TODAY’S S&P 500 SET-UP – January 9, 2013

As we look at today's setup for the S&P 500, the range is 46 points or 1.11% downside to 1441 and 2.05% upside to 1487.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.61 from 1.62

- VIX closed at 13.62 1 day percent change of -1.23%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA mortgage applications (prior -10.4%)

- 10:30am: DoE Inventory reports

- 11am: Fed to buy $1.25b-$1.75b in 2036-2042 sector

- 1pm: U.S. to sell $21b 10-yr notes reopening

GOVERNMENT:

- House, Senate not in session

- FCC Chairman Julius Genachowski speaks at CES, 4:30pm.

- Israel’s Ehud Barak visits Leon Panetta, 6:45pm

- SEC holds pre-hearing conference in matter of Deloitte Touche Tohmatsu CPAs, BDO China Dahua CPA Co., 9:30am

WHAT TO WATCH

- Clearwire gets unsolicited Dish counterbid to Sprint offer

- SAC Capital said to raise hedge fund bonuses amid probe

- AMR sees reasonable possibility of recovery for shrholders

- Goldman said to be part of Fed-led foreclosure settlement

- ITC judge may say next steps on Apple/Samsung ruling

- Blackstone said to seek doubling of credit line to $1.2b

- China-Japan dispute takes rising toll on top Asian economies

- First Quantum takes C$5.1b bid for Inmet Mining hostile

- Apple CEO returns to China amid falling phone market share

- BOJ to work more closely with Abe at regular policy meetings

- UBS client pleads guilty in offshore tax case

- U.S. shopping center demand slows amid sluggish job growth

- Shell’s mishaps in Artic drilling prompt U.S. govt. review

EARNINGS:

- Helen of Troy (HELE) 7:30am, $1.14

- Constellation Brands (STZ) 7:30am, $0.55

- Shaw Communications (SJR/B CN) 8am, C$0.46

- Pricesmart (PSMT) 4pm, $0.62

- Ruby Tuesday (RT) 4:02pm, $(0.06)

- Texas Industries (TXI) 6pm, $(0.31)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COMMODITIES – with the exception of Oil (which is a big exception as it will, at some pt, slow growth), Bernanke’s Commodity Bubble continues to deflate; Corn making a lower-low this morning and Gold is failing at its TAIL risk line of $1671 again; we covered gold so that we can re-short it on this bounce; manage the risk of the range proactively.

- Brent Crude Halts Two-Day Gain as U.S. Oil Inventories Increase

- Alcoa Sees Aluminum Use Climbing on China Recovery: Commodities

- Gold Trades Little Changed at $1,659.31 an Ounce in London

- Wheat Rises on Outlook for Lower 2013 Stockpiles; Corn Steady

- Copper Rises on Speculation About Revivals in Biggest Consumers

- Robusta Coffee Rebounds as Roasters, Investors Buy; Cocoa Falls

- Cold Weather to Aid India Wheat Crop to Record for Seventh Year

- Iron Ore Seen Set for Bear Market After Restocking Rally Fades

- Rubber Advances for Second Day as China May Step Up Purchases

- Lead Premium Paid in Europe Said to Almost Double for This Year

- EU Carbon May Decline to Record as Glut Expands: Energy Markets

- Chinese Bauxite Production Holds Key for Aluminum Markets

- China Said to Plan Sale of Government Cotton Stockpiles

- U.S. Drought Persisting Seen as Threat to Corn, Soybean Supplies

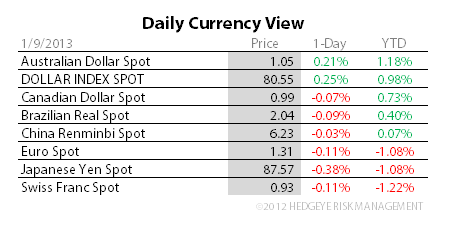

CURRENCIES

EUROPEAN MARKETS

EUROPE – the short squeeze to higher-highs in European stocks continues; Italy’s MIB Index leading the charge this wk, up another +1.1% this morning crossing the 17,000 line and making a higher-high; remember that, unlike the USA, European corporates aren’t comping all-time peak margins; most of their stock markets are cheaper on a cyclically adjusted basis too.

ASIAN MARKETS

ASIA – the Shanghai Composite corrected a whole 3 basis pts overnight and both the Nikkei and Hang Seng reversed back into the green; KOSPI down -0.3% was controlled and most importantly held both TRADE (1980) and TREND lines of support; Thailand said no more rate cuts for now as the economic demand side of the picture improves.

MIDDLE EAST

The Hedgeye Macro Team