“Should I be turned into a vegetable or a happy imbecile?”

-Nassim Taleb

That’s a quote from Chapter 3 of Taleb’s book, Antifragility, where he discusses everything from “Crimes Against Children” to the misguided interpretation of “equilibrium” by social scientists.

Clearly, Taleb doesn’t like social scientists. There’s a little bit more than a little anger in some of what he writes, but there’s also plenty of truth. Sometimes the truth makes some people angry.

Personally, I like socially oriented scientists. I just don’t want them running my money. For that, I don’t need a philosopher either. I need a real-time Risk Manager.

Back to the Global Macro Grind…

The thing that non-market people generally don’t get about risk is that it works both ways. There is no such thing as risk “on” and “off” inasmuch as there is no Mr. Miyagi running the Bank of Japan (yet) either.

Risk is always on. It can squeeze you to the upside as fast as it can crash on you to the downside. There is no better example than that in the Land of The Rising Sun itself. Since Bernanke’s Top (September 2012) where he completed his US Dollar Debauchery, the Japanese Yen is down approximately -17%. Since US stocks stopped going down on #GrowthSlowing (mid November), the Nikkei is up +32.4%!

The Nikkei (for all the social scientists out there still trying to prove out their Ph.D in Keynesian Economics) isn’t something you can export. During today’s Currency War, it’s what squeezes (and pleases) politicians in the short-term (the stock market), while it impales their people’s purchasing power for the long-term.

Enough about that.

Why do I keep buying the damn dip?

- Fundamental Research: Macro Economic Data in Asia and in the USA continue to improve

- Quantitative Signals: my model continues to signal higher-lows of support and higher-highs of resistance

Why make it any more complicated than that?

I used to.

Then I started reading a lot of books and realized how much I do not know.

That’s why the best fundamental framework I can find right now is grounded in Chaos Theory. No, that doesn’t mean I am a philosopher. Neither does it mean I’m turning into a happy bullish imbecile. It simply means I fully Embrace Uncertainty.

What does the mean?

- I obey the signal, not the noise (Quantitative Signals)

- I then attempt to confirm or disprove the signal alongside my team (Fundamental Research)

I know, I keep saying the same thing, over and over and over again. I guess that might make me somewhat antifragile, for now. Then I’ll get clocked, and I will feel shame – then it will be time to evolve my process all over again.

As US and Asian Equity markets (our 2 largest allocations in the Hedgeye Asset Allocation Model) move back to immediate-term TRADE overbought, here are some mixed signals to consider amidst your daily noise from the #OldWall:

- SP500 immediate-term Risk Range remains tight and trade-able (for now) = 1

- US Equity Volatility remains bearish and breaking down relative to 5yr lows; TRADE support = 12.15

- US Equity Market Volumes are now trending bullish on up days and bullish (down volume) on down days

- US Dollar Index continues to make higher long-term lows, holding its TAIL of $78.11 support

- Chinese Equities (Shanghai Composite) are crashing to the upside into a Bullish Formation (2274 TAIL support)

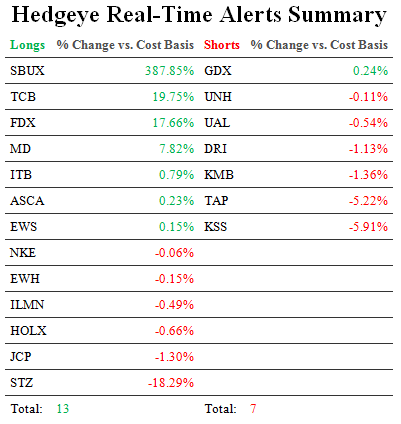

- Both our Hong Kong (EWH) and Singapore (EWS) long ETF positions aren’t as overbought as the SPY at 1516

- Japan’s Nikkei flashed an immediate-term TRADE overbought signal overnight at the Yen signaled oversold

- KOSPI continued to diverge, like Brazil’s Bovespa has, breaking its TRADE and TREND lines of support

- EuroStoxx600 was down -0.5% last wk and is confirming an immediate-term TRADE breakdown again today

- France, Italy, and Spain have all seen their respective stock markets snap TRADE lines of support

- CRB Commodities Index failed, again, at its long-term TAIL risk line of 306 so far this week

- Gold continues to look like Treasury Bonds, awful relative to US and Asian stocks

- Oil remains the biggest NEW headwind to our Fundamental Research call on global #GrowthStabilizing

- US Treasury Yields (10yr) are now confirming a Bullish Formation (bullish TRADE, TREND, and TAIL)

- Yield Spread (10s minus 2s) is plenty wide at +174bps this morning; bullish for the Financials (XLF)

There is no “equilibrium” in a multi-factor, multi-duration, Global Macro risk management model. There is no happy place either. Like in any dynamic, non-linear ecosystem, what you want to embrace is the uncertainty of time and space.

So eat your veggies, buy red, sell green, and keep moving out there as risk factors do.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, EUR/USD, USD/YEN, UST 10yr Yield, and the SP500 are now $1, $114.96-117.41, $79.11-79.94, $1.34-1.36, 91.63-94.33, 1.91-2.10%, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer