Guess? Is one of the more interesting names to us heading into ICR. It will undoubtedly be one of those companies where 50 analysts will be crowded around the CEO at the break-out session fighting to glean every last bit of information. But we have no reason to believe that the information will be positive relative to expectations.

To put this into perspective, the stock is up 14% since the trough before the latest quarter and is sitting just 4% (or $1) away from its TAIL line of resistance). On that last print, which was very sloppy to say the least, it was clear that management really has no clue as to why its business is weak. While placing blame on a weak consumer might be accurate, we can point to a host of other companies that are still growing even with a weak consumer.

Also, one notable difference at ICR this year is that GES is without a COO and a CFO – the first time in its history of attending this conference where that will be the case. So let me get this straight…the company just lost two of its best players (with the simultaneous and still mysterious resignation of Prince and Secor), and the remaining bench is left trying to bridge the gap between macro and a micro problems.

In looking at sentiment, one might think that these concerns are already baked into the stock. After all, sentiment (as measured by our Sentiment Monitor) is sitting near a historical low of 20 on a scale of 100. (i.e. this says that sentiment is bearish, which when exaggerated is a contrarian indicator for the stock).

But we don’t think so, and we think it comes down to earnings.

1) We need to assume that every business unit accelerates in order to hit the company’s 4Q guidance – which they issued at a time when they admittedly did not know what was driving their business down.

2) We’re at $1.65 next year versus the consensus at $2.32. Yes, it looks cheap at 10.8x consensus estimates. But it’s at 15.2x our number.

3) Keep the current multiple steady on our estimate, and you get a $17.75 stock – that’s 30% downside from where it is today.

Keep in mind that GES was one of the companies that came out an announced a special dividend for the 2012 calendar year -- $1.20 per share, or $110mm. This was one of the more self-serving moves we’ve seen, as the co-founders own 30% of the stock and drew better than $55mm in dividends for the year. That’d be fine as it pays other shareholders as well, but the reality is that this company is likely to generate free cash flow this year of only $125mm.

Even though the company is not levered, it hardly seems prudent to pay up for a special dividend when you’re looking at an economically cyclical business that depends on hitting fashion trends and the company just lost leadership by way of departures in the COO and CFO ranks. Shareholders probably liked the dividend, but we can’t quite stomach it from a risk management perspective heading into an uncertain 2013.

Of course, the disconnect would be that management does not view 2013 as a year where there is risk to earnings, while we do. Therein lies our comfort level with our short case.

The near term risk to the upside is that the company is one press release away from announcing an external management hire that gets people all excited. We don’t think that one person can immediately make a big difference here – especially given that whomever is brought on will need to prove (as Carlos Alberini did) that he or she can manage both the shareholder and family agendas simultaneously, which is tough to do. But we need to at least acknowledge the risk.

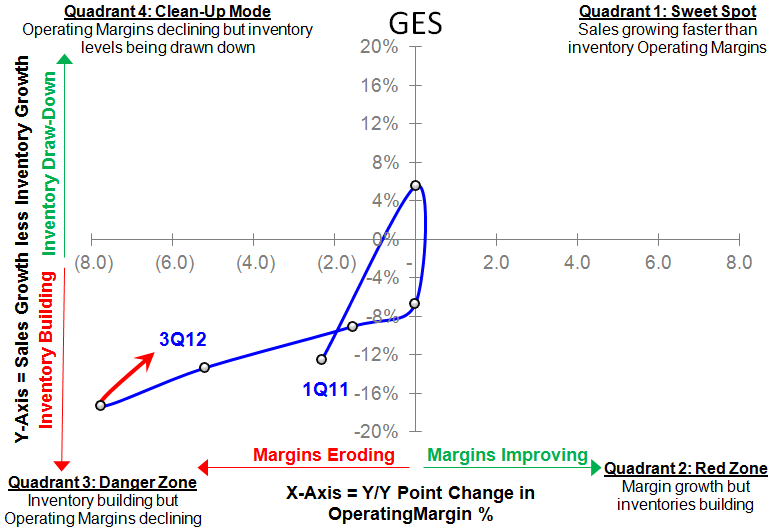

Note: As it relates to earnings, GES is currently sitting in a very bearish part of its SIGMA chart, with inventories and margins both working against the company.