“Let no such man be trusted.”

-Shakespeare

According to John Meacham (author of Thomas Jefferson: The Art of Power), that was one of Jefferson’s favorite passages from Shakespeare’s Merchant of Venice – the tragic comedy about a man (Shylock) lending to another man (Antonio) for a pound of his flesh.

Thank goodness for Portia – in the end, she reminded Shylock that he must remove Antonio’s “flesh” (not the blood) and warned him that if he went a hair beyond a pound, “Thou diest and all thy goods are confiscate."

Written at the end of the 16th century (between 1596 and 1598), these were some pretty serious times of debate about debt and default. But looking at today’s consensus fear-mongering about Cyprus screwing its depositors, what has changed? Is the world about to end, again?

Back to the Global Macro Grind…

I realize that’s maybe a little too philosophical for the monkey getting whipped around by the futures this morning. As Meacham himself points out, “Plenty of philosophical men live in abstract regions, debating types and shadows.”

But, my friends, behold! “The rarer sort is the reader and thinker who can see the world whole.” (Jefferson: The Art of Power, pg 47) And our risk management duty this morning is not to freak-out Italian Election style; it’s to see the world for what it is, not what Fear-Dwellers who have been getting run-over shorting US stocks for all of 2013 want it to be.

“To be, or not to be”, scared out of your mind this morning - remains the question. Todd Jordan and I took our wives to see Paul Giamatti in Hamlet this weekend so, admittedly, I have the Shakes; please bear with me as you read the Top 3 Most Read on Bloomberg this morning:

- “CYPRIOT OUTRAGE COULD DERAIL EURO-AREA BAILOUT”

- “ASIA STOCKS DROP ON CYPRUS BANK LEVY”

- “GOLD, GERMAN BONDS RALLY ON CYPRUS”

I know, I know – this is some scary stuff. If you’d like to freak-out alongside Old Media (must have crisis for ratings to stop crashing), I have a new hash-tag for you: #EOW (End Of World).

All of this comes after the US Dollar had its 1st down week in the last 6 (one week does not a new intermediate-term TREND make) – so what is a man or woman to do this morning but look at everything else that’s born out of the horror that is Cyprus:

- German and British stocks (after hitting new highs last wk) are down a whole -1% and -0.7%, respectively

- The Euro is actually now up on the session (versus the USD) at $1.29

- Irish stocks are up on the day too

Irish stocks? Yes me friends – ‘twas Saint Patty’s day yesterday. So, if the world is going to end today, have another pint, and smile about it will ya!

To be sure, at some point we will actually see the end of the world (and that day I will not be writing an Early Look), so I don’t want to be too complacent here. But I don’t want you freaking-out at another lower-high for the VIX and higher-low in the US stock market either.

Contextualizing where people are freaking-out from is usually more important than the why (their storytelling) after the correction (it’s called mean reversion, and yes it happens after stocks are up for 10 of the last 11 weeks).

First, here’s the context of Cyprus’ stock market:

- Down -8% in the last month

- Down -16% in the last 3 months

- Down -62% in the last year

Evidently, aside from some Russian money launderers (who don’t do Macro) getting smoked this morning, someone down there in the Socialized South of Europe knew something was going on, for a while now.

Then, there’s the US stock market’s context:

- Immediate-term TRADE overbought line = 1567

- Immediate-term TRADE support line = 1535

- Intermediate-term TREND support = 1486

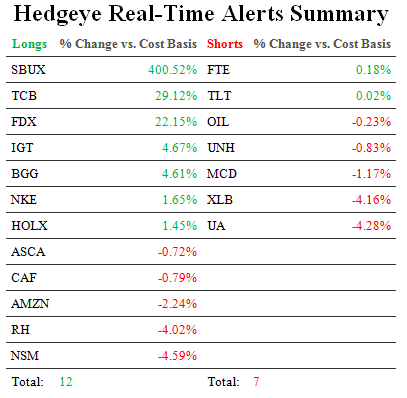

In other words, with US Equity Volatility (VIX) down another -10.2% last week to a fresh 5-yr weekly closing low of 11.30, the Fear-Dwelling (front-month VIX) is down -41% from the last day you could have freaked right out and sold low (February 25th, Italian Election Day). So you might not want to do that again today. After selling some on green last week, we’ll be covering shorts and getting longer again, on red.

Our immediate-term Risk Ranges for Gold, Oil, US Dollar, USD/YEN, UST 10yr Yield, VIX, Russell2000 and the SP500 are now $1, $107.27-110.17, $81.94-83.04, 93.64-97.39, 1.91-2.01%, 10.72-14.47, 938-958, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer