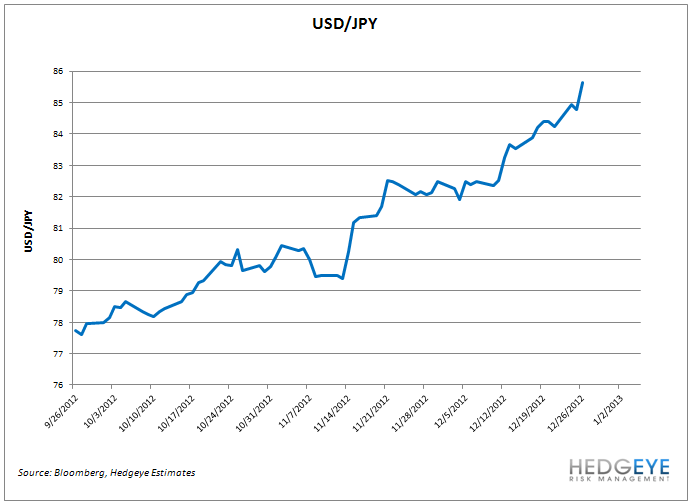

The Bank of Japan recently decided it would prefer to follow in the footsteps of the United States and the Federal Reserve. Japan's policy of debauching its currency, the yen, is part of a plan to stop its strength. As you can see in the chart below, the yen has fallen considerably over the last three months and recently hit a 27-month low against the US dollar. Japan thinks that more stimulus spending, currency printing and bailouts are the surefire way to fix the Japanese economy; if the US economy is anything to go by, that type of plan is but nothing but wishful thinking.