Pinnacle Foods is offering 29 million shares of common stock (4.35 million additional shares in the overallotment) in an initial public offering set to price on Thursday the 28th. The Blackstone Group is the selling shareholder and will continue to own 68% of the shares outstanding subsequent to the IPO. The shares are expected to be offered in the range of $18-$20 per share, with a total market capitalization of $2.227 billion at the middle of the range assuming exercise of the overallotment (all of our math does). Proposed ticker is "PF".

Well-Known, Center of the Store Brand Portfolio

Pinnacle Foods is a single geography (the U.S. represents $2.454 billion of the company’s $2.478 billion in 2012 sales), center of the store grocery company that operates in 12 major product categories (as defined by the company):

The company claims leading positions in 10 of the 12 major product categories in which it competes, though we think the definition of “product category” has to be tortured a bit to make that claim. For example, “frozen complete bagged meals” (25.1% share of market, #2 player according to the company) seems like a subset of “frozen” that is somewhat arbitrary. Further, within the Duncan Hines Grocery Division, we accept the company as the market share leader (31.3%) in shelf-stable pickles, but don’t see the category as particularly attractive.

We think investors should view the company as a pure play on the center of the grocery store or, said another way, the section of the grocery store with the least attractive growth profile and margin structure.

Company May Struggle to Grow Revenue

The company acquired Birds Eye Foods in December of 2009, adding approximately $1 billion in net sales to the company. In the years subsequent to that acquisition (’11 and ’12), the company grew revenues +1.3% and +0.4% respectively – given the categories in which it competes, we have a difficult time seeing the company with anything more than 1-3% organic revenue growth profile over time and that may be generous on our part. Our forecast for 2013 is 1.5%.

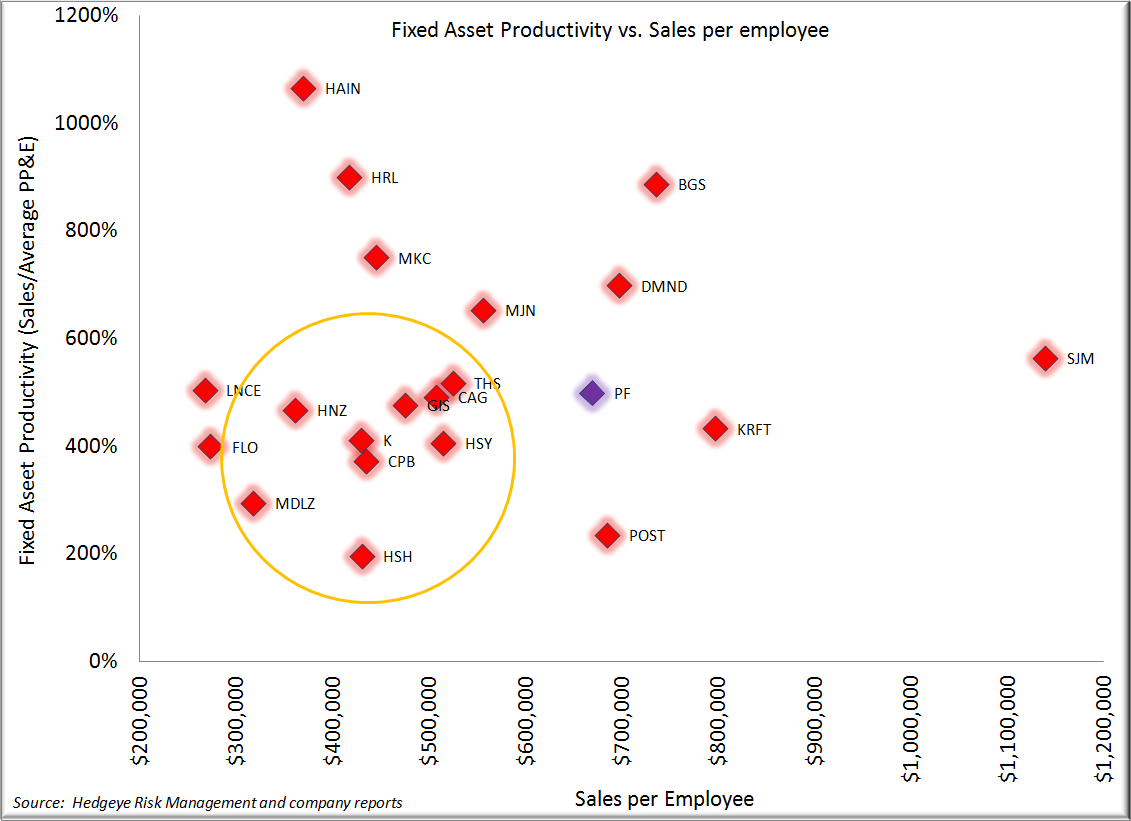

Based on our preferred metrics, we see the company as a well-run asset with brands that are well-supported by advertising and R&D (see charts below). Unfortunately, that means that we don’t see much opportunity for SG&A leverage going forward, particularly in light of our modest top line assumptions for the company.

Margin Opportunities?

The company has cited on each of its last two quarterly conference calls a moderating cost inflation environment. This commentary is largely consistent with the sentiment coming out of CAGNY across consumer staples. Further, the company does have initiatives in place that focus on productivity savings in procurement, manufacturing and logistics that can serve to magnify any benefit to the gross margin line that might accrue from lower input costs.

That is a good thing, as we think any operating margin expansion is likely going to have to come from the gross margin line, and we do see some opportunity there as we move through 2013. The company faces some easy gross margins comparisons in 1H ’13, and we expect that the moderating commodity environment that we are currently in will start to benefit gross margins in 2H ’13, so we see a full year opportunity for gross margin expansion for the company – our assumption is 50+ bps of gross margin expansion in ’13. When we couple our gross margins assumption with our modest top line forecast and the lack of leverage in SG&A and other line items, our forecast is for EBIT to grow 5.5% in ’13 (approximately $100 million of EBITDA get us to a 2013 EBITDA forecast of a little more than $450 million).

What's it worth?

At $19 per share, the company is trading at 9.3x EV/EBITDA with the broader food group at 11.1x, so a discount to the broader group and one that we feel is deserved. We struggle to see material upside given the company's margin structure and brand portfolio and the current state of the grocery industry. Having said that, a couple of non-financial considerations may drive the valuation beyond the point we see as reasonable. To begin with, the yield at $19 will be 3.79%, not outsized, but chunky enough to provide support for the shares in the $18-19 range, limiting the downside.

The company also has about $1 billion in NOLs, shielding the company from cash taxes through 2015 - however, the S-1 doesn't make it clear that the NOLs would survive incremental sales by Blackstone (change of control), making the value difficult to determine. As it currently stands, the NOLs will preserve about $80-$85 million per year (assuming 100% utilized against a 36% tax rate) of income from taxes, through 2015 and "modest" amounts thereafter. We should point out that Spectrum Brands (SPB) has NOLs that are of substantially longer duration than those at PF that the market doesn't seem to value at all, so we would be careful basing an investment decision on the market's ability to correct assign a value to those assets.

The company may benefit from a dearth of small and mid-cap names in the packaged food space. With a market capitalization of approximately $2.22 billion at the mid-point of the proposed offering range, PF will lie between POST (market cap $1.36 billion) and HSH ($4.16 billion) on the market cap spectrum. HAIN ($2.83 billion) is a different animal given its position in the faster growing natural and organic space.

Highly Levered Asset

Even subsequent to the repayment of approximately $550 million of debt (mostly 9.5% coupon debt, so expensive, to be sure), the company will still be a highly levered asset, trading at 4.5x net debt to trailing 12 months EBITDA. In 2012, FCF (cash from operations less capital expenditures) was $124.6 million – out of that, the company will have to pay approximately $84.4 million in dividends (proposed dividend is $0.18 per share, quarterly), leaving approximately $40 million per year to pay down debt (conservatively, as it assumes no growth). The company is a deleveraging story, though certainly not a rapidly developing one.

The level of debt currently on the balance sheet will likely make it difficult for the company to pursue any acquisition of meaningful size. At 4.5x net debt to EBITDA, PF is near the level where most consumer staples companies end up subsequent to doing a deal. Any acquisitions are likely to be relatively small in nature and not transformational, and that is even before taking into account an elevated valuation environment in the staples space.

Timing is everything they say

The Pinnacle IPO has been threatened for some time – beginning in early 2012. But, as they say, timing is everything and Blackstone has the wind at its back with takeover speculation rampant in the consumer staples space, strength in the broader market and valuations at a multi-year high. Further, and though no one could likely have timed the IPO so fine, the style factors that have been working in the market recently are high short interest (not applicable), low P/E (suggesting low growth) and high debt/EBITDA – or basically everyone’s short book and Pinnacle Foods. Bottom line, there is a good bit supporting this IPO.

While we expect some speculation that Pinnacle could be a target, we don’t see it right now. As we mentioned above, low-growth, center of the store company doesn’t check off any of the boxes that the bigger companies in the space are looking for – emerging market exposure, health and wellness, and categories with pricing power, to name a few. KRFT is a likely consolidator of grocery assets going forward, but that was a pretty easy call to have been made before the IPO.

Where does that leave us?

PF is a highly-levered, low-growth asset trading at only a slight discount to an already inflated peer multiple of EBITDA, and that is giving credit in our forecast to both top-line growth and gross margin expansion. We don't see the name a particularly compelling long-term investment though neither do we see significant downside from the proposed offering price range. Finally, buying from a private equity firm that seems to have timed the market well with regards to its sale doesn't strike us as a particularly good idea.

-Rob

Robert Campagnino

Managing Director

HEDGEYE RISK MANAGEMENT, LLC

Matt Hedrick

Senior Analyst