The Q&A from today’s ECB press conference revealed that there was “discussion on whether to cut rates but the prevailing consensus was to keep rates unchanged”, leaving the interest rate on the main refinancing operations unchanged at 0.75% along with the interest rates on the marginal lending facility and the deposit facility at 1.50% and 0.00%, respectively.

The real call-out of the meeting is the ECB staff’s projections downward target range revision for Eurozone 2013 GDP to between -0.9% to -0.1% versus December’s estimate of-0.9% to 0.3%. Draghi blamed the revision on the worse-than-expected Q4 print of -0.6% Q/Q due to weak domestic demand and falling exports. The staff’s 2014 GDP estimate is a very “healthy” range of 0.0% to 2.0%.

The 2013 CPI range was revised to 1.2 – 2% hinting at a more deflationary outlook versus a December estimate of 1.3% – 2.5%.

In his prepared statements, Draghi highlighted recent data that suggests stabilization in 1H 2013 and improvement in 2H 2013. In the Q&A he suggested some positive signs leading to less “fragmentation”:

- Stronger world demand from exports

- The ECB’s monetary policy stance will remain accommodative as long as needed

- Counterparties have so far repaid €224.8 billion of the net LTROs issued (€500B)

- Target 2 balances are improving

- Funding for sovereigns has improved

- Increased capital flows from the core to the non-core

- Financial market improvement since July 2012

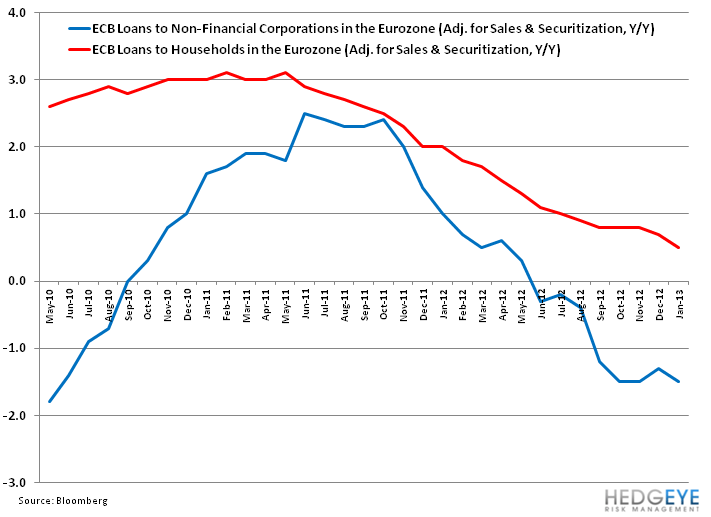

However when questioned on the difficulty of credit reaching the real economy, especially for small and medium sized enterprises, Draghi had little to say and no specific program in mind to spur lending. Below we show a chart of the weaken credit lines to households and corporations, one piece of evidence of a very clogged environment that should hamper real growth.

--Today’s Q&A was packed with questions on the Italian election and how those receiving the most support rejected the fiscal discipline that Draghi advocates. Draghi had this to say: “markets, despite excitement after the election, have reverted back to where they were before. There’s recognition that these are democratic elections. Much of fiscal adjustment that Italy already went through will now go on auto pilot, and the country has less debt versus 2012 to roll over. You’ve also seen that contagion to other countries is muted, versus the past. This is positive.”

--The question of staggeringly high youth unemployment came up again which Draghi dodged, saying it’s up to the individual countries to provide labor market reforms.

--On the need for a bailout of Cyprus Draghi said that the Eurogroup is discussing this and a statement could perhaps come in the second part of March. He said Cyprus is a small country but transfer risks could be bigger and it’s important for the Cyprus government to take this opportunity to adhere to anti- money laundering legislation.

--On the rumor of the ECB leaving Troika, Draghi called the report “Angst of the week”, and said it was unfounded.

As it relates to the EUR/USD, we don’t think the outcome of today’s meeting will have a huge impact on the currency cross. The meeting does suggest bearishness due to a lower 2013 GDP target and more downside to the CPI outlook. However, Draghi still appears armed to issue policy and leverage the bank where necessary, which should continue to support the cross. We think the real inflections over the next days and weeks will come from the uncertainty over Italy’s next government.

Matthew Hedrick

Senior Analyst