TODAY’S S&P 500 SET-UP – March 22, 2013

As we look at today's setup for the S&P 500, the range is 23 points or 0.25% downside to 1542 and 1.24% upside to 1565.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.67 from 1.67

- VIX closed at 13.99 1 day percent change of 10.42%

MACRO DATA POINTS (Bloomberg Estimates):

- 11am: Fed to purchase $3b-$3.75b notes 2018-2020 range

- 12pm: Revisions to Fed’s industrial production data

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Obama to meet w/ King Abdullah II of Jordan

- 7:30am: Fed Gov. Sarah Bloom Raskin, CFPB Director Richard Cordray, FDIC Chairman Martin Gruenberg speak at Natl Community Reinvestment Coalition conf.

WHAT TO WATCH

- BlackBerry Z10’s U.S. debut marks biggest test of comeback

- Dell go-shop period for other offers expires today

- FCC Chairman Julius Genachowski said to be leaving agency

- Cyprus lawmakers to debate bailout bill as deadline looms

- Euro area said to weigh closing Cyprus banks, asset freeze

- Boeing faulted by 787 investigators for battery fix comments

- Samsung said to be in talks to sell Liquavista to Amazon

- Sharp extends deadline for 2nd Qualcomm payment to June 28

- Citigroup says pay plan holders rejected helped keep Corbat

- Life sale said to shift to strategies; some buyout firms exit

- German business confidence unexpectedly drops from 10-mo. high

- Australia probes pricing by Apple, other tech cos.

- Goldman Sachs raises U.S., Japan growth forecasts

- Deutsche Bank, Goldman miss $129m fee in Evonik IPO snub

- U.S. Spending, Supreme Court, BRICS, AMR: Wk Ahead March 23-30

EARNINGS:

- Tiffany (TIF) 6:59am, $1.36

- Stella-Jones (SJ CN) 7am, C$0.93

- Darden Restaurants (DRI) 7am, $1.01

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Brent Crude Set for Second Weekly Drop to Shrink Premium to WTI

- Gold Seen Extending Rebound as Cyprus Revives Bulls: Commodities

- Biggest Crisis Since 2008 Looms for South African Mines: Energy

- Gold Falls From 3-Week High as ETP Drop Overshadows Cyprus Woes

- Palm Oil Heads for Weekly Gain as Inventories Seen Declining

- Industrial Metals Advance as Economies in U.S., China Improve

- Rubber Declines for Second Week on Yen, Europe Debt Concerns

- China Soybean Imports Seen Lower Than USDA Forecast Amid Delays

- Copper Fees Climb in Shanghai as Metal Seen Moving to Malaysia

- Rebar Declines as Demand Seen Curbed by Slowing Chinese Economy

- Diesel Best Returns in Two Years Waning on China: Energy Markets

- Brazil Gold Allure Puts Australia’s Beadell in Play: Real M&A

- Traders Cut Paulson Gold Favorite on Liquidity: Chart of the Day

- Mistry Sees Palm Rally Through May on Ringgit, Reserves Drop

CURRENCIES

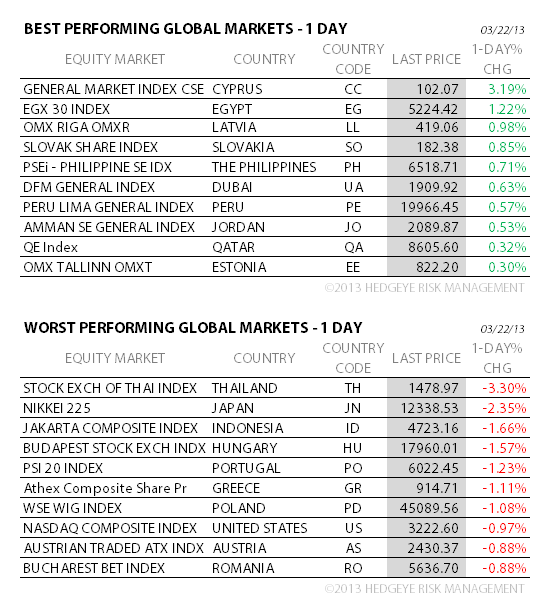

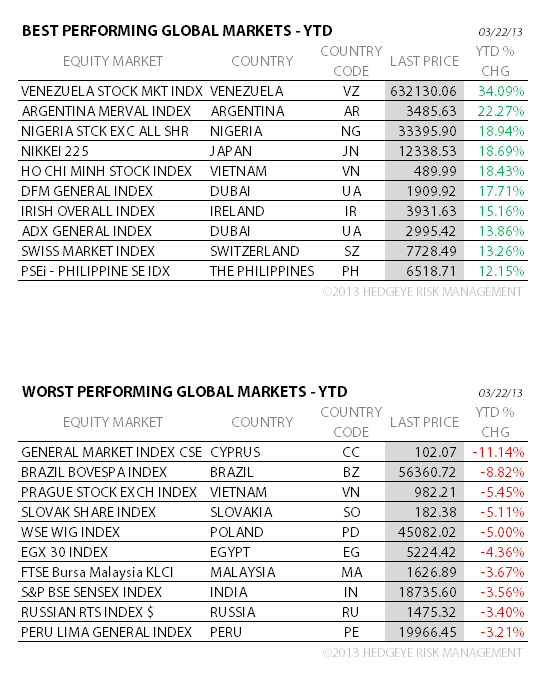

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team