"May you live in interesting times."

-Reputed Chinese curse

It has been an interesting start to the year, to say the least, for the consumer staples sector. The sector's leadership status in a strong tape is certainly an unfamiliar and perhaps uncomfortable position for many investors.

In review, another month in the books and another month of out-performance for our coverage. On average, consumer staples stocks rose 4.8% in March, with only the household and personal care sector and the tobacco sector lagging the S&P's +3.6% rise during the month.

Packaged food continued its strong performance (+7.0% in March) in the wake of the Heinz transaction, lagging only the protein sector (+9.0%) in terms of monthly performance.

We continue to struggle (based on our conversations with clients it seems many dedicated staples investors share the sentiment) with valuation. However, we recognize that valuation in and of itself is not a catalyst and that valuation may not matter for periods of time, perhaps extended periods of time. The simple fact is that a number of staples names have outstripped the multiple that we are comfortable paying for the cash flow stream, even considering earnings upside from potential margin improvement driven by lower commodity costs and improvements in business momentum driven by improved consumption trends. That doesn't mean that we are in a hurry to run out and short everything, but we caution investors to recognize that at some point, valuation will matter.

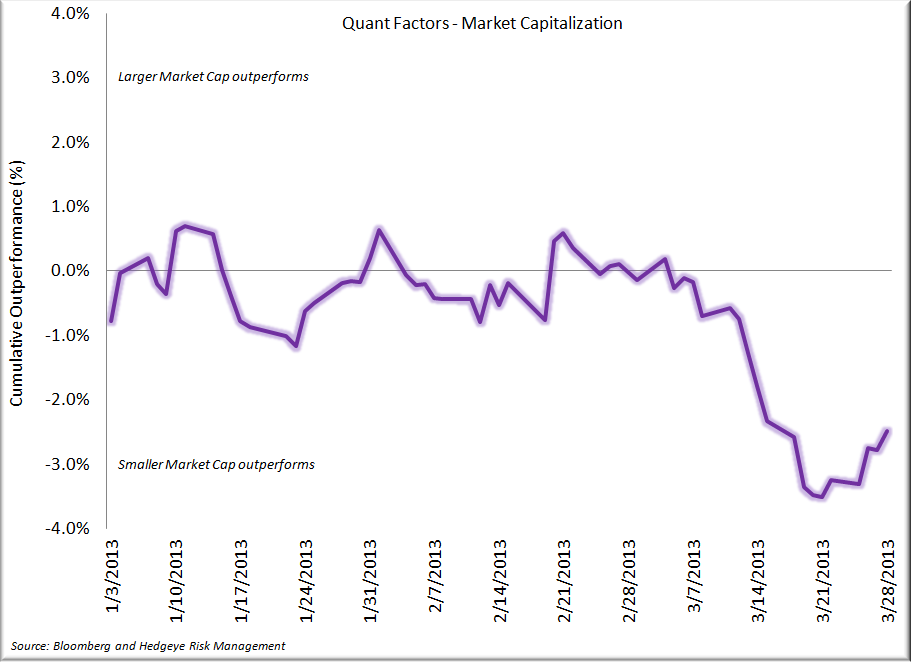

This month we have added a look at several quantitative factors in relation to the staples sector. Keep in mind that all these factors are relative within staples (i.e. smaller capitalization does not meet the technical definition of small cap, but rather represents a name within the lower half of the cap spectrum within staples).

Based on the above analysis, we can develop several themes in terms of what has worked within the staples sector:

- In March, lower beta (lower growth, perhaps 2012 laggard) outperformed higher beta names

- Higher short interest has been a consistent out-performer in 2013

- Smaller capitalization names had a very good month in March

- Dividend yield doesn't tell us much of a story - lower yield had a period of out-performance that has since reversed

- Higher debt to EBITDA has been a consistent outperformer, likely representing outperformance of lower "quality" names

Bear in mind, the performance of the staples sector has largely been absent any significant, positive EPS revisions. Further, absent any material change in business momentum or margins, consensus estimates should head lower on the strength of the dollar to the extent a company has businesses outside the U.S. While we acknowledge the impact of translating a set of results from one currency to the next is largely irrelevant to the value of a business, optics do matter.

Revisiting an analysis from last month, we see that performance was balanced across PE quartiles, with the modest relative under-performance in higher multiple names largely caused by BNNY's monthly performance (-9.5%). In fact, it was nearly impossible to find a consumer staples stock that didn't go up in the month of March.

Similar to last month, multiples expanded across all quartiles.

In keeping with a familiar theme, the yield spread between the 10 year treasury and the XLP has widened in recent days, making the XLP marginally more attractive to investors seeking yield. Further, we think it is possible that yield bearing assets in the U.S. (XLP and consumer staples stocks included) might see inflows to the extent that confidence in the European banks has taken a hit in the wake of the Cyprus situation.

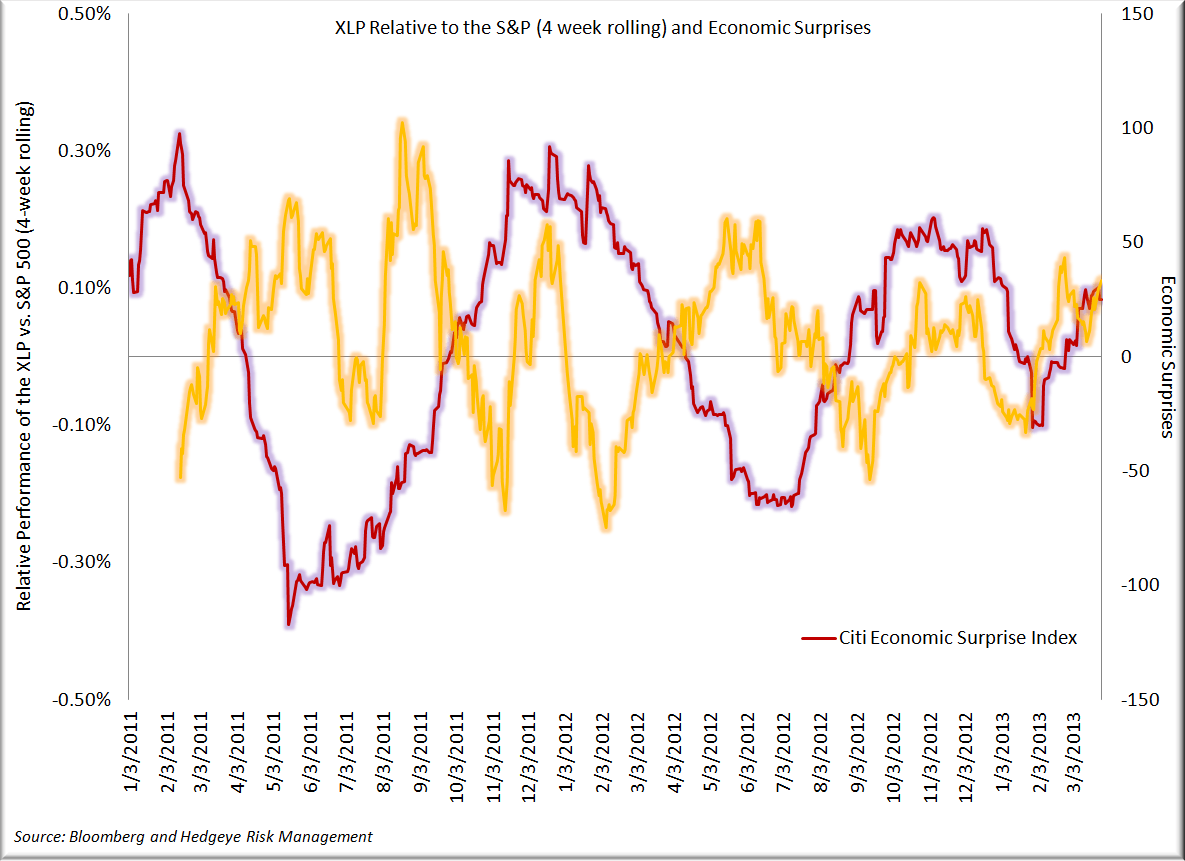

Finally, taking a look at the performance of the XLP in relation to a basket of economic indicators and the performance versus consensus shows us that the broader economy continues to surprise to the upside (consistent with Hedgeye's macro call) driving performance of the XLP.

Where does that leave us?

Valuations suggest that we should stick to the sidelines, but it is difficult to ignore/fight improvements in the economy and money flows. Therefore, we are going to stick with value where we can find it and our preferred list remains unchanged:

- ADM

- BUD

- CAG

- NWL

Our least preferred list could be much longer based solely upon our concerns surrounding valuations in the sector, but for the moment we will add two names as we approach Q1 EPS:

- KMB

- GIS

- TAP

- CL (new)

- K (new)

Enjoy the rest of your weekend.

Rob

Robert Campagnino

Managing Director

HEDGEYE RISK MANAGEMENT, LLC

Matt Hedrick

Senior Analyst