We think that this is the first ICR conference in at least 5-years where there is the absence of a major theme to carry the group – up or down – for the year. Management teams seemed complacent in their lot of ‘slightly better than average’ business trends, with few companies (FNP and URBN are two) who stand out with an exceptional process to drive their business to the next level.

Our top longs remain FNP, NKE, RH, URBN, and believe it or not – JCP is even gravitating to our bench of ideas.

On the short side, we like department stores – M, KSS, as well as GPS, and GES.

DETAILS

The tone of this week’s ICR conference seemed positive overall to us, with a far more favorable preannouncement cadence than last year, and notable commentary on good inventory positions despite mixed sales results. You could drive a truck through the range in quality of the management teams there, and we were specifically impressed with discussions with both FNP and URBN as it relates to their respective views as to what it will take to more than double the size of their businesses, and the categories and selling methods it will take to get there.

But there was one big trend that hit us hard – and that was the absence of a recognizable trend at all. That might seem like a ridiculous statement, but let’s look at past ICRs and add some context.

- 2008 and 2009: We were in the depths of the Great Recession. Positive datapoints were few and far between. The sentiment was almost uniformly negative, and the stocks behaved accordingly. Into the 2009 ICR conference alone, the group (as measured by the RTH – cap weighted S&P Retail Index) was off by almost 15%. The MVR (equal-weighted index of 30 retail stocks) was off by over 30% into and around the conference.

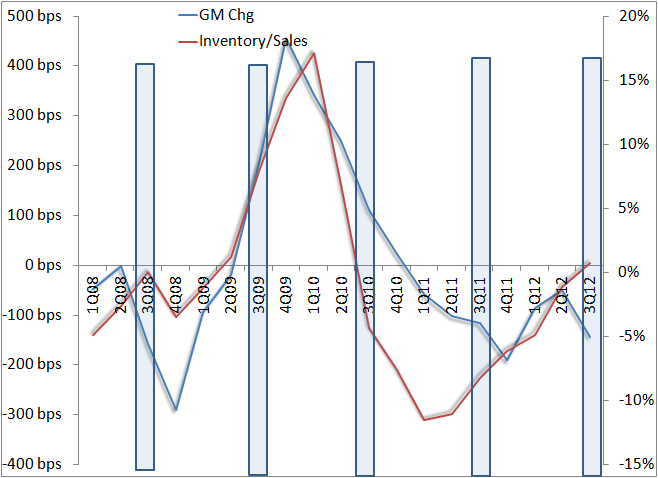

- 2010: This was a big recovery year. Sales accelerated and inventories fell. That sent gross margins up high and earnings revisions higher. This is clear as day in Exhibit 2 below. The stocks started to work in earnest two quarters before the conference, but were still up 5-10% on the event as the recovery continued.

- 2011: The Raw Material Scare. This is when people thought that cotton, which had just doubled in price over the shortest time period in history, would stay at $2 in perpetuity. The ‘recession earnings recovery’ slowed, at the same time the outlook for Average Unit Costs (AUC) went grossly out of favor. Translation = negative tone at ICR, and decelerating stock price performance.

- 2012: This was an interesting one. There were more severe preannouncements than any year yet, but more often than not companies chalked this up to the lingering impact of higher costs – which was the ultimate excuse because the fact of the matter is that it was valid. But at the same time the companies gave positive unofficial outlooks on getting pricing power in 2012 and the gap between AUR and AUC turning positive. The bottom line is that it gave people reason to believe, the tone of the event was upbeat, and the stocks traded up.

- 2013: This year, as shown in Exhibit 2, Inventory/Sales trends are back to zero-barrier after a strong four-quarter trajectory upward. Gross margins are still down, but are within 100bp of peak and unlike last year, clean inventories won’t likely provide a tailwind. We’re not looking to paint a big negative call here, but just can’t come up with something positive, either. We’re pretty much ‘retail-agnostic’. The market seems to agree, as the stocks are only up 3% on the event – which is less than usual. We may get more GM improvement in 2013, but by and large, we need a strong consumer for the group to work en masse from here. The lack of strong proactive plans by many companies seems to support this.

Exhibit 1: S&P Retail Index vs. Past ICR Conferences

Exhibit 2: Sales/Inventory Spread vs. Gross Margins (60 Company Average) vs. Past ICR Conferences