The EUR/USD has put on a nice move of +3.4% YTD and is up +10.3% since Draghi issued his all hands on deck to save the common currency (via the introduction of the OMT bond purchasing program) in early August 2012. This conviction in the EURO is expressed well by looking at CFTC contracts of net positions in the EUR/USD (1st chart below). Coming off a net short bottom last summer, contracts are decidedly now net long in the new year -- seemingly there has been a lot of firepower behind the possibility that Draghi could use the OMT!

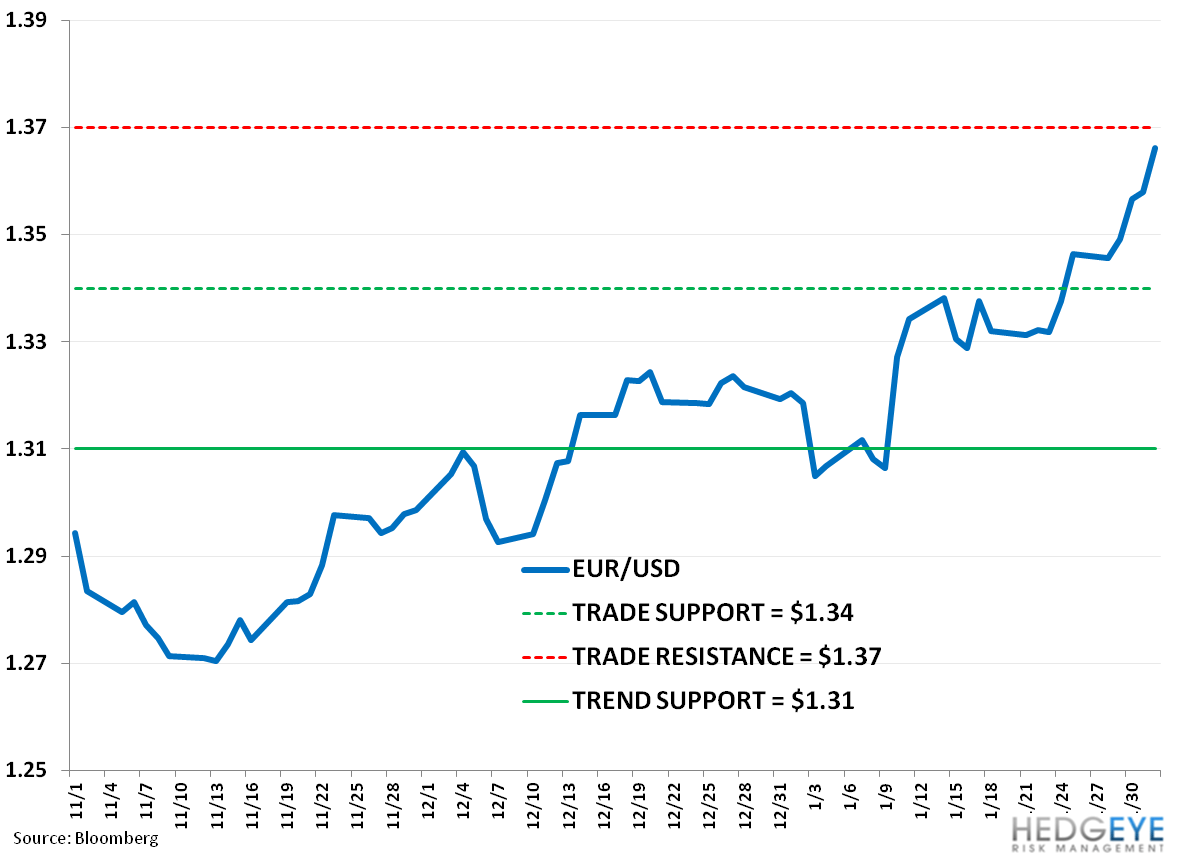

In the second chart below we update our quantitative risk levels for the EUR/USD, with topside immediate term TRADE resistance at $1.37 and intermediate term TREND support at $1.31. Our call remains to trade the range and it’s worth noting that there’s a pretty light formal calendar ahead.

What to watch for:

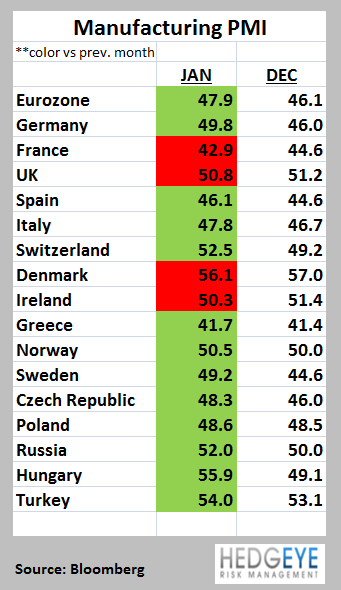

- ECB Meets: Thursday the ECB’s governing council convenes. We expect no change to the main interest rates. This position is grounded in recent data that is supportive of an “accommodative” hand’s off approach from Draghi – CPI came down 20bps to 2.0% Y/Y in JAN, exactly at the ECB’s targeted level; PMIs across the region looked broadly better, and importantly showed improvement in the Eurozone average and in Germany; and while the unemployment rate remains nominally high (10.7%), it saw no increase in the DEC reading. We think investors are beginning to price in much of the bad ‘crisis’ news, in that case what’s left in play is a long runway of slow, low growth, and unexpected sovereign/banking flair-ups across the periphery.

- Italian Election February 24-25: we expect to see much political uncertainty heading into the general election which may influence the EUR/USD. The largest and most recent scandal to shake political posturing ahead of the vote involves a 3.9B EUR government bailout to one of Italy’s oldest banks, Monte dei Paschi di Siena, due to derivatives deals gone wrong. The scandal has been a polarizing force because the commoner still feels badly hit by austerity measures while banks are seen as getting free handouts. As it turns out the bank is closely aligned and supported by the Democratic Party, and now you have the leading center left candidate, Pier Luigi Bersani, insisting that his party bears no responsibility, and blaming Mario Monti, the head of a centrist coalition of small parties, for the bank largess. Yet it’s likely the support of Monti’s side that Bersani needs to establish a coalition as his faction can’t win an outright majority. The result is that the scandal has helped boost former PM Berlusconi’s right-of-center Freedom Party, and therein fueled more uncertainty on how a coalition government will be formed.