Commentary was better than the awful press release but concerns (e.g. Europe, dry dock costs) remain at the forefront

"Booking volumes during our seasonally strong wave period have remained solid with pricing comparisons improving in recent weeks. However, economic uncertainty in Europe continues to hinder yield growth. "Despite considerable attention surrounding the Carnival Triumph, we had been encouraged to see booking volumes for Carnival Cruise Lines recover significantly in recent weeks. Attractive pricing promotions, combined with strong support from the travel agent community and consumers who recognize the company's well-established reputation and quality product offering, were driving the strong booking volumes. "Our long term business fundamentals remain strong as we broaden our customer base of new and repeat cruisers through attractive product offerings, high satisfaction levels and compelling value propositions. We expect to drive return on invested capital higher through a measured pace of capacity growth and a continued focus on fuel consumption savings. We continue to expect over $3 billion of cash from operations this year and remain committed to returning free cash flow to shareholders in 2013 and beyond."

-CCL CEO Micky Arison

CONF CALL

- Q1: +3.9% capacity (+3.1% NA, +5.1%EAA (+17% in AIDA brand)

- Q1: net ticket yields : -3.3% (-5.8% EAA, -1.5% NA (2/3 of capacity in Caribbean); net onboard yield +1.1% (increase in NA brand offset by EAA brand weakness)

- Q1 Fuel price were down 4% YoY--saved them 3 cents

- 2013 Wave bookings (JAN 6-MARCH 10): fleetwide pricing slightly ahead, bookings running ahead; NA bookings running higher with slightly higher pricing; EAA bookings substantially higher with slightly lower pricing

- Post Triumph, ex Carnival brand, NA booking were higher ; EAA bookings were higher

- Post Triumph, Carnival brand, bookings trended lower but expect bookings to improve and normalize over the next several weeks

- Carnival Dream may have some effect on bookings and have taken that into guidance

- Will not break out quarter by quarter but overall bookings are behind last year at slightly lower pricing. NA bookings behind at slightly higher pricing; EAA bookings behind on lower prices.

- Caribbean/Alaska pricing is higher on lower occupancies

- Europe pricing/occupancies is lower; however, seeing significant uptick in European brand bookings

- Reduced ticket price trends contributed $0.14 decline (1/2 NA, 1/2EAA); lower onboard yields 6 cents; 5 cents ship modification costs (aka dry docks)

- Carnival Triumph: issues will take time to review and resolve

Q&A

- Hopeful Legend will sail its normal itinerary

- Will be more promotions, factored into guidance

- Won't see a huge incremental in sales and marketing

- Maintenance capex more like $600MM+ recently--the forecast CCL gives is around 800+

- Spending more on per berth basis as ships get older

- CCL doesn't capitalize dry dock costs

- Dry dock days are between 12-13; scheduled routinely twice every five years or once every three years for each ship

- 2013: 425 dry dock days planned

- Since 1Q Onboard spend was only up 1%, CCL took down 2Q, 3Q, and 4Q a little bit from previous guidance. All major categories will still be up but not as much as previously

- 30 cent guidance range is attributed to economic uncertainty in Europe and all the recent ship events

- UK/Germany: while bookings curve is still closer in, bookings have improved. For summer/early Fall, price cuts were taken to maintain occupancy.

- Still struggling with Italian uncertainty but encouraged by Costa brand

- Spain continues to be a challenge but our presence is small; we expect better performance in 2013 vs 2012

- Overall, Southern Europe was tougher than they thought

- Moving up dry docks that would have occurred in 2015 to 2013

- The 'hiccups' seen in the past couple of weeks are not major issues

- Huge decline in bookings (Carnival brand) immediately following Triumph but did not last very long

- From a consumer standpoint, most look at each brand but don't really connect to the corporate level.

- Costa had added a 2nd ship in Asia--pricing is good.

- Princess ship in Japan in late April; a second Princess ship in 2014 in Japan

- Why were commission/transportation expenses lower? Air cost as a % of mix is lower--less guests buying from CCL overall does not affect that #

HIGHLIGHTS FROM RELEASE

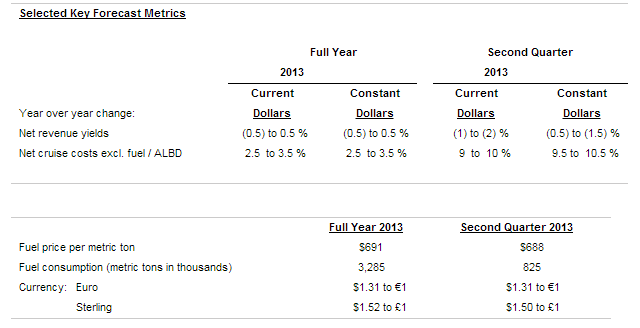

- The change in net yields is due to the economic uncertainty in Europe and pricing promotions for the Carnival brand combined with less than expected growth in onboard revenue across the group. The company also expects net revenue yields on a current dollar basis to be flat for the full year.

- The company expects net cruise costs excluding fuel per ALBD for 2013 to be up 2.5 to 3.5 percent on a constant dollar basis compared to up 1 to 2 percent in the December guidance. The change in cost guidance is due to the impact of repair costs, as previously announced, as well as, expenses related to the enhancement of vessels in the remainder of the fleet as a result of the ship incident.