With the stock raging in the final hour of trading on Friday – up 14.6% with volume more than tripling – it’s pretty clear that someone already knew that the company had taken a major step towards shoring up its liquidity.

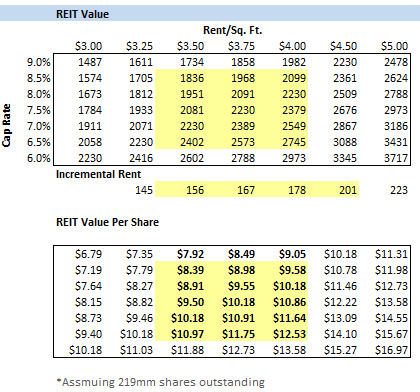

But in looking at the transaction itself, it's positive any way you slice it, and it makes a ton of sense as Ullman’s first move out of the box as CEO. In addition, while the deal stipulates that the $1.75bn term load is securitized by real estate and ‘all other assets’ of the company – we think that the latter language of that agreement is irrelevant. We estimate that the lower end of JCP’s real-estate value clocks in at a little over $1.8bn, or $8.40 per share. Under a best-case scenario (which we have no fundamental reason to bank on) we get to $2.745bn, or a little over $12.53 per share. Nonetheless, the real-estate should cover the loan.

Our Take On The Stock

Ullman and the stock are one and the same at this point. The good news is that he’ll be a stabilization factor as it relates to a) the balance sheet (done), b) talent retention, and c) stopping the bleeding in what remains of JCP’s core customer. Even better news is that when JCP reports earnings in May, the company will blame any negatives on Johnson, and take credit for any positive changes on the margin. It'll be tough to spin the print in a way that does not favor JCP. Near-term momentum remains in JCP’s favor.

On the flipside, we’re still not comfortable enough with JCP's long-term strategy to have it on our Best Ideas list, as we’d need confidence in revisiting $2.50+ in EPS power in order to get us enough outsized upside in the risk/reward profile. While we saw severe incompetence in pricing the existing business with Johnson running the show, the reality is that he had a vision as to what JCP could become, and it was one that made sense. It was no slam dunk by any means, and was riddled with execution challenges. But it was one where we could make financial assumptions in the outer years, apply a discount rate, and build up to over $3 in EPS power.

We’re now seeing Ullman solve the balance sheet issue – but that’s something that we were confidence would have been resolved under Johnson. What we don’t have anymore, however, is a reasonable sense of what this company could look like in another 2-3 years. Despite what they say, it simply has no long-term strategy. There’s a short-term CEO who is in place to fix short-term problems. While that happens there’s no reason why this stock can’t grind higher, and we think it will. The ‘JCP is expensive’ call does not hold much water here. That said, we’d rather wait to get involved in a big way when we could be confident in the BIG research call – like 50%+ over a 1-2-year period. When playing for that kind of upside, we're not concerned about getting involved a few dollars higher. Until then, we'll trade the name.