This note was originally published March 21, 2013 at 21:41 in Retail

There are three things we were looking for in Nike’s quarter; proof that 1) Nike is gaining share/driving consumer demand across its portfolio, 2) Gross Margins are improving at a rate well ahead of consensus expectations, and 3) that it is achieving these things with disproportionately less capital invested in its business (ie driving returns higher).

Well, Nike showed us every one of these, topped our EPS estimated by a penny, and blew out the Street by $0.06ps. No changes to our above-consensus EPS estimates our thesis. Nike remains a top pick.

Some important points:

North America En Fuego. As it relates to demand, we saw North America sales up 18%, which was on top of a 17% growth rate last year. Importantly, futures were up 11% despite being up at a colossal rate of 22% this quarter last year. Think about it like this -- try to find another company with 45% share in its category that is growing its top line at a mid-teens rate while improving margins and lessening capital intensity along the way. Let us know what you find, we think you’ll come up dry.

China has definitely bottomed. Don’t let management’s caution fool you. They specifically made it a point to keep estimates grounded and said that that they still have a lot of wood to chop. But futures going from -6% and -5% over the past two quarters to +4% in 3Q is proof positive that this business has at least found bottom, and is likely trending higher once again.

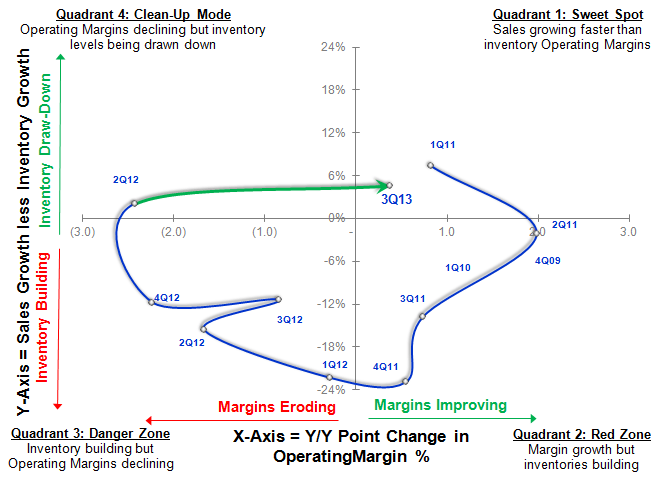

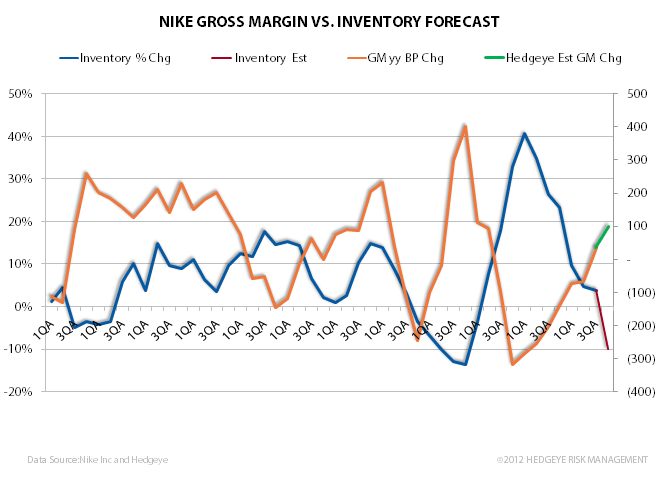

Inventories still improving – driving better margins. Though pricing and easing raw materials costs helped gross margins, the spread between inventory and sales growth is getting better and will continue to drive gross margins higher. This is probably best evidenced by our SIGMA chart, where it shows Nike making a big move into the upper right quadrant of this analysis. Over time, triangulating margins with capital efficiency explains away 92% of stock moves in retail. Translation – it matters.

We think that the spread between inventories and margins will continue to diverge well into FY14

Here’s our previously-published comments on our expectations for 3Q.

NKE: Ahead of the Print

We think that the Q is in good shape, but if there are any fireworks we’re confident enough in our thesis to support the name.

Conclusion: Our analysis suggests that Nike’s quarter is in good shape. But let’s face it, Nike always manages to light off a firework or two. If that happens to be case on Thursday, we’re confident enough in our underlying thesis that we’d support any weakness.

Will the quarter be a blowout? Not exactly. We’re modeling $0.72 vs the Street at $0.67. Nice upside -- but not huge. We’re about in line with the Street on the top line at about 11%, but we’re 50bp higher on the gross margin line. We think that’s fair given the easing product costs flowing through the P&L as well as 2Q ending with the most favorable inventory position in nine quarters.

Futures: As it relates to futures, bears are calling me with the expected ‘futures are decelerating’ concerns. The company is going against a 22% North American futures number in this quarter, and +18% globally. It doesn’t take a genius to figure out that this is a ridiculously tough quarter to comp. On a 2-year run rate, a 7% North American or 5% Global futures number suggests an even underlying trend. We think Nike comes in 2-3 points above those levels. On a go-forward basis, keep in mind that after this quarter, we started to see China drop off precipitously. Beginning next quarter, we expect any slowdown in growth in North America to be offset by a rebound in China and an uptick in Western Europe (NKE is about to anniversary the latest downturn there, and FL recently noted a stabilization in Europe).

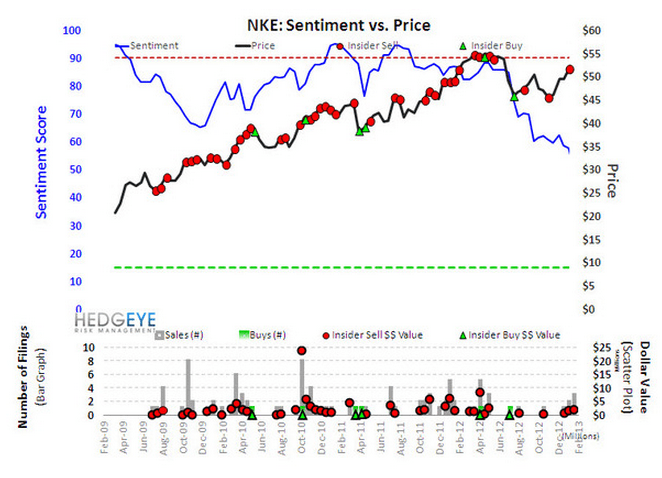

Sentiment is Flat-Out Bad: Lastly, we need to acknowledge sentiment and valuation. We agree that the stock isn’t cheap at 17x earnings. But let’s not forget that sentiment on Nike remains quite bad. Our sentiment monitor, which is based on both sell-side recommendations, short interest and insider trading activity, suggests that Nike is more hated today than almost any time over the past 10-years.