TODAY’S S&P 500 SET-UP – April 1, 2013

As we look at today's setup for the S&P 500, the range is 16 points or 0.84% downside to 1556 and 0.18% upside to 1572.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.62 from 1.61

- VIX closed at 12.7 1 day percent change of -3.42%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:58am: Markit US PMI Final, March, est. 55.2

- 10am: Construction Spending M/m, Feb., est. 0.8% (prior -2.1%)

- 10am: ISM Manufacturing, March, est. 54.2 (prior 54.2)

- 10am: ISM Prices Paid, March, est. 59.5 (prior 61.5)

- 11am: Fed to buy $2.75b-$3.5b in 2020-2023 sector

- 11:30am: US to sell $35b 3-mo., $30b 6-mo. bills

- U.S. Rates Weekly Agenda

GOVERNMENT:

- Washington Week Ahead

- Rule governing high-risk loans takes effect; may change how FDIC-insured banks invest in CLOs

- USTR releases annual assessments of global trade barriers, incl study on technical, health, safety trade restrictions

- Homeland Security to begin cutting staffing hours

- FAA will begin furloughing staff, closing more than 230 control towers at smaller and midsize airports

WHAT TO WATCH

- Federal court judge dismisses civil claims against U.S. banks over Libor manipulation; rules some commodities-related suits may proceed

- Verizon sued for $2.85b in debt, interest from Idearc spinoff

- Dell said to consider Blackstone LBO with CEO guarantee

- Proxy statement has PC sales falling by $10b over 4 years

- Chesapeake names Dixon acting CEO, to hold conf. call on ops

- Beijing, Shanghai boost home curbs as China acts to cool mkt

- Wal-Mart to spend 500m yuan ungrading Chinese stores, China National Radio says

- All Nippon Airways plans for June restart of Dreamliner flights

- Boeing canceled test flight of 787, Seattle Times says

- Cerberus may begin more formal steps in Freedom Group sale

- Exxon to excavate Pegasus oil pipeline to find cause of leak

- Google is biggest threat to TripAdvisor, CEO Steve Kaufer says in FT

- Panasonic said to be under U.S. probe over bribery: WSJ

- Apple iRadio may be introduced in summer 2013, AppleInsider says

- Tesla turned profitable in 1Q; Model S sales exceeded forecast

- Amazon buying Goodreads book-review site irks author group

- U.S. Weekly Agendas: Finance, Industrials, Energy, Health, Consumer, Tech, Media/Ent, Real Estate, Transports

- North American M&A Agenda

- Canada Weekly Agendas: Energy, Mining

- BOJ Meeting, U.S. Jobs, China Index: Wk Ahead April 1-April 6

EARNINGS:

- Cal-Maine Foods (CALM) 6:30am, $1.40

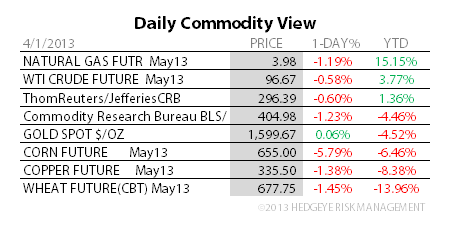

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Corn Heads for Bear Market After U.S. Stockpiles Beat Estimates

- Bullish Bets Rebound at Fastest Pace in Four Years: Commodities

- Rubber Falls Into Bear Market as Stockpiles Swell, Demand Eases

- Indonesia to Review Rubber Exports After Prices Tumble in Tokyo

- Brent-WTI Crude Spread Widens as Exxon Shuts Pipe to Texas

- Spot Gold Little Changed as Silver Nears Bear-Market Threshold

- Copper Drops to 8-Month Low in Shanghai on China Manufacturing

- Hedge Funds Backing $100 Crude Lift Bullish Bets: Energy Markets

- Asia Gasoil Contango Narrows; Fuel Oil Crack Drops: Oil Products

- Mitsubishi Materials to Cut First-Half Copper Output by 6.8%

- Palm Oil Drops to Two-Month Low as Europe Crisis to Curb Demand

- Russia Sets Minimum Prices for Grain Purchases for Stockpiles

- China Manufacturing Rises at Faster Pace in March, Gauges Show

- Coffee Exports From Indonesia’s Sumatra Fall as Inventories Drop

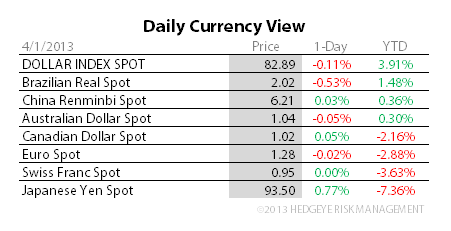

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team