We like this company but are less sold on the stock.

Panera Bread’s shares have been among the worst-performing in quick service restaurants over the last 6 months. As the chart below illustrates PNRA shareholders have been suffering; until recently, PNRA was the only QSR stock with a negative return over the last half-year (YUM has also slipped into the red on a six-month basis). Considering this, alone, suggests that perhaps the stock is worth buying. We believe the fundamentals say “not yet”. Besides, depending on the duration one takes into account, any narrative can be told. Since early 2011, the stock is up roughly 60%.

Fundamental View

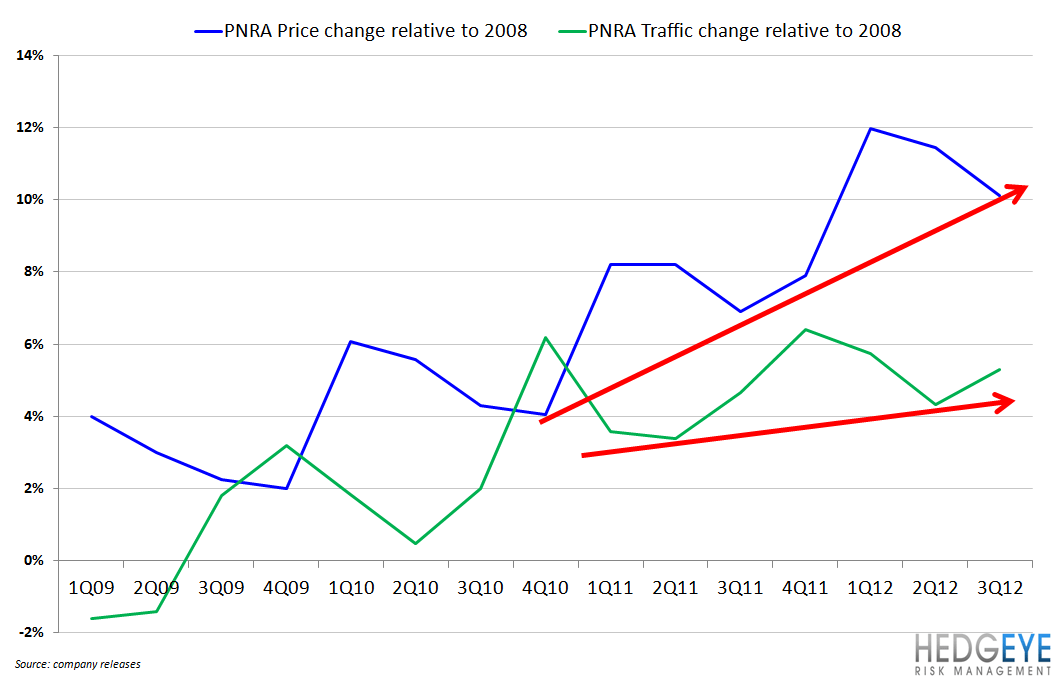

One of our chief concerns with Panera Bread is its ability to continue to generate positive traffic over the next three quarters. Over the past four years, comp growth has increasingly depended on pricing. 1Q13 is facing a difficult compare versus a year ago when weather boosted same-restaurant sales by 200 bps. We believe that 1H13 consensus expectations may be overly optimistic from a same-restaurant sales perspective. The company continues to build its marketing effort and we expect a similar increase in 2013 to that of 2012 to-date. The company’s catering business can potentially capture incremental traffic but we think there is a limit to how additive this initiative can be. The greatest source of leverage for the company is the marketing budget. By raising its marketing spend as a percentage of sales, PNRA can drive incremental traffic. With marketing at a mere 1.5% of sales, there is room to run before the company falls in line with industry norms. Guidance for 2013 is for that number to rise from 1.5% in 2012 to 1.7%.

With the average check at (roughly) $10 for lunch, Panera is now competing with the casual dining chains that are pushing lunch price points at $6-$7.

While there are plenty of positives to draw on, the fact that capex is growing so rapidly (with sequential acceleration), while sales growth seems to be rolling over, is a cause for concern. The company continues to generate strong Returns on Incremental Invested Capital but sequential deceleration has not historically been a good sign for stock price performance. If sales growth continues to diverge from capex growth, returns will continue to decelerate. We will be watching this name closely through 4Q12 EPS but, for now, ROIIC and our macro team’s quantitative model (below) indicate that it is premature to be long this stock.

Howard Penney

Managing Director

Rory Green

Senior Analyst