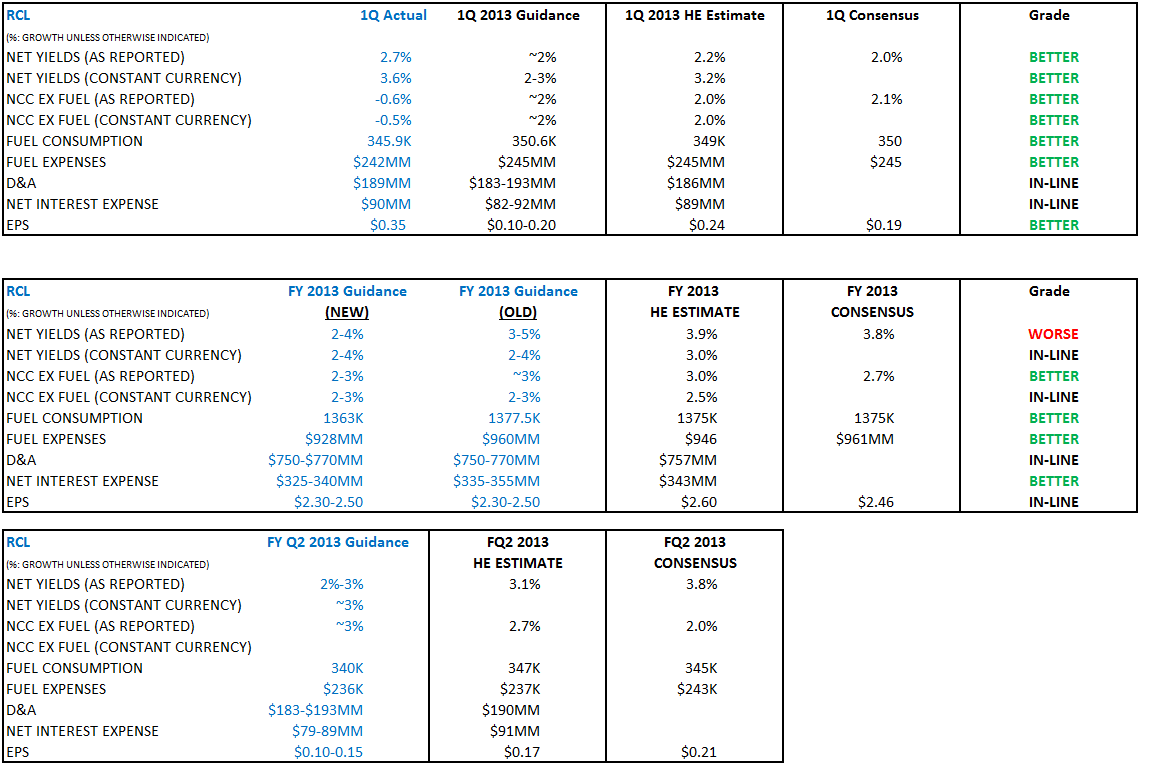

In an effort to evaluate performance and as a follow up to our YouTube, we compare how the quarter measured up to previous management commentary and guidance

OVERALL

- BETTER: Given the many scares in the industry recently, the earnings beat, unchanged guidance and some reassuring comments on the conference call were a net positive.

EUROPE

- SLIGHTLY BETTER: More optimistic but still see limited visibility. Germany is doing well, offset by weakness in Spain and UK. RCL believes for this segment, it is sufficiently ahead on rate and occupancy for FY 2013. Around February, they were less than 50% booked for 2013, now they are 70% booked. No changes in 2014 itineraries that have been announced.

- PREVIOUSLY:

- "Even though the economies in the U.S. and in places like Germany and France still aren't very good or aren't great, it's really the weakness in Southern Europe that is keeping our yields from truly exciting growth. Europe represents 27% of 2013 capacity, down 3.2 points versus 2012 against the backdrop of the Arab spring in 2011 and both industry and macroeconomic adversity in 2012, we expect the yield increase in 2013 relative to both years. Northern European capacity for the industry and the company are substantially up and our year-over-year yield expectations are lower in the North than they are for the Eastern and Western Med, where our capacity is down in each sector for the second consecutive year....In aggregate, we're feeling is though we will have yield improvement in Europe this year."

- "And while the way the season is off to a promising start in most markets, we've seen a significant deterioration in demand from Spain. All indications suggest the continued challenging operating environment in Spain for an extended period of time. This has resulted in significant changes in our plans and expectations for the brand."

- "The UK has been disappointing from a volume standpoint, but pricing is above last year."

ASIA/AUSTRALIA

- WORSE: Represent 5% of 2013 capacity. Gave lower yield guidance given the removal of Japanese ports of call from nearly all of their 2013 North Asia program. As a result, most itineraries from their Shanghai/Tianjin homeports are calling only South Korea ports. Australia yields are forecasted to be flat to slightly lower YoY.

- PREVIOUSLY: "It's particularly interesting to note how well both Australia and China have held up. Both are looking towards flat to higher yields despite really very large capacity increases and in the case of China, that's in spite of the impact from the territorial dispute with Japan. Asia-Pacific... Our booked load factors look strong for sailings in the first half of the year, although pricing is behind a year ago. Overall, we expect yields to be about flat for this region despite the large capacity increases."

CARIBBEAN

- LITTLE WORSE: Still expecting record yields in 2013 but saw weakening demand for Caribbean itineraries following bad publicity in March which is now rebounding.

- PREVIOUSLY: "At the itinerary level, the Caribbean will account for 44% of our 2013 capacity, which is a 4% increase from last year. We are seeing solid booking trends for this product group, and based on what we know today, we expect a record year for yields in the Caribbean."

LOAD FACTOR AND APD TRENDS

- BETTER: Booked load factors and APDs are higher YoY. Bookings curve has been expanded across the board (similar to 2008).

- PREVIOUSLY:

- "As of today, our total booked load factors and booked APDs are slightly better than at the same time last year and better than this point in time in 2011."

- U.S. source business is up significantly versus the same period last year. Asian and Australia bookings have more than kept pace with the added capacity we have placed in both markets. With the exception of the UK and Spain, Europe has been pretty solid."

- "I think the U.S. is for the most part... in line with the year ago. We do have some pockets, some products where people are actually beginning to book a little bit further out, which is obviously helpful. Northern Europe for the most part is very consistent with what we were seeing last year. But we have seen contraction in Southern Europe. The Southern European countries are actually booking about a month closer to sailing than they had been a year ago."

ONBOARD SPEND

- BETTER: Saw improvements in all categories and on all ships in 1Q.

- PREVIOUSLY: "As it relates to onboard revenue, there's a tremendous effort taking place across all brands to create onboard revenue upside, and I would say we're cautiously optimistic at this point in the year."