Our Healthcare sector’s recent survey of birth statistics in key US markets shows that births may resume growth in 2013 after persistent annual declines dating back to 2008. We think the rest of the investment community has not yet caught up on this key metric.

Sector head Tom Tobin says this could be the leading edge of a surge in revenues and profits for companies like Mednax (MD).

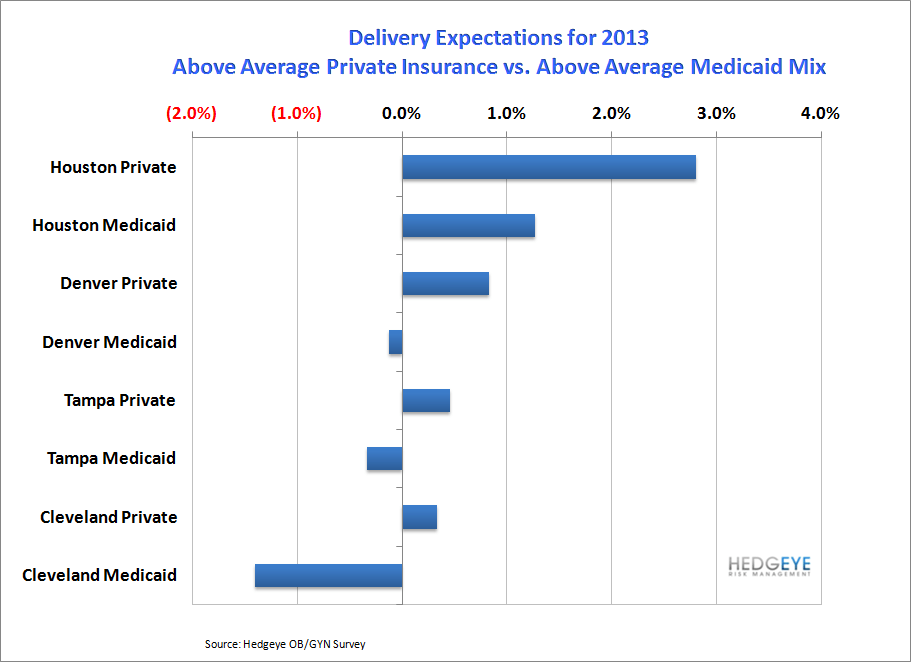

The increase in births will directly benefit MD, who provides neonatal intensive care treatment to premature babies. That increase should be driven by families with private-payer insurance coverage. This is significant for MD: private insurance reimburses MD at roughly three times the rate that Medicaid pays, and MD’s highly fixed-cost structure means increases in revenues will drive greater increases in profits.

Tobin calculates the outsized effect of shifting the payer mix away from Medicaid, and to private insurance. For every 1% move from Medicaid to private insurance, MD stands to gain 1.2% in additional revenues, and 1.5% in profits. Put differently, MD’s cost structure magnifies the profit impact by approximately 50%. The emerging birth trend could turn into a big payday for MD.

MD stock has a pattern of performing well as short interest declines. There was record shorting in the stock at the end of 2012, which has since backed off. If buying volume comes in, MD looks well positioned for a rally on both emerging fundamentals, and on a trading set-up.