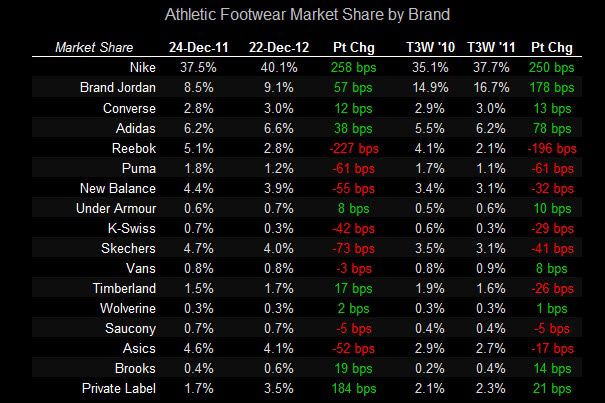

Athletic footwear clocked in another very impressive week, with low teens growth over last year for the week ending Sunday per NPD. Mind you, this comes on the heels of an impressive +35% holiday week, and also comes just as people are increasingly questioning the sustainability and longevity of the so-called ‘sneaker cycle’. Remember that sales turned down for three weeks in a row at the same time we saw Finish Line implode due to company-specific issues. That hardly helped the space.

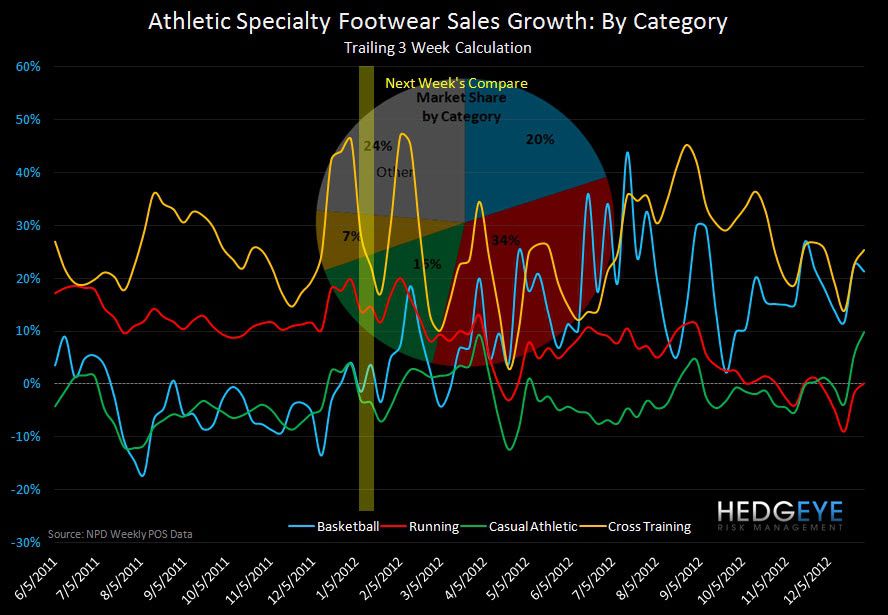

One thing we’re encouraged to see is that it is not just performance shoes carrying the day. The gap between performance and non-performance closed almost entirely last week due to a step-up in boot sales. While the performance side of the business is a better barometer for the Nike’s and Foot Locker’s of the world, we like the idea of more even-keeled sales across categories, and this week is the first time we’ve seen that since February 2011. On the margin, this is good for COLM, VFC, and DECK.