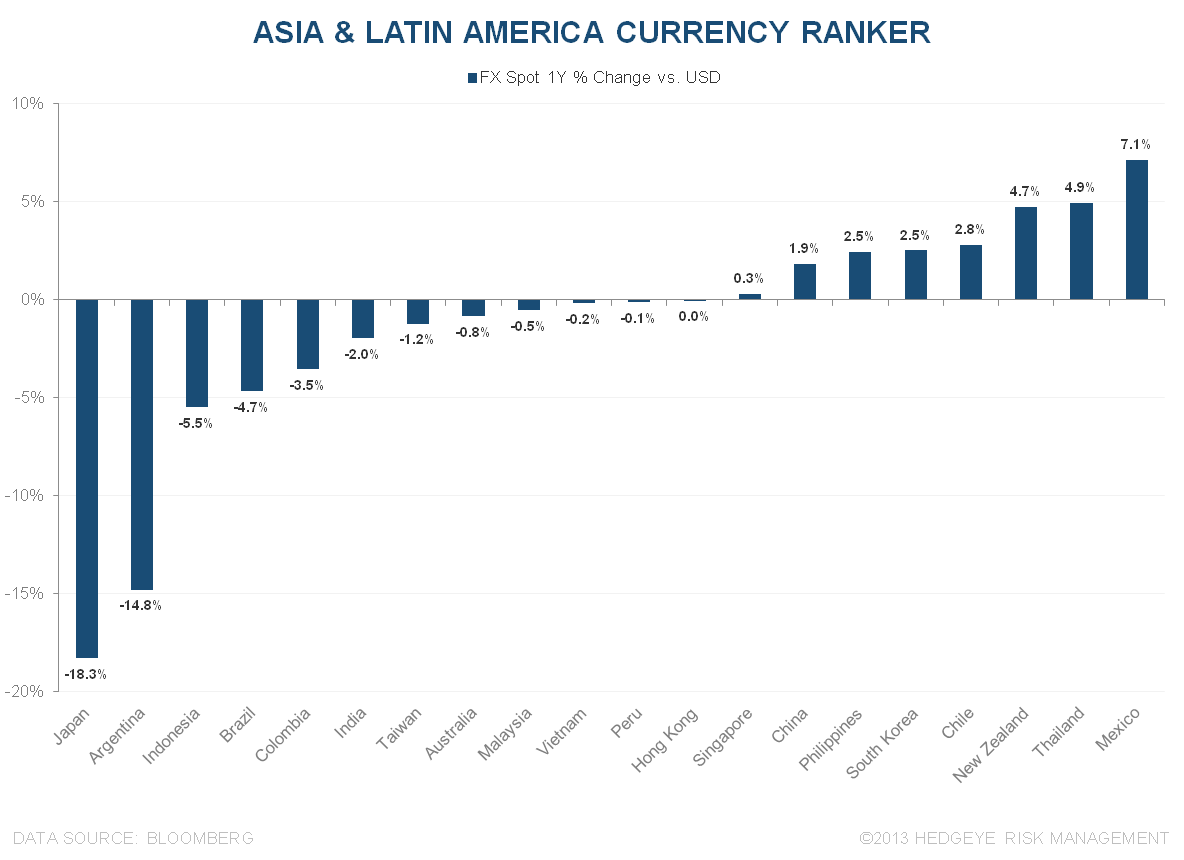

Argentina has one of the best performing equity markets in the world. Over the last twelve months, their Merval Index (Argentina’s equivalent of the S&P 500) has put up +67.9% in gains as the value of the Argentine Peso (we are bearish on the currency) plunges against the value of the US dollar.

While the country’s stock market is on fire compared to America, the country’s underlying economic situation leaves much to be desired. In fact, much of the equity market strength is being driven by strict capital controls and fear of eventual public confiscation of household deposits. Last week, Argentina turned to the International Monetary Fund (IMF) for a $400 million cash deposit in order to increase their allocation to an emergency line of credit of sorts. Though the country had $39.8 billion in reserves, Argentina is drawing on those funds for bond repayments ($30 billion since 2010) and it just hit a six-year low. Essentially, the country is fiscally under the gun and will remain in a tough spot as long as Cristina Fernandez is president.