One derivative of the financial distress in the gaming industry may be the need for capable casino management. The ownership transfer to the banks and bondholders of distressed assets and companies, in most cases, necessitates a third party to actually run the casinos. Additionally, with all of the assets potentially up for sale, private equity appears to be circling the wagon and would certainly need capable casino management. We’ve argued that the survivors will benefit from potentially fewer competitors and certainly lower quality competition as capex budgets have been slashed. The survivors could also capitalize on a re-emergence of the third party casino management contracts, something not seen on a mass scale since the explosion of Native American Casinos.

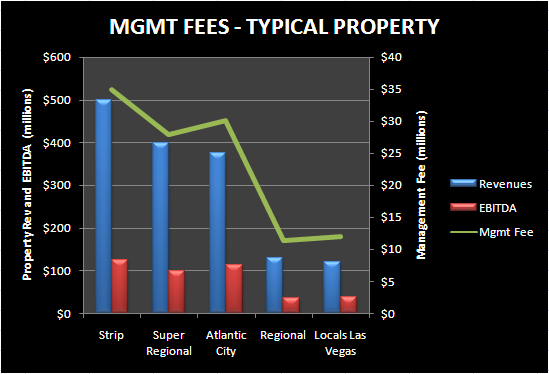

Third party casino management is a terrific business. It requires little upfront cash and is essentially pure profit, thus it is ROIC enhancing. The management company generates a fee usually based off revenues (stable) and operating profit (incentive based). In the charts below, we’ve highlighted some examples of potential contracts using a fee structure of 2% of revenues and 20-25% of EBITDA. Each example is based on an average type property in the market indicated. Obviously, the numbers could be much higher. For instance, Bellagio should generate around $1.1 billion and almost $300 million in revenues and EBITDA, which would produce a management fee of $80 million, under our assumptions.

Private Equity has likely been in touch with some operators already. The relationship with Private Equity would probably include an equity contribution by the manager to secure the contract. Given the numerous distressed gaming assets, lenders are probably reaching out to capable operators as well. The potential operators could include some of the better regional operators such as ASCA, BYD, PNK, and PENN. These companies generate between $200 (PNK) and $625 million (PENN) in EBITDA annually so clearly, management contracts would be material. Note also that the examples given are for individual properties. It is also possible that the operators could procure multiple management contracts, i.e. running the OpCo properties for Station Casinos.

The regional stocks have had huge runs off the bottom in the last few weeks. Valuations appear reasonable for these mature companies. However, a new growth vehicle such as casino management could justify higher valuations.