TODAY’S S&P 500 SET-UP – March 4, 2013

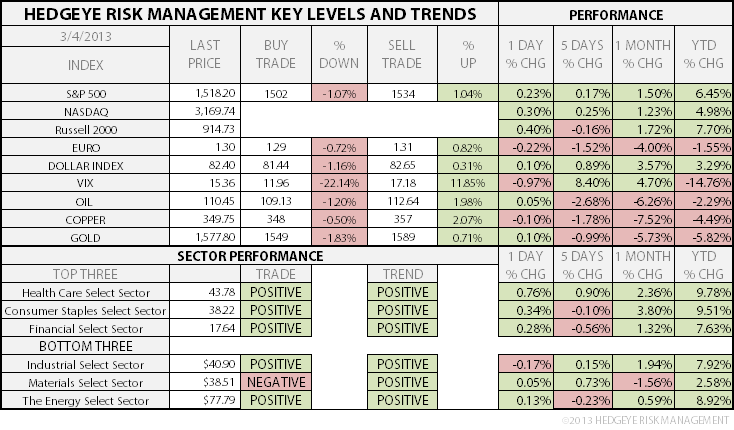

As we look at today's setup for the S&P 500, the range is 32 points or 1.07% downside to 1502 and 1.04% upside to 1534.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.62 from 1.61

- VIX closed at 15.36 1 day percent change of -0.97%

MACRO DATA POINTS (Bloomberg Estimates):

- 8am: Fed’s Yellen speaks in Washington

- 9:45am: ISM New York, Feb. (prior 56.7)

- 11am: Fed to buy $1.25b-$1.75b notes in 2036-2043 sector

- 11:30am: U.S. to sell $35b 3-mo. bills, $30b 6-mo. bills

- 11:45am: Former Fed Chairman Volcker speaks in Washington

- 1:15pm: Fed’s Powell speaks in Washington

- U.S. Rates Weekly Agenda

GOVERNMENT:

- This week, agencies implement automatic budget cuts, House may take up continuing resolution to keep govt funded

- IAEA board convenes in Vienna to discuss Iran

- Institute of International Bankers conference; speakers include Under Sec. of Treasury Mary J. Miller, Fed Gov. Jerome Powell, Comptroller of the Currency Thomas Curry, CFTC Chairman Gary Gensler, FDIC Chairman Martin Gruenberg

- Washington Week Ahead

WHAT TO WATCH

- Obama calls lawmakers to seek ways to recast budget cuts

- Euro leaders demand austerity; Italy moves closer to vote

- Las Vegas Sands says it probably violated FCPA

- Buffett plans acceleration of Berkshire capital spending

- Buffett plans to boost stake in IBM; says yr was subpar

- Transocean board seeks $2.24/shr div; Icahn wanted >$4

- Kuroda pledges bolder action as BoJ governor

- Samsung to seek further review as Apple damages cut ~45%

- Genting to buy unfinished Las Vegas Echelon resort from Boyd

- China monetary tightening pressure eases as rebound slows

- ‘Giant Slayer’ is wknd’s top film w/ $28m in NA sales

- U.S. Weekly Agendas: Finance, Industrials, Energy, Health, Consumer, Tech, Media/Ent, Real Estate, Transports

- North American M&A Agenda

- Canada Weekly Agendas: Energy, Mining

- U.S. Jobs, ECB Rate Meeting, Kenya Votes: Wk Ahead March 4-9

EARNINGS:

- Yingli Green Energy (YGE) Pre-mkt, $(0.57)

- Tech Data (TECD) 6am, $1.76

- Arena Pharmaceuticals (ARNA) 7am, $(0.05)

- Stratasys Ltd (SSYS) 7am, $0.38

- Vermilion Energy (VET CN) 7am, C$0.53

- Shuffle Entertainment (SHFL) 4pm, $0.12

- Cninsure (CISG) 4pm, NA

- Ascena Retail Group (ASNA) 4:02pm, $0.23

- Santarus (SNTS) 4:05pm, $0.01

- ABM Industries (ABM) 5pm, $0.22

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Oil Futures Decline for Third Day to Trade Near $90 a Barrel

- Investors Least Bullish in Four Years Pulling Funds: Commodities

- Gold Swings as Investors Weigh Economic Stimulus Against Dollar

- Cocoa Falls to 10-Month Low on Ivory Coast Rainfall; Sugar Rises

- Palm Oil Climbs as Worst Losing Streak Since 2006 Spurs Demand

- Indonesian Palm Reserves Seen Declining by Bangun on Demand

- Lead and Zinc Decline as China Property Curbs Could Damp Demand

- Vietnam 2013 Rice Exports Reach 744,408 Tons as of Feb. 28: VFA

- Angola to Start Cargo Rail Line From Luanda Port This Month

- Keystone Report Spurs Opponents to Vow Stiffer Fight on Pipeline

- Marathon Said to Join Oil CEO Search as Bid War Looms: Energy

- U.S. Soybean Reserve Seen Lower in Survey; Grain Supply May Rise

- Joblessness Down as Bernanke View of Cyclical U.S. Weakness Wins

- Rubber Drops to Two-Month Low as China to Cool Property Prices

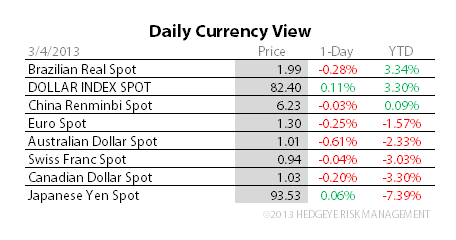

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team