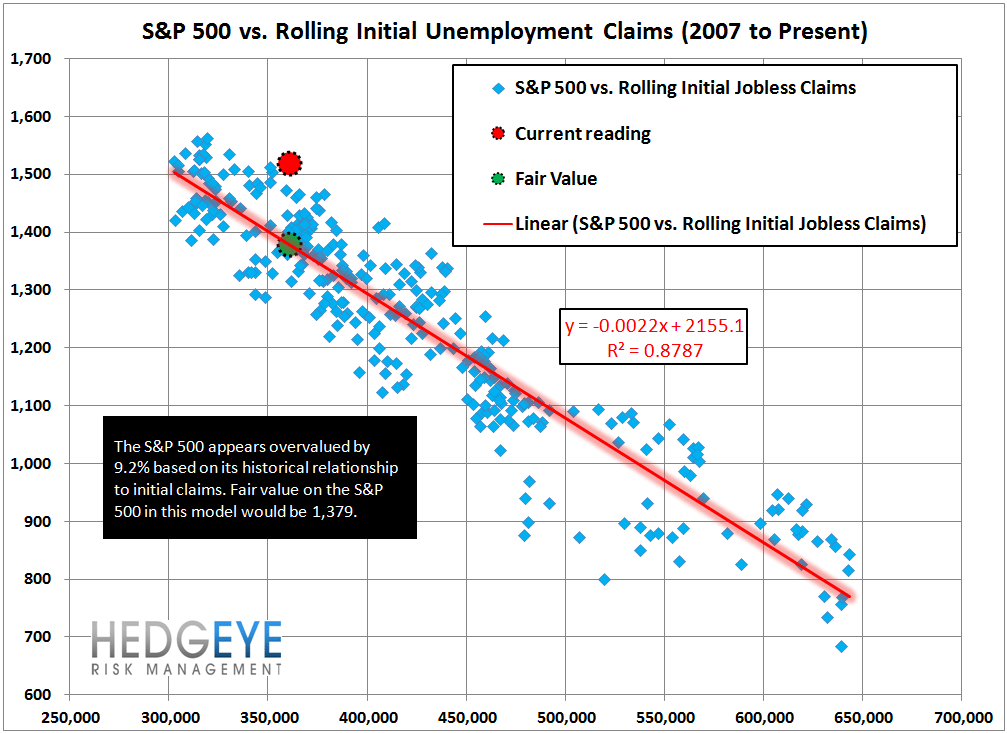

Labor Market Improves Further In Latest Week

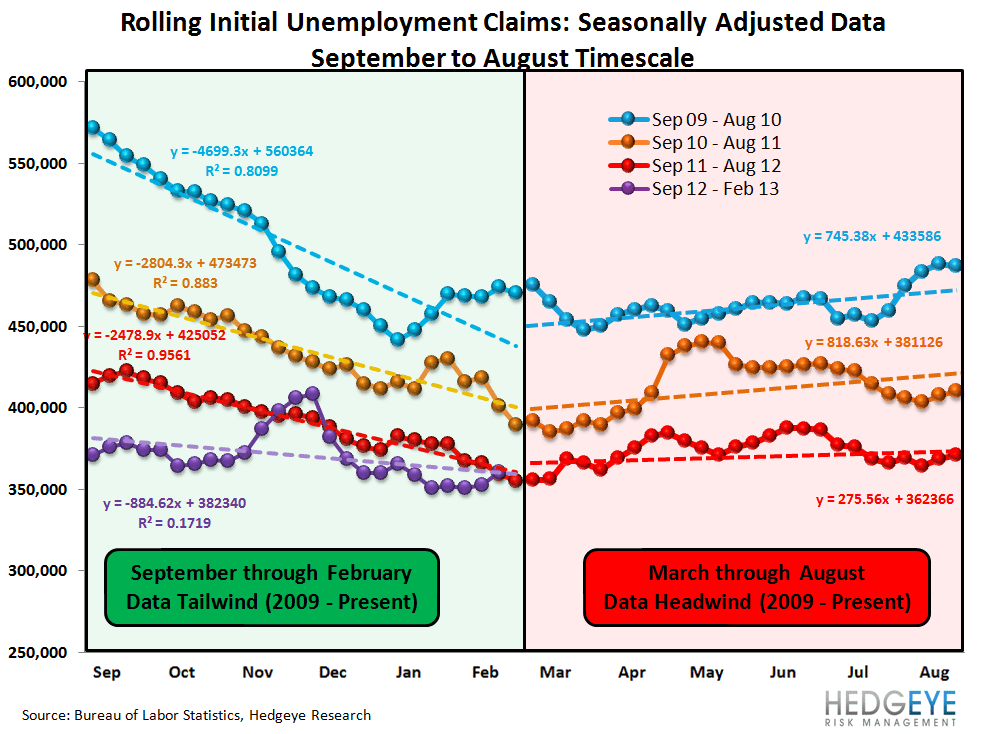

This week's backup in initial claims (SA) was a bit of a negative surprise, as the last four years have shown steady improvement throughout February. As a reminder, the seasonally-adjusted tailwinds will be coming to an end in a few weeks.

Prior to revision, initial jobless claims rose 21k to 362k from 341k WoW, as the prior week's number was revised up by 1k to 342k.

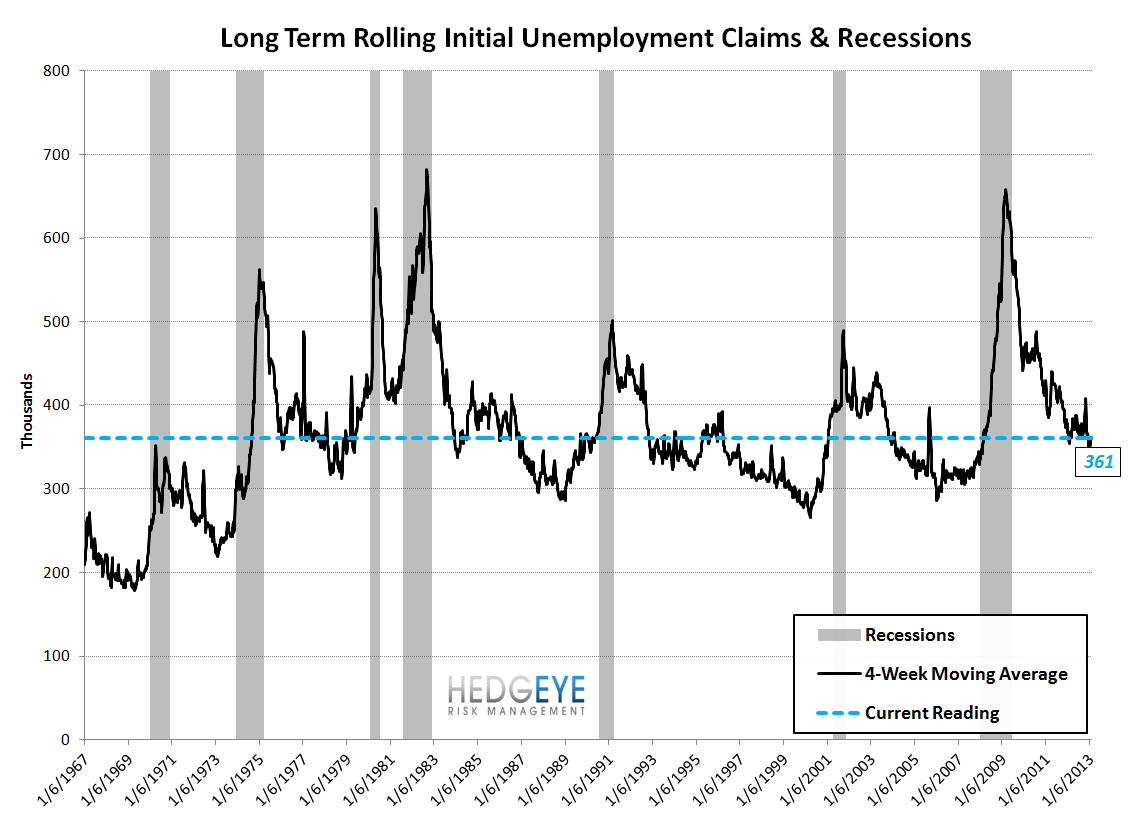

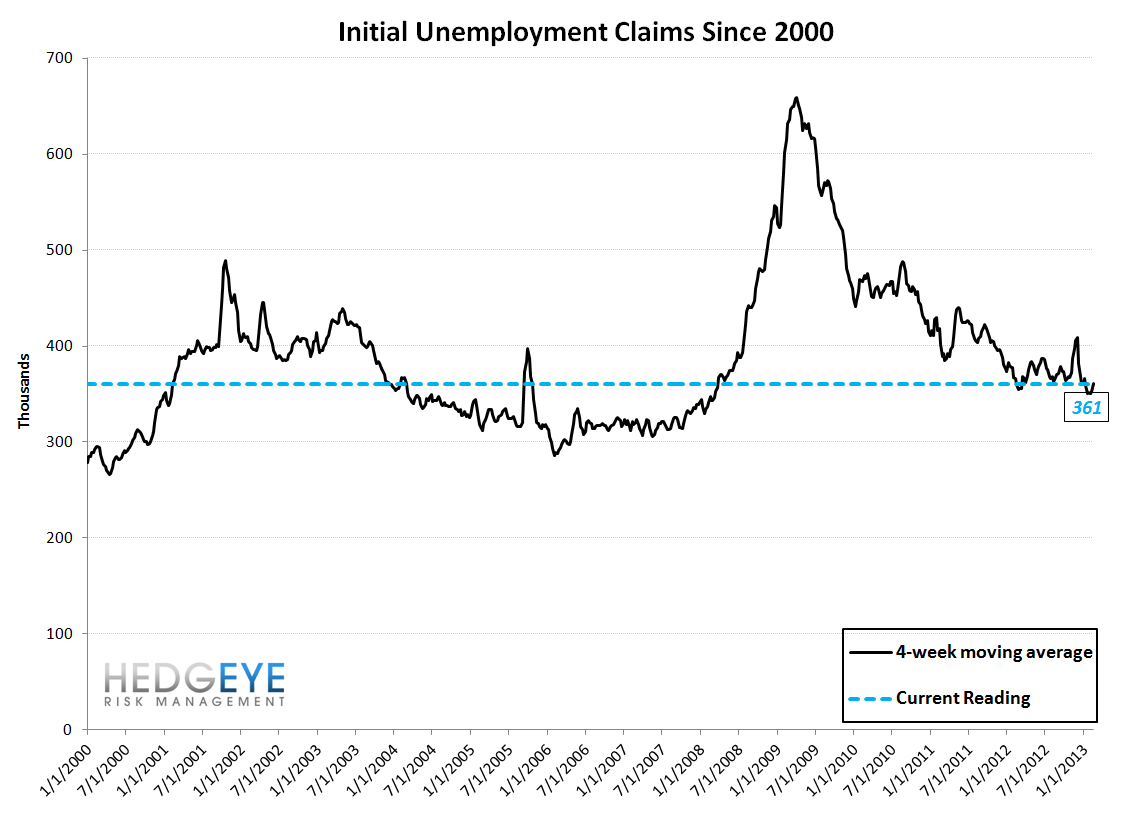

The headline (unrevised) number shows claims were higher by 20k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 8k WoW to 360.75k.

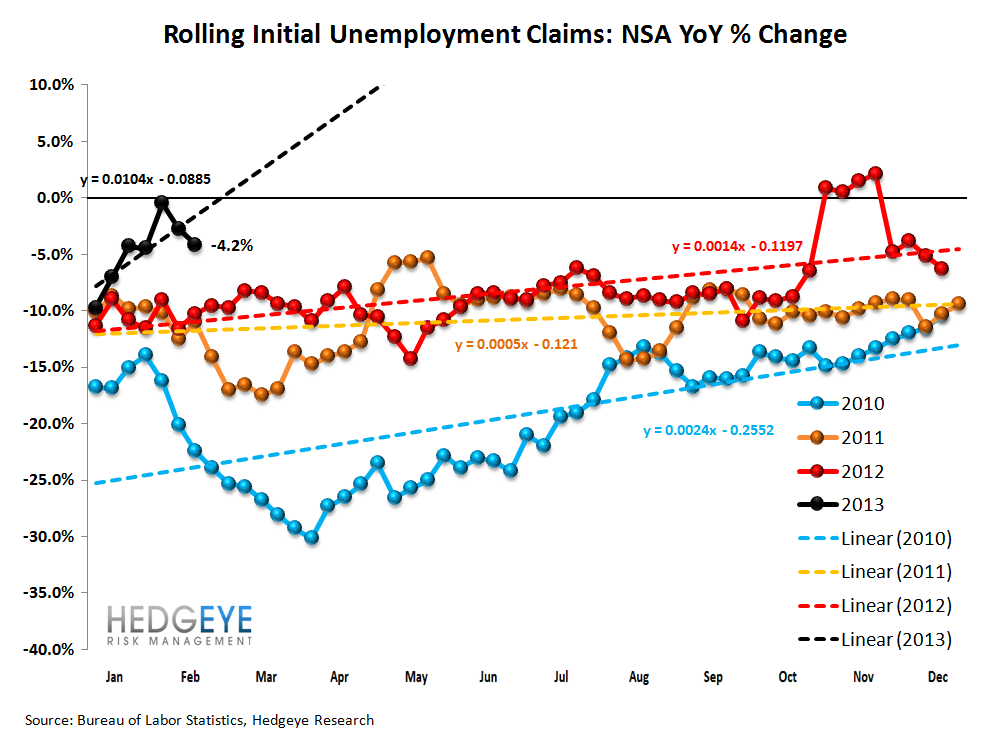

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -4.2% lower YoY, which is a sequential improvement versus the previous week's YoY change of -2.7%. This is good news, as it signals that the real labor market is, in fact, still strengthening.

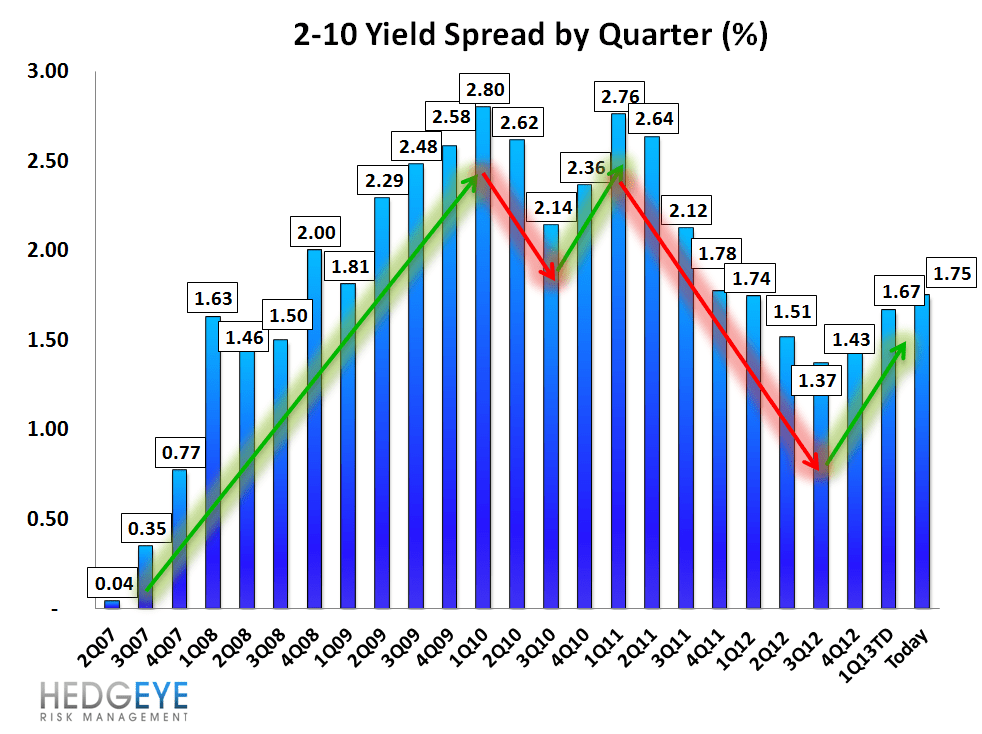

Yield Spreads Widen Further

The 2-10 spread rose 3.8 basis points WoW to 175 bps. 1Q13TD, the 2-10 spread is averaging 167 bps, which is higher by 24 bps relative to 4Q12.

Joshua Steiner, CFA