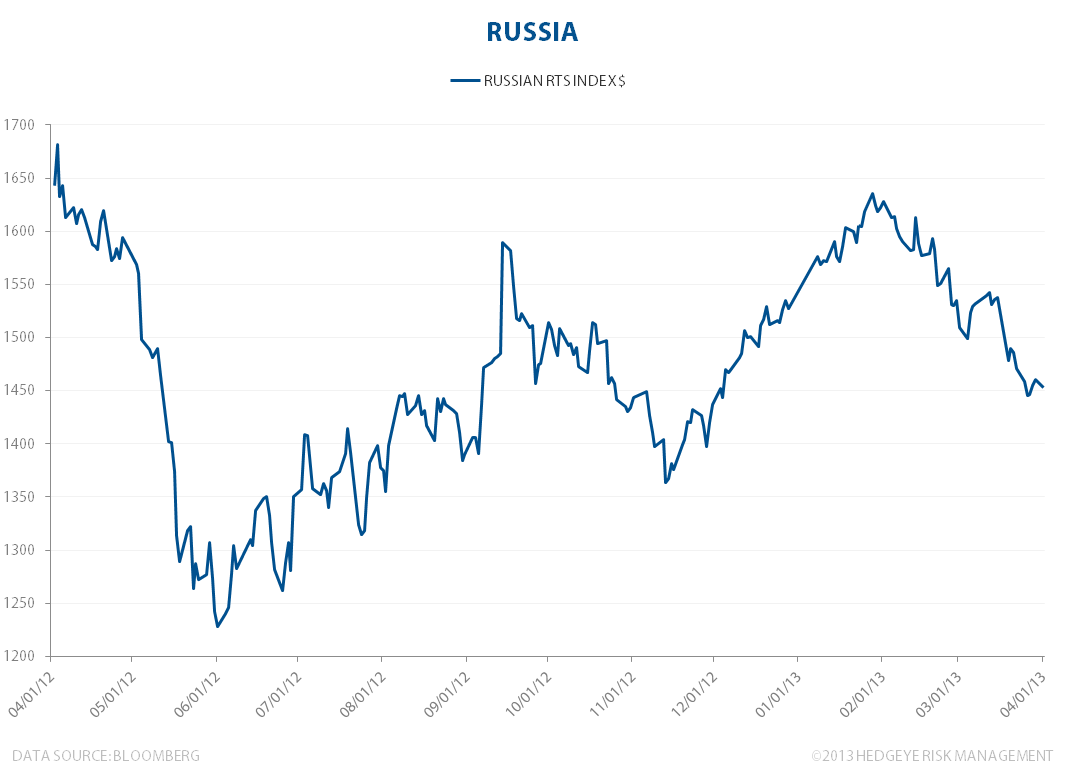

Russia's stock market continues to be one of the worst performing in the world with the RTS Index down another -0.93% to start off the month of April. The RTS Index is down -11.6% since hitting its year-to-date high in January. Comparatively, the S&P 500 is up +9.5% year-to-date and closed at a new all-time high yesterday.