being long Consumption will be really right, B) being short Commodities will be epic, and C) Putin will be pissed.

Putin? Yes, as in Vlady. Russian geopolitical and said economic-power runs on Oil inflation. He’s been whining in the press for the last few weeks, so expect his next move to be Japanese (devalue the Ruble). Then this flow show party can really get started.

Flow show? No, I’m not talking about my hair. I mean #EmergingOutflows (introduced as our latest Global Macro Theme in yesterday’s conference call). #StrongDollar = bad (for some Emerging Markets). So we’ll have a deeper dive Hedgeye Black Book pending on that. Knock on wood (my hockey head), but horse manure sprinkled with some Hedgeye Macro tobacco has never smelled so good.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, Euro/USD, UST10yr Yield, VIX and the SP500 are now $1284-1399, $99.43-103.99, 95.77-101.70, $1.29-1.31, 1.70-1.77%, 10.53-16.65, and 1557-1601, respectively.

Happy Birthday Laura, and best of luck to you out there today,

KM

Keith R. McCullough

Chief Executive Officer