This note was originally published at 8am on February 26, 2013 for Hedgeye subscribers.

“The tiger will see you a hundred times before you see him once.”

-John Vaillant

I’ve never been hunted down by a Siberian Tiger, but I’ll take John Vaillant’s word for it on how that might feel. On page 51 of The Tiger, he partly explains how I felt in very short order yesterday. Risk happens fast. Feelings aren’t what you want to be managing in your portfolio.

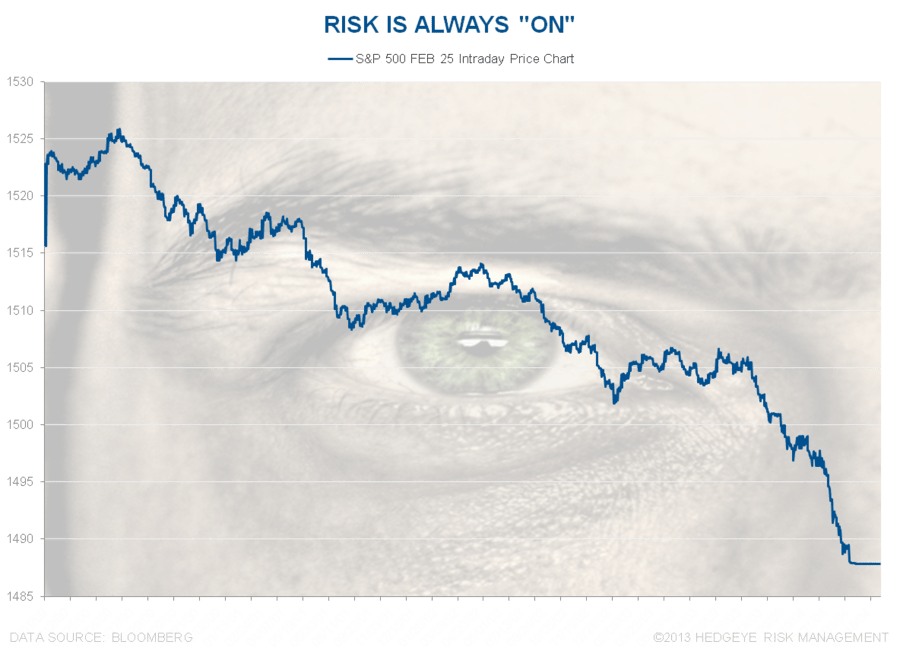

How could you not feel this? At 10AM EST yesterday, the SP500 was at 1524, and the Volatility Index (VIX) was at 13.63. I thought we were going to test the YTD high (1530 SPX) and volatility would continue to collapse. I thought wrong.

Actually, if you told me the reason why we were going to have a violent reversal (as in a +39% six-hour energy move in the VIX and the worst US stock market down day since November 7th) was the Italian election, I wouldn’t have changed my position either. I should have.

Back to the Global Macro Grind …

Should have, could have, would have – they are all loser excuses people make, so don’t expect me to make them this morning.

We made some good moves yesterday (covered our Yen short at the YTD low, shorted Utilities at the YTD high), but my overall net long position in US Equities was dead wrong. There is no excuse making in my books. The score doesn’t lie; people do.

Whether I think Italy should matter doesn’t matter. It’s what the market says matters that matters. So let’s get on with our day and focus on not making more mistakes.

As I wrote yesterday, I don’t start with the Research View (it actually improved again yesterday with Strong Dollar taking Oil prices down to a 7wk low), I start with the Risk Management Signals – here they are in the USA, across durations (TRADE, TREND, and TAIL):

- SP500 broke immediate-term TRADE support of 1502; remains bullish TREND and TAIL with 1463 TREND support

- Russell2000 broke immediate-term TRADE support of 901; remains bullish TREND and TAIL with 869 TREND support

- VIX ripped through all lines of resistance and moves to bullish TREND provided that 17.18 holds (watch this closely)

- US Dollar Index remains in a Bullish Formation (bullish TRADE, TREND, and TAIL)

- CRB Commodities Index remains in a Bearish Formation (bearish TRADE, TREND, and TAIL)

- US Treasury 10yr Yield broke immediate-term TRADE support of 1.96%; remains bullish TREND and TAIL with 1.84% TAIL support

Then, if I dig inside that 1st factor (SP500) and break it into Sector Style Exposures (dividing the pie into 9 S&P Sectors):

- 5 of 9 Sectors are still in Bullish Formations: Healthcare, Financials, Industrials, Utilities, and Consume Staples

- 2 of 9 are bearish on both TRADE and TREND durations: Basic Materials and Tech (AAPL = 14.9% of the Tech ETF)

- We bought Financials (XLF) into the close yesterday and shorted Utilities (XLU) on the open – both on signals

So, net net net – not a lot has changed here from a Research View perspective. The only S&P Sector that is down YTD is the one we’d expect to be down (Basic Materials), as we expect to see a Strong Dollar perpetuate A) commodity deflation and B) consumption #GrowthStabilizing.

However, that doesn’t mean the Risk Management Signals are going to let us out of The Tiger’s grasp right here and now. Immediate-term TRADE breakdowns force people to make decisions on intermediate-term TREND positioning. And that’s what we need to do next.

Looking at Global Macro risk more broadly, across Global Equity markets:

- Japan was down -2.26% last night (after being up +2.4% the day prior) and remains in a Bullish Formation (no TRADE breakdown)

- China’s Shanghai Composite was down -1.4% (broke TRADE support of 2321, but held TREND support of 2209)

- South Korea’s KOSPI was only down -0.47% overnight and is holding last week’s bullish TRADE/TREND breakout

- Brazil’s Bovespa remains bearish TRADE and TREND (that’s not new, and largely because of the Commodity exposure)

- Germany’s DAX broke TRADE support of 7670 again this morning; remains bullish TREND and TAIL with TREND support of 7528

- Italy’s MIB Index is a bloody mess, down -4.5% this morning and back into a Bearish Formation

So, do we give up on the Research View? Or do we acknowledge that short-term (TRADE) durations breakdown, breakout, and whip around - always stressing our ability to navigate the markets intermediate-term TRENDs?

Italy and France are dysfunctional economies being managed by a socialist #PoliticalClass (not new news – this is the 62nd Italian government since WWII). Brazil is going down for the reasons we think are bullish for the #1 research factor in our model (commodity deflation is a global tax cut for consumers).

Risk Sees my position. It sees yours too. It’s never “off.” It’s always on, and whether it was a SP500 price of 1524 (10AM EST) or 1487 (4PM EST), evidently it goes both ways, fast. I’ll be doing a lot of waiting and watching for the next few days, to make sure yesterday’s 6hr move wasn’t an emotional head-fake.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST10yr Yield, and the SP500 are now $1549-1612, $112.61-116.38, $80.72-81.98, 91.65-94.41, 1.84-1.96%, and 1479-1502, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer