This note was originally published at 8am on January 25, 2013 for Hedgeye subscribers.

"Most of the time ‘I don’t know’ is the right answer.”

-Wesleyan University Professor, 2008

It was nearing midnight and towards the end of a ten hour stint in a 4’ x 8’ freezer on a winter night in early 2008 that I realized I wasn’t going to be a career research doctor.

At the time, I was a PhD candidate performing an RNA isolation as part of some larger work on DNA enzyme kinetics. What that means exactly isn’t really important, but it takes a long time and the work flow requires that most of that time be spent inside a walk-in ice box.

Tired, bored, and numb, I was thinking more about the puts I bought in NLY (REIT/Mortgage Investor) earlier in the day than on the final mix components for the experiment. I ended up aliquoting (fancy science term for “added in”) way too much of the wrong substrate into the mix. No take-backs or mulligans in experimental biochemistry - Game over, reset clock, 10 more hours of overnight freezer duty. A short-time later I joined Hedgeye.

Similar to probing the populous on their view of functional Enzyme Kinetics, I imagine that asking the average person how the U.S. calculates inflation conjures images of Good Will Hunting scenes, blackboard equations and chalk dust mathematical revelation.

Reality, however, more often resembles a bearded, middle-aged Robin Williams than it does a svelte, young Matt Damon. Consider the following question:

“If someone were to rent your home today, how much do you think it would rent for monthly, unfurnished and without utilities?”

That gem of a perfectly subjective question, asked as part of BLS’s monthly price survey process, drives the calculation of “owner’s equivalent rent” and singularly represents approximately one quarter of the index used to calculate CPI inflation in the United States.

China reports official GDP numbers 5 minutes after the quarter ends, we have owner’s equivalent rent. Next.

Parsing the reality from the illusory in reported domestic labor market data and understanding the subtleties of the seasonal and other statistical adjustments presents its own unique challenges.

‘Tis the Season(ality)

As we’ve highlighted previously, strong and quantifiable seasonal adjustments have had a meaningful impact on the temporal trend in reported economic and employment data over the last four years. In short, the shock in the employment series in late 2008 – early 2009 which occurred alongside the peak acceleration in job loss during the Great Recession has been captured, not as a bona fide shock, but as a seasonal factor.

The net effect of this statistical distortion is that seasonal adjustments act as a tailwind from September – February, then reverse to a headwind over the March-August period. From a positive seasonal adjustment factor perspective, we’ve got about one month left.

Sell in May & Go Away (Until September)

From a strategy perspective, the temporal pattern in market dynamics, despite being rather obvious to any market observer, hasn’t been insignificant.

The annual déjà vu pattern in market prices, reported economic data and monetary policy announcements observable over the last 4 years isn’t particularly surprising when considering the reflexive interaction between the associated dynamics:

reported economic data begins to inflect, market prices move higher, confidence and optimism measures begin to improve alongside stock prices and reported econ growth, the marginal bid moves from treasuries to equities as improving conditions pull expectations around a Fed exit timeline forward, equities benefit further while the reported data continues to confirm - until it doesn’t - and then the dynamics reverse, culminating with a new QE announcement in late Q3 just as the data and seasonal adjustments impacts hit trough.

Compressed economic cycles and amplified market volatility at its statistically distorted and centrally planned best.

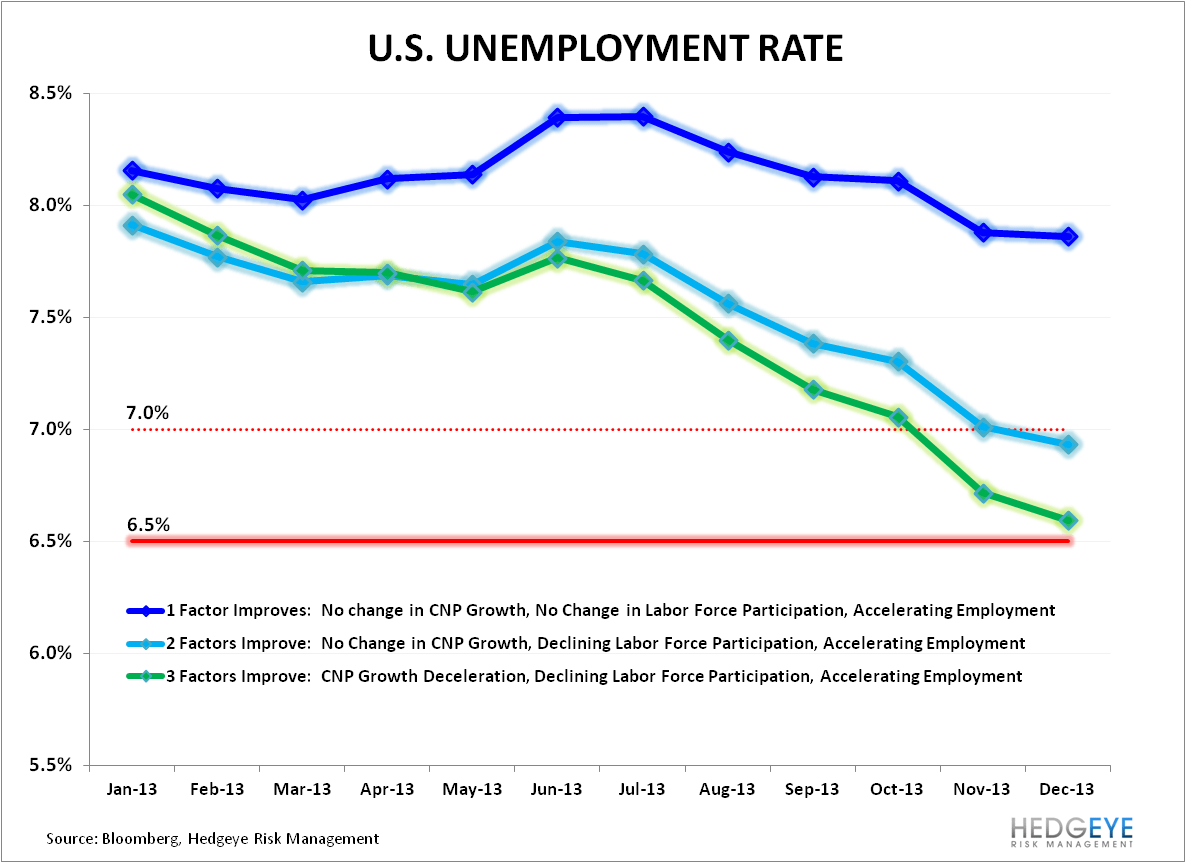

6-Handle?

As the domestic employment and housing data has continued to confirm our 1Q13 Macro Theme of #growthstabilizing, a risk management question we’ve been considering is the possibility of seeing a 6-handle in the unemployment rate in 2013. With Bernanke offering an explicit employment target of 6.5% for a cessation in QE initiatives, a significant decline in unemployment over the NTM may augur higher yields as the bond market attempts to front-run a prospective Fed exit.

A material, mean-reversion back-up in yields is of obvious import for asset allocation decisions and remains the principal candidate catalyst for a driving a large-scale rotation to equities.

Further, in so much as an end to money printing is dollar bullish, we could see a perpetuation of the USD Higher --> Energy/Commodities lower --> Real Earnings/Real Growth Higher dynamic we think needs to persist for sustainable real consumption growth. A step function move lower in commodity prices would also be equity supportive from a rotation perspective.

In a recent analysis we framed up the variable dynamics and put some quant around the magnitude of change in the relevant unemployment rate drivers necessary to take unemployment below 7.0% over the NTM (email us if you’d like a copy of the note).

In short, while we wouldn’t necessarily view a 6-handle on the unemployment rate by 2013 year-end as our baseline case, the reality of the math suggests that it wouldn’t take extraordinary improvement in the factors that drive the unemployment rate to take it below 7% over the NTM.

In terms of how we model unemployment, we effectively need to see 2 of the 3 input variables to trend favorably with respect to their impact on the unemployment rate.

For example, scenarios in which Employment Growth accelerates a reasonable 20bps (2Y basis) on average in 2013 and growth in the Civilian Non-institutional Population (CNP) declines linearly to the historical average over the NTM or the Labor Force Participation Rate (LFPR) continues to decline at the 3Y CAGR both result in a move to/below the 7% unemployment level in 4Q13.

In the chart below we provide a timeline view of the 2013 Unemployment Rate under a selection of progressively favorable scenarios. If you’d like to observe the impact of your own growth and participation rate assumptions on the unemployment rate timeline you can link to the associated model here >> Unemployment Rate Variable Analysis_HEDGEYE

Yesterday on CNBC Ray Dalio remarked that the question for investors now, as always, is how events will transpire relative to what the market has discounted.

We continue to like our 1Q13 Macro themes of #growthstabilizing and #housingshammer. Ultimately, however, Investment perspective remains wedded to last price. Now a hundred SPX points higher from where we first penned the #growstabilizing hashtag back in early December, the relevant risk management question is whether growth can organically and sustainably accelerate from here.

On my first day in the freezer in grad school, my professor offered the following piece of memorable advice with respect to evaluating one’s place within the program’s intellectual pecking order:

“Regardless of what they say, nobody really knows anything. Most of the time ‘I don’t know’ is the right answer”

Stay Tuned.

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now, $1654-1679, $111.51-113.95, $3.65-3.71, $79.41-80.14, 1.32-1.34, 1.84-1.91%, and 1481-1502, respectively.

Christian B. Drake

Senior Analyst