Conclusion: Our analysis suggests that Nike’s quarter is in good shape. But let’s face it, Nike always manages to light off a firework or two. If that happens to be case on Thursday, we’re confident enough in our underlying thesis that we’d support any weakness.

Nike remains one of our favorite names right now. We think its fiscal third quarter to be released on Thursday after the close will be another datapoint to support our view that it is gaining share and returns are rising – and there aren’t many other names that are doing both of those two things right now.

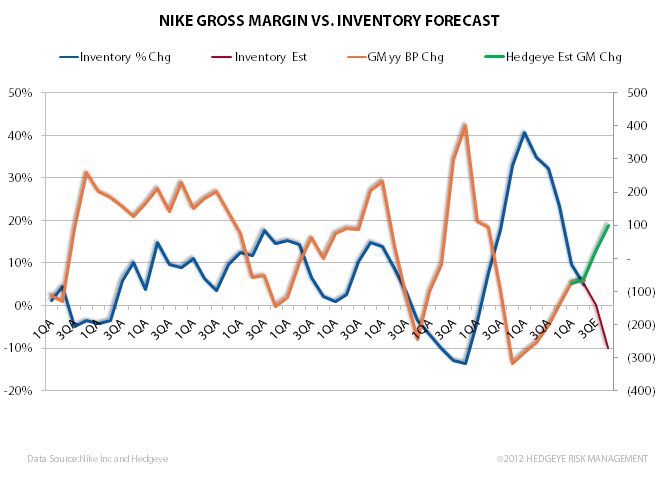

Will the quarter be a blowout? Not exactly. We’re modeling $0.72 vs the Street at $0.67. Nice upside -- but not huge. We’re about in line with the Street on the top line at about 11%, but we’re 50bp higher on the gross margin line. We think that’s fair given the easing product costs flowing through the P&L as well as 2Q ending with the most favorable inventory position in nine quarters.

Futures: As it relates to futures, bears are calling me with the expected ‘futures are decelerating’ concerns. The company is going against a 22% North American futures number in this quarter, and +18% globally. It doesn’t take a genius to figure out that this is a ridiculously tough quarter to comp. On a 2-year run rate, a 7% North American or 5% Global futures number suggests an even underlying trend. We think Nike comes in 2-3 points above those levels. On a go-forward basis, keep in mind that after this quarter, we started to see China drop off precipitously. Beginning next quarter, we expect any slowdown in growth in North America to be offset by a rebound in China and an uptick in Western Europe (NKE is about to anniversary the latest downturn there, and FL recently noted a stabilization in Europe).

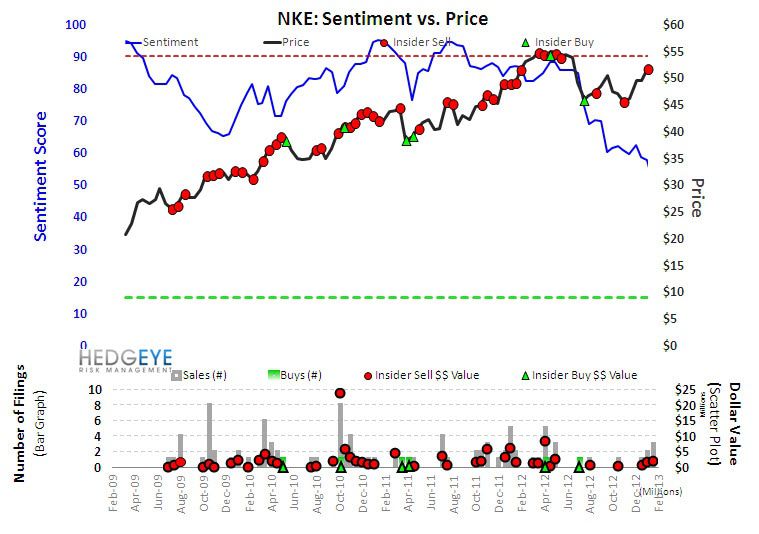

Sentiment is Flat-Out Bad: Lastly, we need to acknowledge sentiment and valuation. We agree that the stock isn’t cheap at 17x earnings. But let’s not forget that sentiment on Nike remains quite bad. Our sentiment monitor, which is based on both sell-side recommendations, short interest and insider trading activity, suggests that Nike is more hated today than almost any time over the past 10-years.