Volume weaker while number of transactions picked up slightly in Q1

Upper upscale (UUP) & Luxury Transaction Trends for Q1 2013

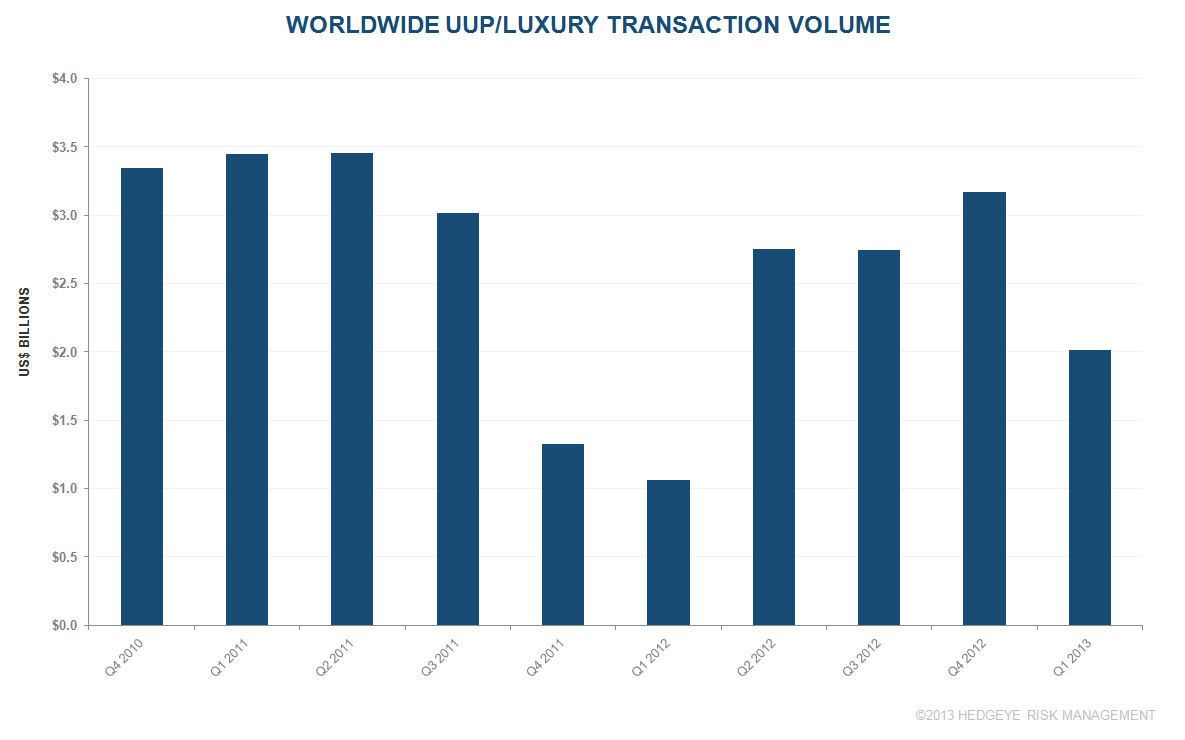

- Q1 2013 worldwide hotel transaction volume (UUP & Luxury brands) was $2.0 billion, down from Q4 2012's $3.2 billion but higher than Q1 2012's $1.1 billion.

- The number of US luxury/UUP hotel transactions was 7 in Q1 2013 compared with 9 in Q4 2012 and 7 in Q1 2012.

- The number of non-US luxury/UUP hotel transactions was 7 in Q1 2013 compared with 3 in Q4 2012 and 4 in Q1 2012.

- REITs were very active and there was a spike in portfolio deals.

- Relative to a two-year trailing average, US average price per key (APPK) in the UUP segment gained 7% at $280k. Non-US APPK in the UUP segment fell by 10% to $287k; however, IHG received a solid >$1MM APPK for its sale of the InterContinental London Park Lane.

Delinquency rate

- According to Fitch, the hotel delinquency rate in March was 7.71%, lower than the 8.87% seen in December. The delinquency rate remains well below the relative high of 14% seen in Q3 2011.