Last Thursday BOE Governor Mervyn King said that “markets determine the level of exchange rate, not us” in response to the Pound’s strong move lower.

Below we provide a refresher on the economic and political developments that have in fact influenced Sterling’s -7.2% slide against the USD year-to-date, performance second worse only to the Japanese Yen (-9.0%) among its G10 brethren.

We suggest that the BOE’s dovish set-up on monetary easing should encourage the Pound Sterling lower, which should put increased downward pressure on the economy as it can’t export its way out of its malaise given its high import dependency. Also, further stoking of inflation through dovish monetary policy should only erode the purchasing power of an already deflated populous.

Lackluster Performance

Britain, like its European neighbors, is struggling with the question of Austerity versus Stimulus. Those mostly on the left (including Labour) suggest that austerity is self defeating, and that by cutting and/or reducing spending during a period of weak demand, it is encouraging economic malaise. Conversely, those to the right (including the Tories under PM Cameron and his Chancellor of the Exchequer George Osborne) suggest that cuts in taxes and spending will revive the private sector (and hiring) and improve the credit rating and therefore lessen the debt and deficit levels and help encourage foreign investment into the country.

We remain in the camp that supports prudent levels of fiscal austerity with directed spending to support job creation. We think, however, that the biggest problem ailing the country right now is the lack of support for a strong Pound from the country’s ruling elite, especially following Moody’s decision on February 22nd to downgrade the UK’s Credit rating one notch to Aa1 from Aaa. In our mind, Mervyn King’s dovish stance on monetary stimulus suggests to us additional downside in the GBP/USD, protracted slower growth, and higher inflation across the island economy over the near to intermediate term.

Under the Hood

While we don’t think Moody’s rate cut is devastating for the credit market, and have suggested in the past that AA is the new AAA, the cut compounds an already perfect storm of fundamental drags hampering the economy, with the threat of rising bond yields only one of them. Here’s what we see:

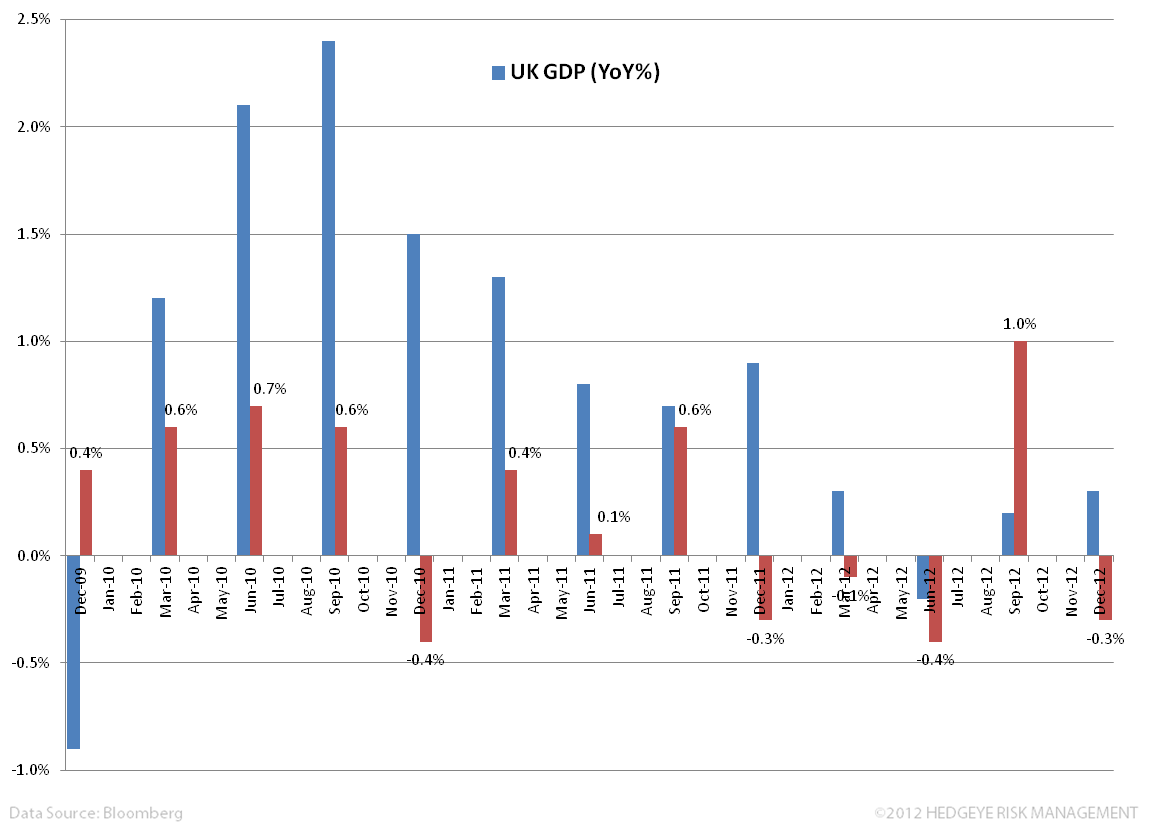

Weak GDP: A starting place to assess the UK is its GDP. Final Q4 GDP came in lower than consensus expectations on a Q/Q basis at -0.3% versus expectations of -0.1% and at 0.0% Y/Y versus expectations of +0.2%. Of note is that 63% of UK GDP is private household spending. As we’ll show below, we think the policy and rhetoric of key government figures, taken with the fundamental drivers of the economy, is choking off economic confidence, and therefore consumer confidence, which should extend the stagnation period or prolong the period until a sustainable economic recovery gains traction. We are below consensus expectations for 2013 of 0.90%.

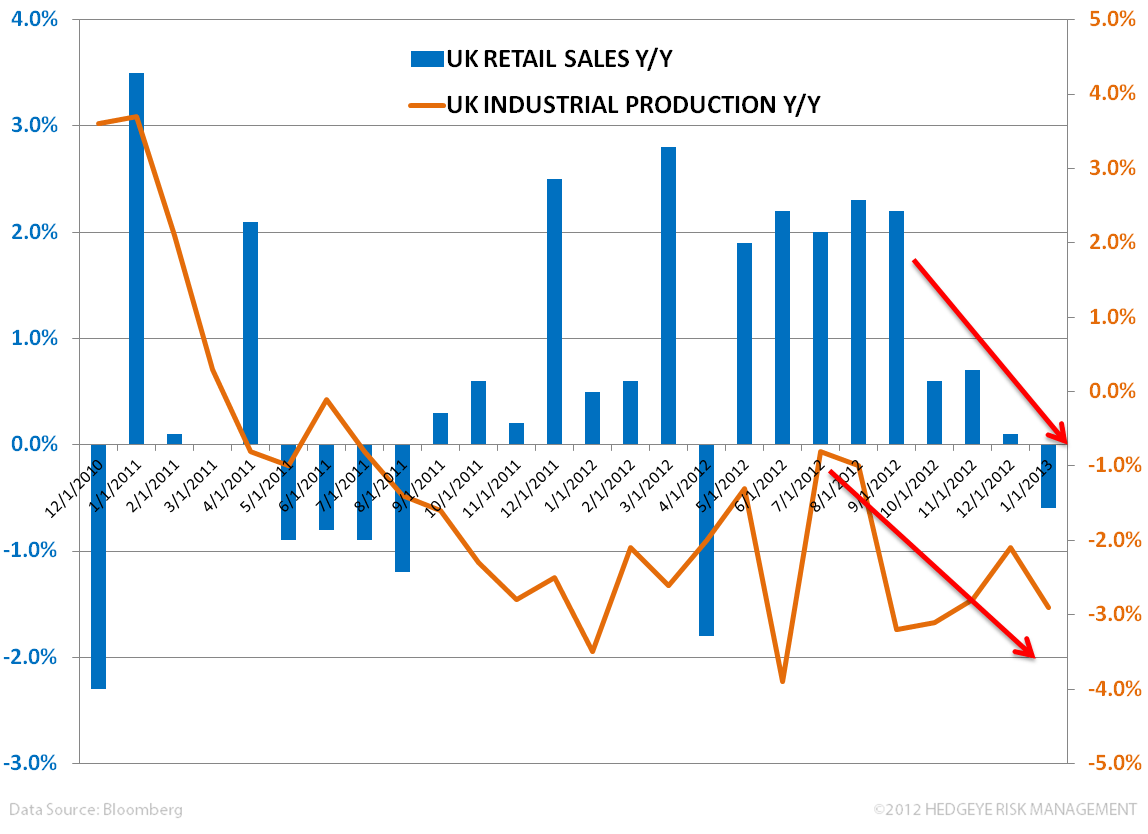

Dumpy Data: From Retail Sales to industrial production, the breadth of recent macro data is headed in the wrong direction. The rollover in economic activity supports the idea that politicians are mismanaging the calculus between austerity and stimulus and driving a decidedly un-virtuous cycle.

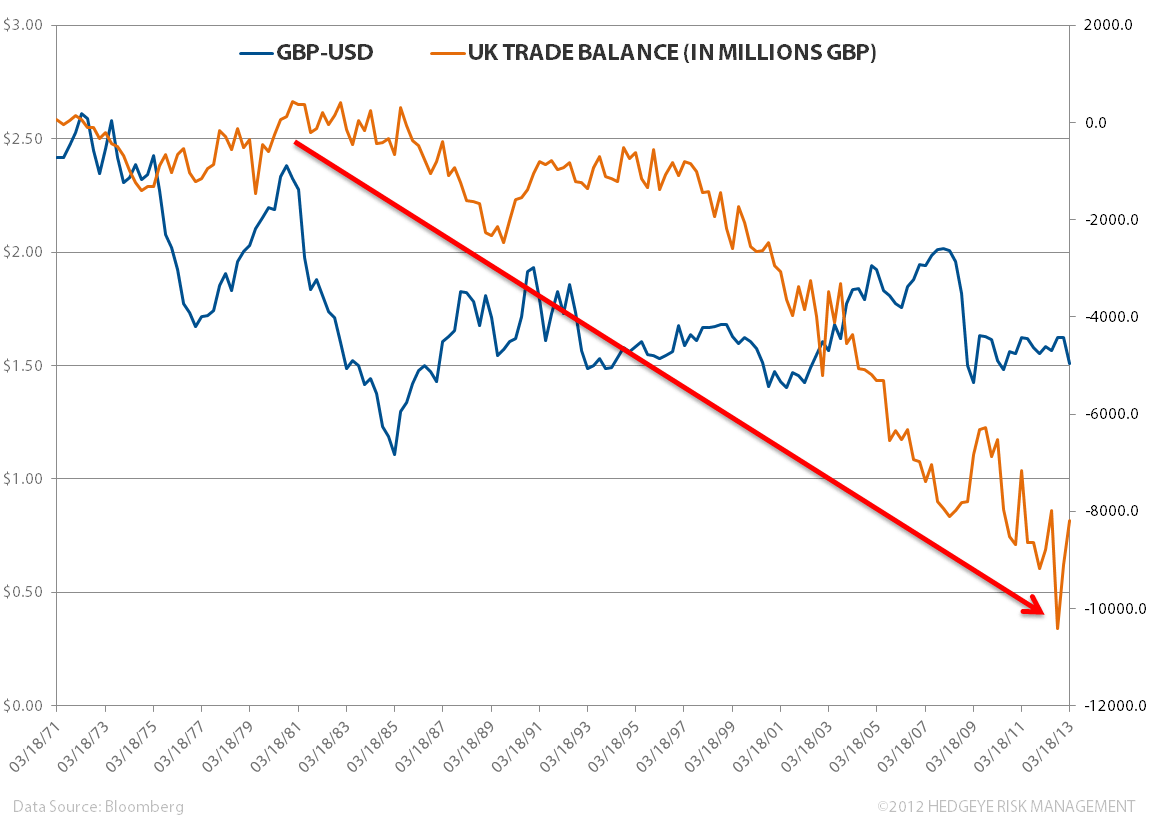

The Fallacy of an Export Recovery: This export camp claims that a fall in the Pound makes British exports cheaper for foreign buyers. While this may be true at face value, a historical look at the current account balance (which is currently in deficit at -3.5% of GDP), shows little correlation between declines in the Sterling and improvements in the trade balance, in fact next to zero (or an r^2 over the past 3 years of 0.174 and 0.038 back to 1971). Further, the export camp leaves out the fact that a weak sterling reduces purchasing power. For an economy 63% levered to consumer spending that buys half of its goods and services from abroad, including that it is a net importer of energy, a weak GBP is a HUGE economic tax, not a benefit.

Inflation Rising: CPI is currently at 2.7% Y/Y and pushing higher. We expect higher import prices through a weaker currency and increased pressure due to elevated and sticky energy costs. This will all put pressure on the BOE overshooting its 2% target rate. The bank has publically said inflation will stay above the target for the next two years. As we show in the chart, CPI is running a full 1.4% above wage increases. Now that’s another tax!

Yields and Deficit/Debt Scares: Is AA the new AAA? …Well maybe. Interestingly, the sovereign bond yields for the USA and France haven’t moved meaningfully (higher) in the wake of a downgrade. We think that given continued uncertainty and slow to contracting growth profiles across the Eurozone, the UK too may not see a meaningful jump in credit spreads. (Fitch and Standard & Poor’s have Britain on “negative watch”). That said, the government is seen struggling to reduce the deficit, which is currently at 7.8% (as Labour calls for more spending), with an elevated debt level at 89% of GDP. Should attention move away from the Eurozone mess, the UK could be in for a real shift of sentiment away from its safe haven status. This could have additional downside risk for the currency.

Savings is the Inverse of Confidence: In the chart below we show another way to represent falling confidence and that’s through the savings rate. The pullback in spending rhymes with increased savings. We’ll leave it to the politicians to see if they can turn around this tide.

Politically Dovish: 3 of the 9 Monetary Policy Committee members, including Governor Mervyn King, have voted for more quantitative easing, as of the last minutes, which should put upward pressure on yields and weaken the Pound. With the 10yr around 2% we could see foreign investors shun the low yield in an environment of currency debasement.

For context, for months David Miles was the lone wolf calling for looser policy. In January King and Paul Fisher joined him, which could tip the balance in favor of increasing the Bank’s current target of £375B. However, the tipping of this balance could once again be disrupted by Mark Carney replacing King in July. We’ll have to wait and watch to see how he comes out of the box.

Sterling Weak: It’s not the Yen, but a close second for the 2nd worst performer YTD versus the USD of the 10 major currencies. Below we outline our key levels.

Matthew Hedrick