This note was originally published at 8am on April 08, 2013 for Hedgeye subscribers.

“Las Vegas is busy every day, so we know that not every man is rational.”

–Charles Ellis

Today at 11am, we are going to be joined via conference call by Dr. Richard Peterson of MarketPsych Data. He will be giving a presentation called, “Behavioral Markets: Quantifying the Psychological Drivers of the Global Economy.” Over the course of the past 9 years, Peterson and his team have been developing sentiment based investment models based on global news and social media sources.

Their underlying technology scours 1,000s of data sources (in natural languages) and then assigns scores for various indicators. These scores are then updated by the minute to create an ongoing data feed, which can provide a real time assessment of sentiment in over 200 countries stock markets, 60 commodities, 30 currencies, and 40 industries.

The key reason that Peterson believes his models can highlight inflection points in markets, via blog and news sources, is based on science. In effect, intense emotions direct attention to vivid events and catastrophic consequences. As a result, the reasoning prefrontal cortex is taken offline and probability assessments are distorted. To Ellis point in the quote above, men and women are not always rational.

In his presentation today, Peterson will walk us through his process and analysis, and then get into the outputs of his model on various time frames and over various asset classes. Many of his investment conclusions we agree with, but others stand in contrast to our models and analysis. This last point should make this morning’s discussion a lively one.

The dial-in information for the call this morning is 1-800-434-1335 and conference code is 141433. The materials can be downloaded at 10:00am following the link docs.hedgeye.com/BehavioralMarkets_04.08.13.pdf. We hope you can join us for the call to get a sense for how a true behavioral finance practitioner quantifies expectations in markets.

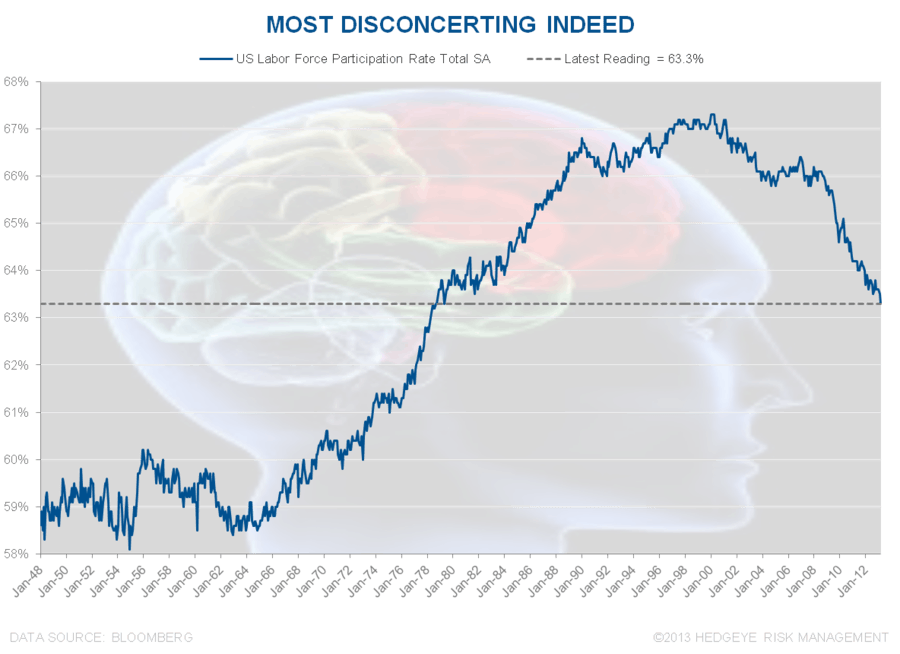

Related to gauging the market sentiment, Friday’s labor report was a bomb by almost any estimation. Non-farm payrolls increased by a mere 88,000 in March versus 190,000 expectations and a 268,000 increase in February. Most disconcerting was the internal participation rate, which measures the percentage of total eligible employees that are in the labor force. We highlight this in the Chart of the Day with a look at long term labor force participation rates, which is now at its lowest level since 1979.

Clearly, muted employment growth is a potential risk to growth accelerating in the U.S. , so we are and will be monitoring this data closely. The response on Friday from the SP500 was somewhat muted as the market was down -0.47% and remains up on the year just under +9%. In terms of sector divergence on Friday, the worst performing sector was Technology -0.8% (and +3.1% on the year) and remains NEGATIVE in our quant models on the shortest duration. The best performing sector on Friday was Utilities +0.43% on the day and +13% on the year.

As usual, we are seeing the interconnected follow through this morning from global markets as Taiwan is down -2.4%. Taiwan is an important geography in the global technology food chain, so is seeing some of the follow through from U.S. technology stock weakness on Friday. As well, having been closed since Wednesday, both the bird flu fears are being reflected in the Taiwanese market as is an increase in North Korean sabre rattling.

The latest from North Korea this morning is that there are signs the country is preparing for a fourth nuclear test. This is based on South Korean intelligence that is showing increased movement of vehicles and personnel at Punggye-ri. This is the site on North Korea’s northeast coast where the previous three nuclear tests occurred. The prior three detonations occurred in 2006, 2009 and February 12th of this year. Clearly, any additional detonation would be a notable acceleration of activity.

In terms of positives related to the North Korean situation, they received their strongest, although also most subtle rebuke, over the weekend from the Chinese. Chinese President Xi Jinping was speaking at the three-day Boao Forum for Asia and said:

“No one should be allowed to throw a region and even the whole world into chaos for selfish gains.”

This is notable in that there is strong support for North Korean within the Chinese People’s Liberation Army, so Jinping is going out on a limb.

The head of the International Monetary Fund Christine Lagarde went less out on a limb when she strongly encouraged Japanese monetary actions over the weekend and called the latest move from Japan a “welcome step”. Her statement is a precursor to newly anointed Treasury Secretary Jack Lew’s first strip to Europe where he is expected to encourage, are you ready for this, more government spending. Keynesians of the world unite!

In the short run, accelerating government spending in Europe would have the likely side effect of expanding deficits. This morning, we can actually see real time the impact of not reducing spending in Europe on government bond yields. Portugal’s Supreme Court rejected cuts in state and pensions and cuts in public sector wages and as a result peripheral bond yields are spiking with Spain and Italy backing up 4.7% and 4.3%, respectively.

Given all of the negative global macro events on the horizon this morning, we have a number of potholes to seemingly avoid so that domestic equity returns can continue their upward climb. The caveat being that the chief risk may be staring at us in the mirror. As Benjamin Graham once said:

“The investor’s chief problem – and even his worst enemy – is likely to be himself.”

Indeed.

Our immediate-term Risk Range for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, VIX, and the SP500 are now $1548-1595, $104.18-108.31, $82.48-83.44, 94.62-98.71, 1.71-1.85%, 12.31-14.55, and 1547-1573, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research