Employment data released this morning by the Bureau of Labor Statistics is positive for the quick service restaurant industry. While near-term data out of the group may be underwhelming, from a comparable sales headline perspective, as we lap difficult weather compares, the pace of hiring in the QSR sector should not be ignored.

Per our note ahead of EPS next week, we like YUM, EAT (although Brinker already reported so not featured in note), and JACK (longer-term) and have a negative view on BWLD and CMG.

Leisure & Hospitality Still Rolling Over

Hiring within the leisure and hospitality sphere is sequentially decelerating, which likely a negative sign for restaurant industry sales, on aggregate. Full service employment growth tends to follow leisure and hospitality hiring more closely than quick service. The chart below illustrates trailing-twelve month growth in full service, quick service, and leisure and hospitality.

The chart below shows monthly employment growth and we can see that the divergence between employment growth in quick service and employment growth in full service is becoming more pronounced. While price points across the industry, among all subgroups, have been converging as the discounting war rages on in casual dining, an upgraded experience is helping QSR take share from casual dining, which is populated with often over-supplied and tired concepts.

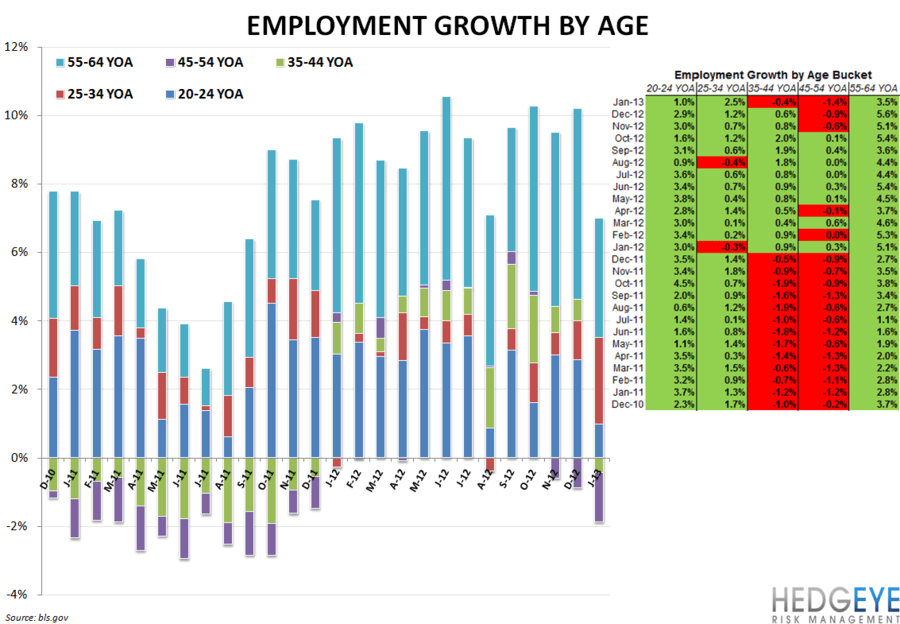

Employment by Age Data Mixed Start to Year

Employment growth by age cohort implies that quick service restaurants have been benefitting from strong employment growth among core consumers while casual dining’s difficulties have been exacerbated by some deceleration among some of the sector’s most vital consumer groups (by age).

However, the chart below highlights a mixed start to 2013 for employment growth among the younger age cohorts. Job growth in the 20-24 years of age cohort remained sequentially decelerated to +1%, year-over-year, versus 2.9% in December. The 25-34 years of age cohort saw employment grow by 2.5% in January, versus 1.2% the month prior.

The 35-44 and 45-54 years of age cohorts both saw negative year-over-year employment growth. We interpret this as negative for casual dining, a highly discretionary sector that derives much of its revenue from families and middle-aged consumers. As the chart below highlights, the 45-54 years of age cohort saw its third consecutive month of negative job growth. The 55-64 years of age cohort, also significant for casual dining, saw employment growth decelerate to 3.5% in January versus 5.6% in December.

Howard Penney

Managing Director

Rory Green

Senior Analyst