This note was originally published March 27, 2013 at 15:04 in Retail

Last week we saw a sequential downtick in both athletic apparel and footwear, which was fairly consistent with the tough week that retail had in aggregate. In fact, it was not a bad showing at all given that the ICSC numbers put up the biggest sequential slowdown relative to prior-year levels in at least two years. The saving grace for both apparel and footwear is that price point integrity remains extremely high, with footwear (Average Sales Profits (ASPs) up in the +10% range, and apparel up in the teens. A negative swing in ASPs would likely coincide with heavy promotional activity -- and we're not seeing it.

No surprises as it relates to winners and losers by brand. Nike and Jordan still dominating. Adidas and Reebok still trying to find a bottom, and Under Armour making very slow and steady improvement.

Source: SportscanINFO, NPD, and Hedgeye

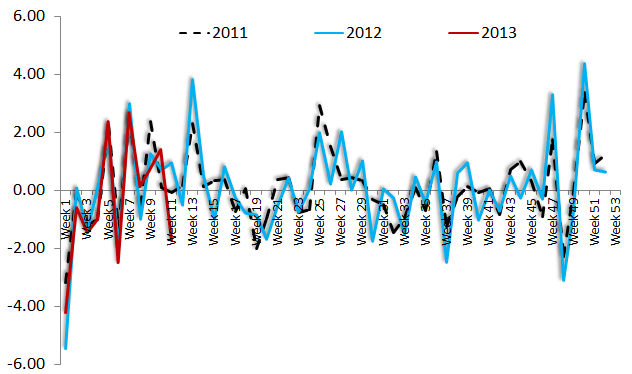

ICSC RETAIL SALES INDEX (Sequential % Change -- 80 Store Sample)

Source: International Counsel of Shopping Centers

Source: SportscanINFO, NPD, and Hedgeye

Source: SportscanINFO, NPD, and Hedgeye