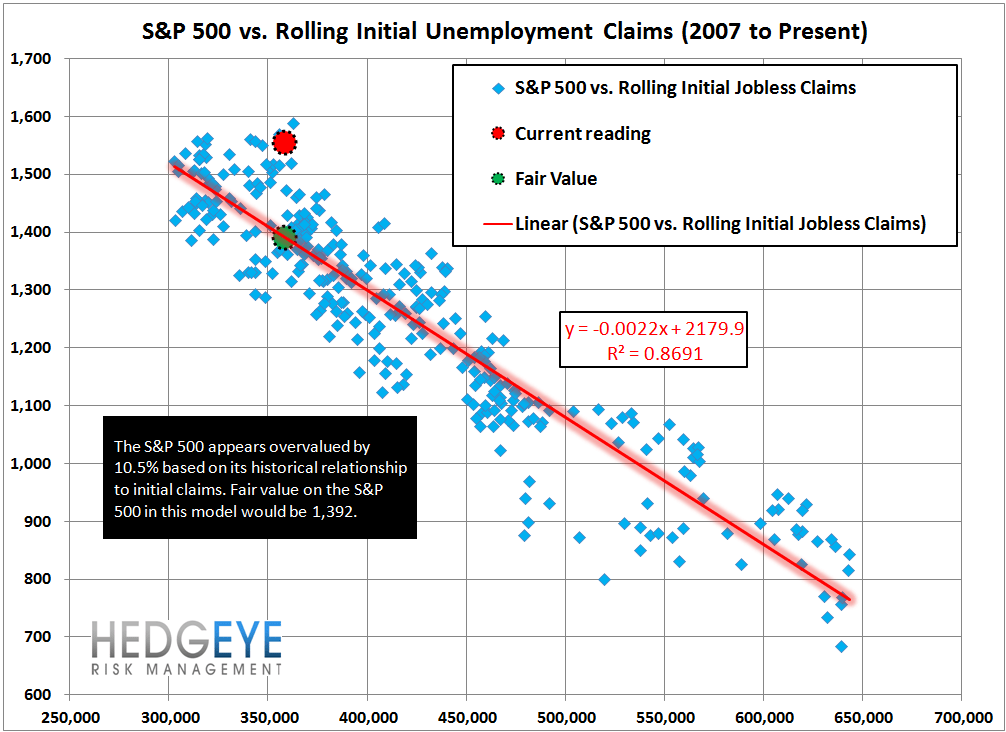

Long in the Tooth, but OK for Now ...

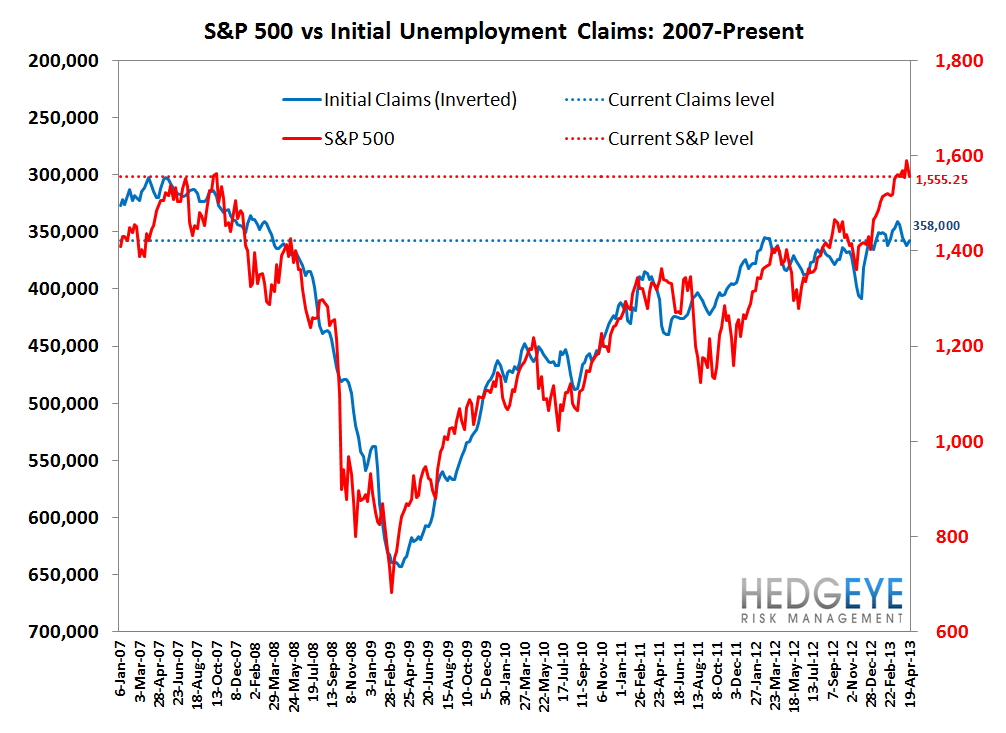

Both SA and NSA initial claims posted sharp improvement in the latest week. In the past we've shown how initial claims are the best leading indicator for forward delinquency metrics at credit card lenders, on a 13-week lead/lag. Clearly, card results were better than expected in 1Q13 and the claims data we're seeing currently suggests further progress in 2Q from DFS and COF, and AXP to a lesser extent.

We've argued in the past that renormalized delinquency levels, i.e. reaching DQ levels consistent with 2005/2006 averages, would herald an end to reserve release tailwinds, and, by extension, usher in earnings growth headwinds. This ongoing positive trend in claims, however, coupled with Krugman's "Jobless Trap" - the segment of the population now perpetually long-term unemployed - has enabled a continued fall in DQ rates since this former core subprime cohort is now "non-underwriteable".

This curious confluence of positive selection (vs. adverse), fast turning assets and secular credit tailwinds has pushed operators to take down coverage further than we would have thought prudent or possible. While this sets the stage for ongoing improvement in the short/intermediate term, we continue to fret about the long-term implications of making all-time lower low DQ rates in a low-growth, highly competitive asset class. Auto is perhaps an even more glaring example, as we noticed in the weekend paper a local credit union offering 0.99% on terms up to 48 months. How that will even cover normalized credit losses in this newly emerging environment of falling used car collateral values I have no idea. But for now, everything's good.

The Numbers

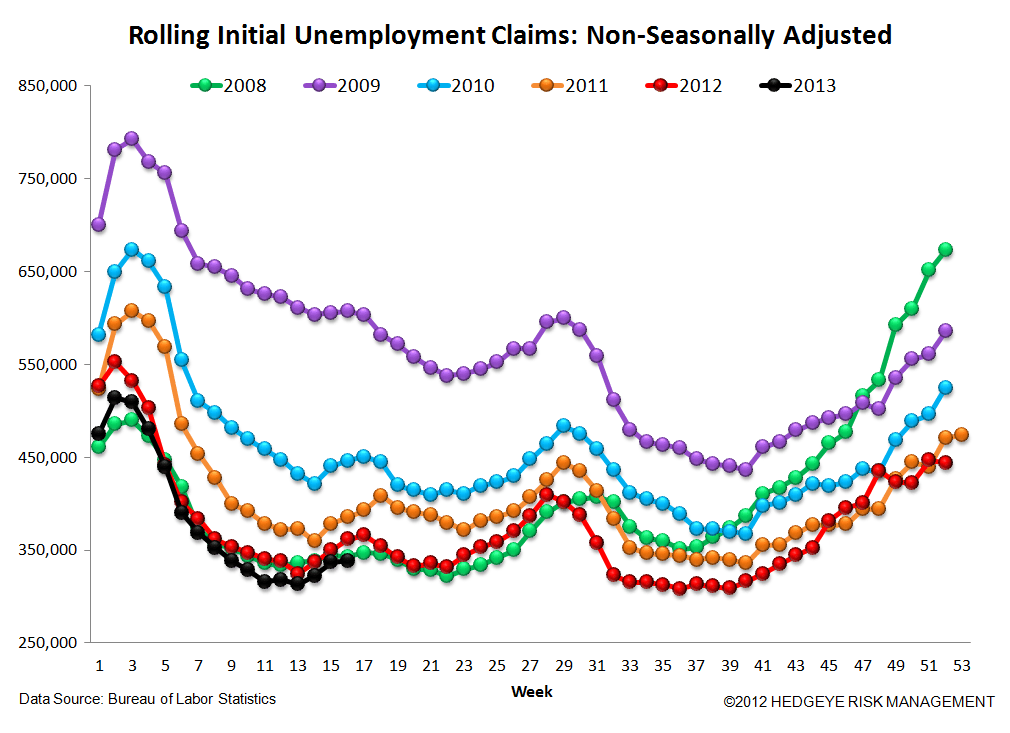

Prior to revision, initial jobless claims fell 13k to 339k from 352k WoW, as the prior week's number was revised up by 3k to 355k.

The headline (unrevised) number shows claims were lower by 16k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -4.5k WoW to 358k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -6.3% lower YoY, which is a sequential improvement versus the previous week's YoY change of -3.8%

Yield Spreads

The 2-10 spread rose 0.2 basis points WoW to 147 bps. 2Q13TD, the 2-10 spread is averaging 152 bps, which is lower by -16 bps relative to 1Q13.

Joshua Steiner, CFA