“If you’re going through hell, keep going” – Sir Winston Churchill

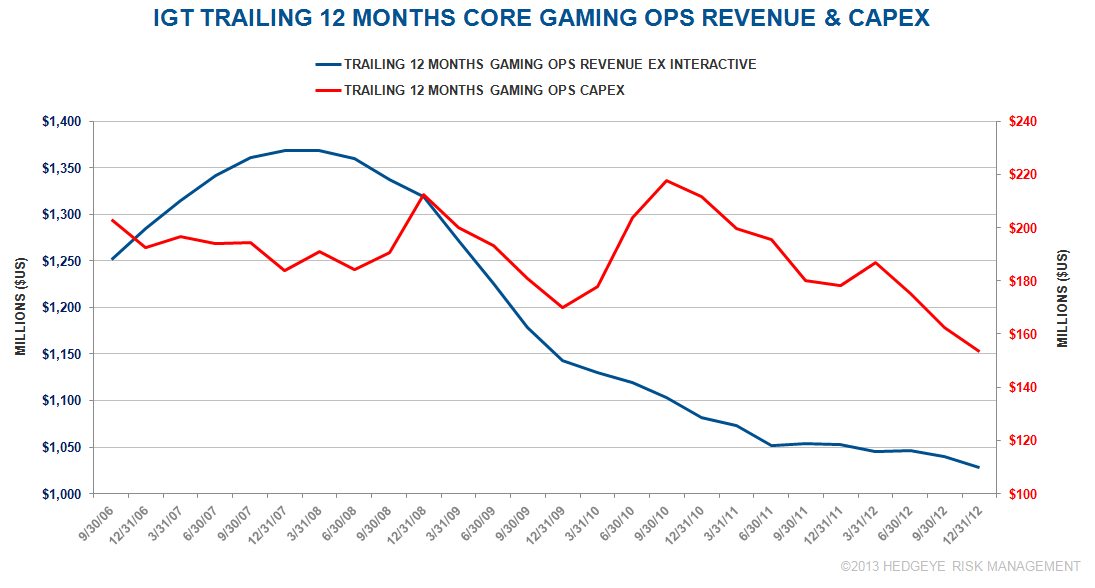

It’s been a long, downward spiral for IGT and its gaming ops business – a five year peak to trough slide of 24% in revenues. Ouch. While we’re not sure that that road has turned north, IGT does seem to be making the best of the situation. We could even go so far as to say that there is actually some definitive positives in the business. Market share in gaming ops has held steady for 2 years and the continued trend of right-sizing capital expenditures has contributed to growing operating cash flow in the segment.

IGT’s gaming operations revenues have declined in 17 of the last 19 quarters and in the 2 that were positive, the YoY increase was less than 1%. Gaming operations gross margin dollars have similarly seen declines in 15 of the last 20 quarters. Given this backdrop, we are encouraged to see IGT investing less money to produce these lackluster results. Gaming operations capital expenditures have seen 9 consecutive quarters of decline.

The bear may say that lower capex spending portends even worse results going forward. However, based on our rigorous statistical analysis, we have found a surprisingly small and statistically insignificant relationship between gaming operations spend and revenues. The fact is, IGT has been able to reduce the cost of maintaining its existing footprint. Maintenance declines are driven by:

- Game performance - The longer the games perform well, the lower the need is to refresh them

- Cost of a refresh

- It’s become a lot cheaper over the years to refresh titles (just a conversion kit and signage)

- The ability to efficiently refurbish and deploy older boxes

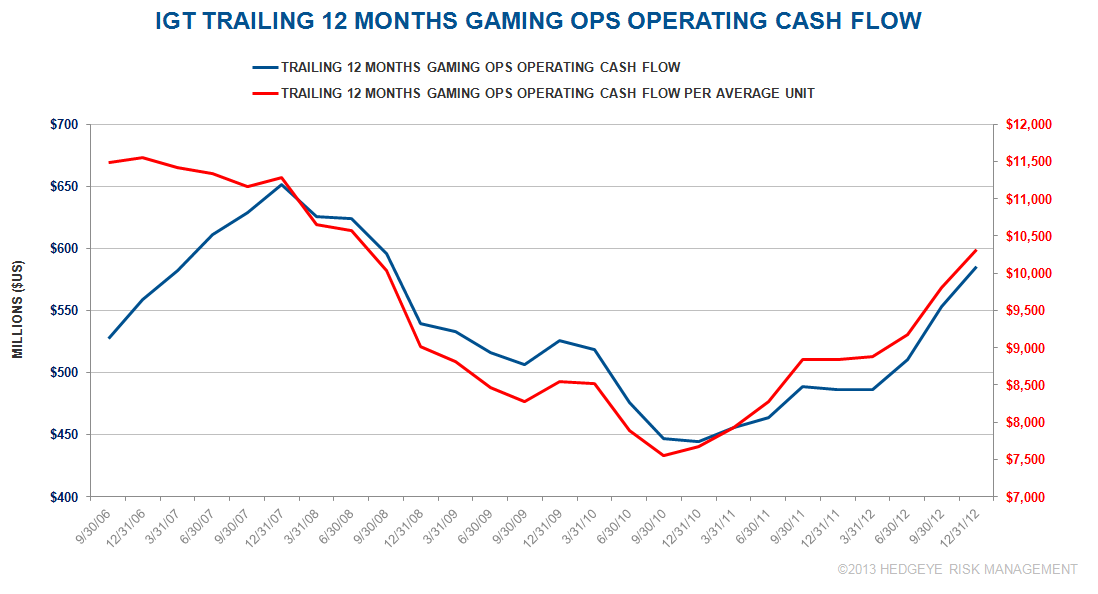

The chart below illustrates that as a result of right-sizing their capital expenditures, IGT has been able to grow their cash flow from gaming operations and increase the productivity of their install base despite the pressure on revenues.

IGT’s gaming ops performance has been a focus of investors, especially the bears. However, despite the strong headwinds, IGT has grown EPS YoY 6 out of the last 8 quarters, with 27% growth over the past 4 quarters. For fiscal 2013, we’re projecting 26% growth. The second leg of our positive thesis is IGT’s ability to generate strong cash flow and distribute that cash to shareholders. As evidenced by the chart above, IGT has been very successful turning a declining top line business into a growing cash flow generator. With the stock trading at just 11x, these factors should continue to move the stock higher as 2013 unfolds.