“Winning is not a sometime thing; it’s an all time thing. You don’t win once in a while, you don’t do things right once in a while, you do them right all the time. Winning is habit. Unfortunately, so is losing.”

-Vince Lombardi

Last week I took a few days of vacation and had the opportunity to catch up on some reading. One of the key books I read last week was, “Top Dog: The Science of Winning and Losing”, by Ashley Merriman and Po Bronson. As the title suggests, the book is a deep dive into the science behind winning, losing, and competitiveness and has applications that go well beyond athletics.

Last week I was also continuing to enjoy the fact that my alma mater Yale recently won the NCAA ice hockey championships. To be fair, a NCAA championship, while a big deal to the players, fans and alumni, is a far cry from a gold medal, Stanley Cup, or World Championships. Nonetheless, it is an example of a team achieving its ultimately goal in a very competitive situation.

Going into the 16 team NCAA hockey tournament, Yale was seeded 15th and a 60:1 underdog according to the Vegas odds makers. On the path to the championship, Yale also achieved a few things that no team had every done before. First, they beat three number one seeds (each regional of four teams has a number one seed). Second, they are the only fourth seed in the Frozen Four to ultimately win. Clearly, this is an example of a team that overcame significant obstacles to become a champion.

So, what is it that enables some teams to win against extreme odds? Counter to intuition, team members getting along and being traditional team players is not the key. In fact according to Merriman and Bronson:

“In the idealized notion of a team, everyone is equal and interchangeable, and this equality drives commitments to the team effort. But the science argues that the ideal is, if anything, a distraction. The goal is not to live up to the ideal, but to perform. In real life, teammates are rarely true equals, and they don’t always get along. Having a hierarchy, with its clear divisions of responsibility, is most often the solution to team performance.”

To use economic terms, great teams are usually much more capitalist than socialist.

Now as Keith would say, back to the global macro grind . . .

In terms of global economic statistics, Spain’s unemployment rate is certainly one that signifies that the nation continues to lose economic share. At a 27.2% rate of unemployment, with an even larger unemployment rate for those new to the work force, Spain is not going to see economic recovery without some help from her teammates.

The key friend to Spain is likely to be ECB President Mario Draghi, especially if he decides to cut rates as he was hired to do. Luckily for Spain, our quantitative models are also signaling that the ECB is likely to ease again. Specifically, every major European equity market is now in a bullish formation in our models, expect Russia. This makes sense as Europe easing would be U.S. dollar bullish, which is negative for the price of oil and Russia is the largest exporter of oil in total barrels per day terms in the world.

Key sovereign debt markets also appear to be signaling some chance of the ECB incrementally easing. Since the world didn’t end with Cyrpus’ bail under as many market pundits were urging would happen, peripheral yields in Europe have tightened meaningfully. Despite the aforementioned employment issues, Spain’s 10-year yield is now at 4.38% and Italy’s 10-year yield is now at 4.06%. As it relates to Italy, this is the lowest yield on the 10-year in more than a year.

Much of the pin action this morning in global equity markets is coming from China. For those that tuned into our conference call on emerging markets this week, this should be no surprise. We came into the year bullish on Chinese equities and have reversed that stance based on new data. The China section in the emerging markets presentation given by my colleague Darius Dale was titled, “Will China Blow?”. Increasingly, this is a very fair question to ask on China.

A key risk or concern over China is whether real estate market prices are in a bubble and whether there is too much debt behind the Chinese real estate market. In effect, is China about to go through a real estate correction comparable to what the U.S endured starting in 2007? Some would argue that the high pace of Chinese economic growth inherently supports a rapid increase in real estate values and this is likely true, to a point.

In general, debt and real estate are very much driving Chinese equity markets. Overnight, the Shanghai Composite closed on its lows as the property subsector once again dramatically underperformed. This was on the back of a Minister of Taxation official warning that if property prices in second tier cities continue to rise then more property taxes will be implemented. On one hand, you do have to hand it to Chinese officials attempting to proactively manage bubbles. On the other hand, the history of government intervention is that governments rarely get things right.

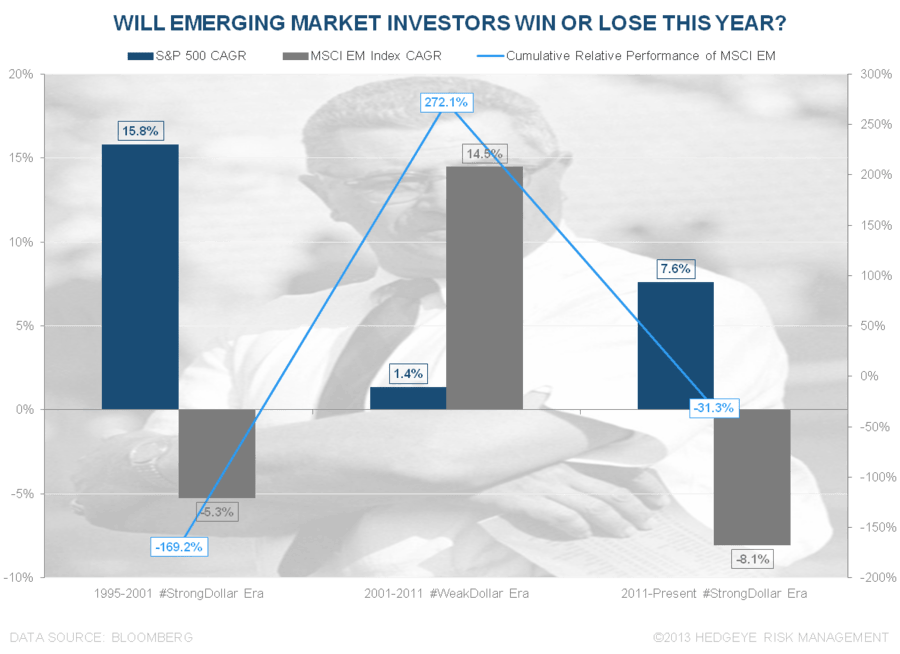

In the Chart of the Day below we’ve highlighted a key slide from the emerging market presentation from earlier this week. This chart shows the performance of the SP500 and MSCI Emerging Market Index in strong dollar periods and weak dollar periods, respectively. They key takeaway is that in strong U.S. dollar periods emerging markets underperform dramatically as, among other things, capital flows out of emerging markets. On the back of this research, we added the emerging markets ETF, EEM, as a short idea on our best ideas list.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, VIX, and the SP500 are now $1, $97.31-103.34, $82.55-83.44, 97.45-101.36, 1.70-1.76%, 11.33-14.89, and 1, respectively.

Keep your head up, stick on the ice, and keep #winning,

Daryl G. Jones

Director of Research