Shipbuilding Update: Walking Down a Long Plank

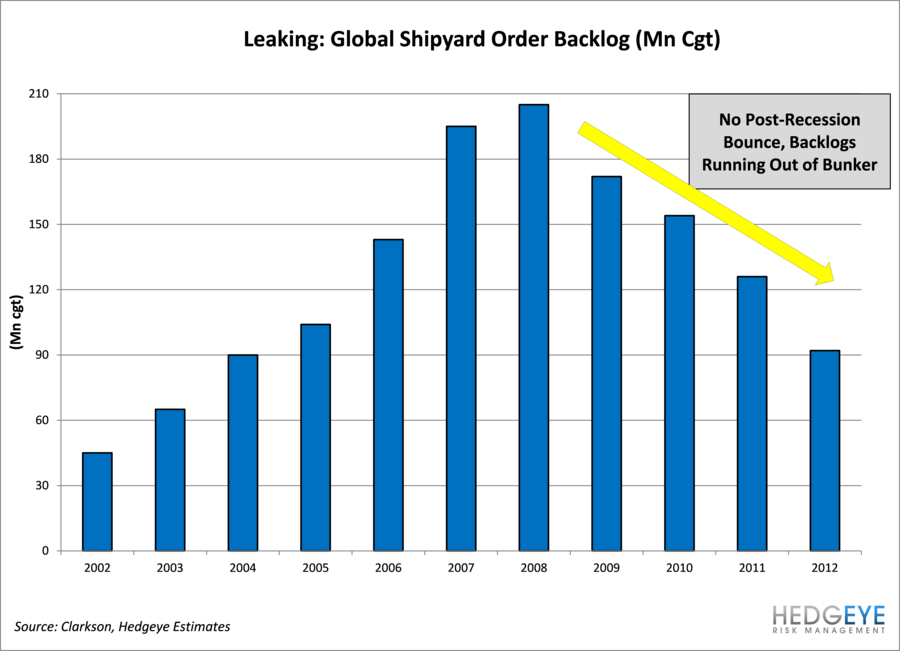

- Backlogs Sinking Fast: Consistent with long down-cycle in commercial shipbuilding, there has been no meaningful rebound in orders. That has left shipbuilders to drain backlogs, reporting revenues that relate to years-old demand. Backlogs have been on a steady downtrend, inflating revenues relative current demand. Chinese backlogs fell from 169.3 mil tons at the end of 2011 to 116.4 mil tons at the end of September.

- Short Fuse: Samsung Heavy has only about two years of work left in backlog, while Hyundai Heavy has only about 1.5 years. When backlogs with high margin orders are gone, revenues and profits should reflect the more averse current market. Using multiples of income statement items produced by draining backlogs is not a reasonable valuation approach, in our view.

- Pricing Highly Competitive: Global shipyards are desperate for new orders to keep their docks full (article). As backlogs continue to fall, pricing is likely to become irrational, in our view. Chinese competitors may be particularly aggressive. This will happen for a long time, if previous cycles are any guide.

- About Offshore: It has been our contention that Chinese shipyards will become increasingly proficient in offshore energy production vessels, undermining the bullish thesis on South Korean shipbuilders. Since this cycle will take upwards of a decade, the Chinese have plenty of time to enter every relevant offshore market, in our view. Chinese entry has continued to be aggressive, as discussed in the WSJ yesterday here.

- Performance & Opportunity: Since we first posted a note on the short opportunity in the Korean shipbuilders here, Samsung Heavy has only underperformed the KOSPI by ~ 8%. We think there is a good deal more that this short has to run as favorably priced orders in backlog are not replaced and margins contract toward historical (read: low) norms. We value Samsung Heavy at around krw 10000-14000 in our base-case DCF vs. a current market price of krw 37800 and we expect that gap to close over the next few years.

- Additional Information: We have additional background on the Shipbuilding industry, so feel free to follow-up if this industry is of interest.

Jay Van Sciver, CFA

Managing Director

HEDGEYE RISK MANAGEMENT

111 Whitney Avenue

New Haven, CT 06510