TODAY’S S&P 500 SET-UP – April 18, 2013

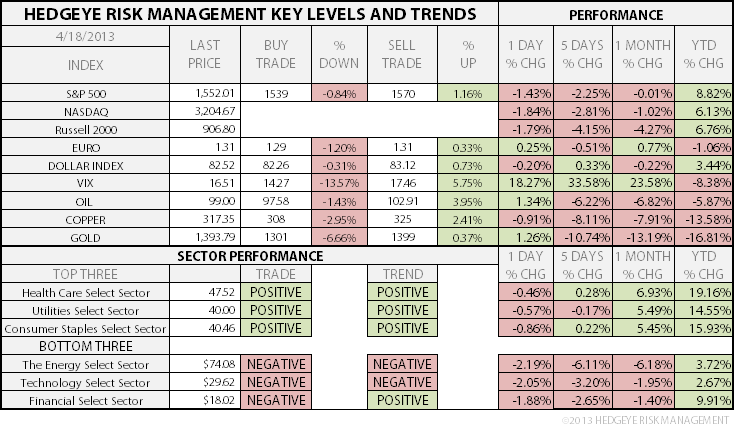

As we look at today's setup for the S&P 500, the range is 31 points or 0.84% downside to 1539 and 1.16% upside to 1570.

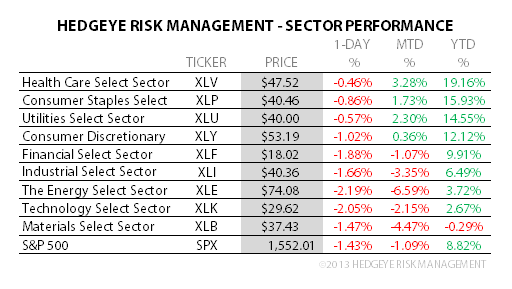

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

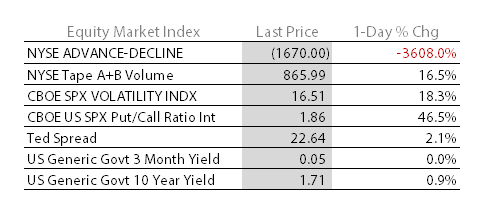

- YIELD CURVE: 1.48 from 1.47

- VIX closed at 16.51 1 day percent change of 18.27%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Init Jobless Claims, April 13, est. 350k (est. 346k)

- 8:30am: Cont Claims, April 6, est. 3.075m (prior 3.079m)

- 9am: Fed’s Kocherlakota speaks in New York

- 9:30am: Fed’s Lacker speaks on credit in Charlotte, N.C.

- 9:45am: Bloomberg Economic Expectations, April (prior -4)

- 9:45am: Bloomberg Consumer Comfort, April 14 (prior -34)

- 10am: Philadelphia Fed, April, est. 3.0 (prior 2.0)

- 10am: Leading Indicators, March, est. 0.1% (prior 0.5%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 11am: Fed to purchase $2.75b-$3.5b in 2020-2023 sector

- 11am: Bank of Canada’s Carney speaks in Washington

- 12pm: Fed’s Raskin speaks in New York

- 1pm: U.S. to sell $18b 5Y TIPS

- 4:15pm: Asmussen, Rehn, Dijsselbloem speak in Washington

GOVERNMENT:

- 10am: Senate Armed Svcs Cmte hears from Dir. of Natl Intelligence James Clapper, Defense Intelligence Agency Dir. Michael Flynn on threats

- 10am: Senate Health and Labor Cmte hears from Labor Sec. nominee Thomas Perez at confirmation hearing

- 11am: President Obama speaks at interfaith service in Boston

- 11:30am: House Speaker John Boehner, R-Ohio, holds briefing

- 1pm: State Dept hears public’s final comments on Keystone, which would carry tar sands from Canada to U.S. Gulf Coast

- House to vote on H.R. 624, Cyber Intelligence Sharing and Protection Act, which White House threatened to veto

WHAT TO WATCH

- G-20 draft affirms pledge to avoid competitive devaluations

- Herbalife unlikely to hire new auditor before investor meeting

- PBOC’s Yi says yuan trading band to widen in near future

- Japan March exports exceed analyst ests. after yen slide

- Wells Fargo urges judge to dismiss U.S. mortgage loan fraud suit

- SEC to move past financial crisis cases under new chairman

- American Express profit beats est. as card spending climbs

- SEC sues Schottenfeld trader Mancuso over Goffer insider tips

- Biggest cinemas delay ‘Iron Man’ ticket sales in Disney dispute

- Explosion hits Texas fertilizer facility, unknown number dead

EARNINGS:

- BB&T (BBT) 5:45am, $0.68

- WESCO International (WCC) 6:15am, $1.14

- KeyCorp (KEY) 6:17am, $0.19

- Fifth Third Bancorp (FITB) 6:30am, $0.39

- AutoNation (AN) 6:45am, $0.64

- Hubbell (HUB/B) 6:58am, $1.09

- Danaher (DHR) 6am, $0.76

- UnitedHealth (UNH) 6am, $1.14 - Preview

- Morgan Stanley (MS) 7:15am, $0.56 - Preview

- Sonoco Products (SON) 7:30am, $0.53

- Verizon Communications (VZ) 7:30am, $0.66 - Preview

- Fairchild Semiconductor (FCS) 7:30am, $0.05

- PrivateBancorp (PVTB) 7:30am, $0.29

- Watsco (WSO) 7:30am, $0.33

- Baxter International (BAX) 7am, $1.05

- Omnicom (OMC) 7am, $0.75

- People’s United Financial (PBCT) 7am, $0.18

- Penn National Gaming (PENN) 7am, $0.65

- PepsiCo (PEP) 7am, $0.71 - Preview

- Philip Morris International (PM) 7am, $1.34 - Preview

- TransForce (TFI CN) 7am, C$0.26

- Alliance Data Systems (ADS) 7am, $2.52

- Pool (POOL) 7am, $0.05

- Snap-on (SNA) 7am, $1.34

- PPG Industries (PPG) 8:11am, $1.54

- Syntel (SYNT) 8:30am, $1.03

- Amphenol (APH) 8am, $0.86

- Freeport-McMoRan (FCX) 8am, $0.71 - Preview

- Peabody Energy (BTU) 8am, $(0.14) - Preview

- Blackstone Group (BX) 8am, $0.53

- Sherwin-Williams (SHW) 8am, $1.09

- Union Pacific (UNP) 8am, $1.96 - Preview

- Cypress Semiconductor (CY) 8am, $0.01

- Nucor (NUE) 9:01am, $0.24 - Preview

- Home BancShares (HOMB) 9:15am, $0.61

- Ultratech (UTEK) 9am, $0.49

- Acacia Research (ACTG) 4pm, $0.50

- Align Technology (ALGN) 4pm, $0.23

- Cubist Pharmaceuticals (CBST) 4pm, $0.32

- Chemed (CHE) 4pm, no est.

- Chipotle Mexican Grill (CMG) 4pm, $2.13 - Preview

- Hub Group (HUBG) 4pm, $0.42

- Associated Banc-Corp (ASBC) 4:01pm, $0.25

- B&G Foods (BGS) 4:01pm, $0.37

- Google (GOOG) 4:01pm, $10.67 - Preview

- Microsoft (MSFT) 4:02pm, $0.68 - Preview

- Capital One Financial (COF) 4:05pm, $1.62

- E*TRADE Financial (ETFC) 4:05pm, $0.12

- International Business Machines (IBM) 4:05pm, $3.05

- Cepheid (CPHD) 4:05pm, $(0.02)

- Forward Air (FWRD) 4:05pm, $0.39

- Intuitive Surgical (ISRG) 4:05pm, $3.97 - Preview

- Electronics for Imaging (EFII) 4:05pm, $0.32

- EastGroup Properties (EGP) 4:05pm, $0.77

- Restoration Hardware Holdings (RH) 4:06pm, $0.61

- Advanced Micro Devices (AMD) 4:15pm, $(0.17)

- City National (CYN) 4:15pm, $0.92

- Celanese (CE) 4:30pm, $0.78

- Glacier Bancorp (GBCI) 4:30pm, $0.28

- Valmont Industries (VMI) 5:30pm, $2.52

- Western Alliance Bancorp (WAL) Aft-mkt, $0.21

- Cytec Industries (CYT) Aft-mkt, $0.87

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Copper Poised to Enter Bear Market as Industrial Metals Slide

- Nickel Rout Seen Easing With Output Costs Breached: Commodities

- Gold Gains as Price Drop Lures Buyers, Economic Data Falls Short

- Goldman’s Contrarian Currie Foresaw Gold Collapse Paulson Missed

- Brent Rises From Nine-Month Low; No Emergency OPEC Talks Seen

- Copper Set to Enter Bear Market on Demand Concern: LME Preview

- Gold Tumble Stokes Demand From Indian Bazaars to Chinese Malls

- Gold’s Worst Plunge Since 1983 Ends 12-Year Bull Run: Timeline

- Palm Oil Advances as Decline to Lowest This Year Seen Excessive

- Gold’s Deviation to Stocks Tips Equities Rally: Chart of the Day

- Oil Firms Break Promise on Biofuels as Chevron Defies California

- BHP Billiton Cuts CEO Pay as Mining Industry Profits Decline

- China’s Poultry Feed Demand to Slump 20% on Bird-Flu Outbreak

- Copper’s Drop ‘Not Sustainable’ Near Term, NAB’s Knight Says

CURRENCIES

GLOBAL PERFORMANCE

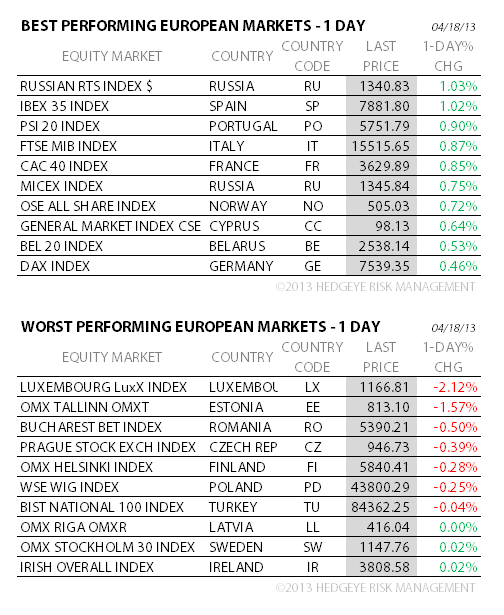

EUROPEAN MARKETS

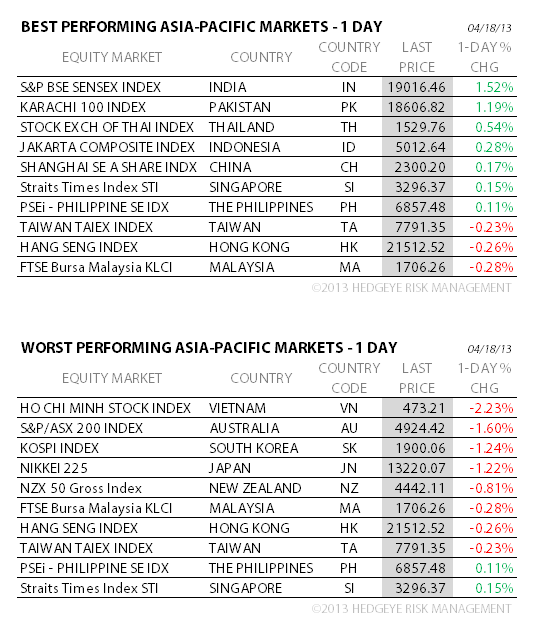

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team