PCAR: Momentum Building

- Backlog to Build Ratio: We showed in our August 2012 Black Book on Truck OEMs that a low backlog to build ratio was typically a decent buy signal for the group. While the backlog to build ratio has improved since the August trough, the ratio remains very low. We continue to believe that shares of PCAR would benefit from market normalization.

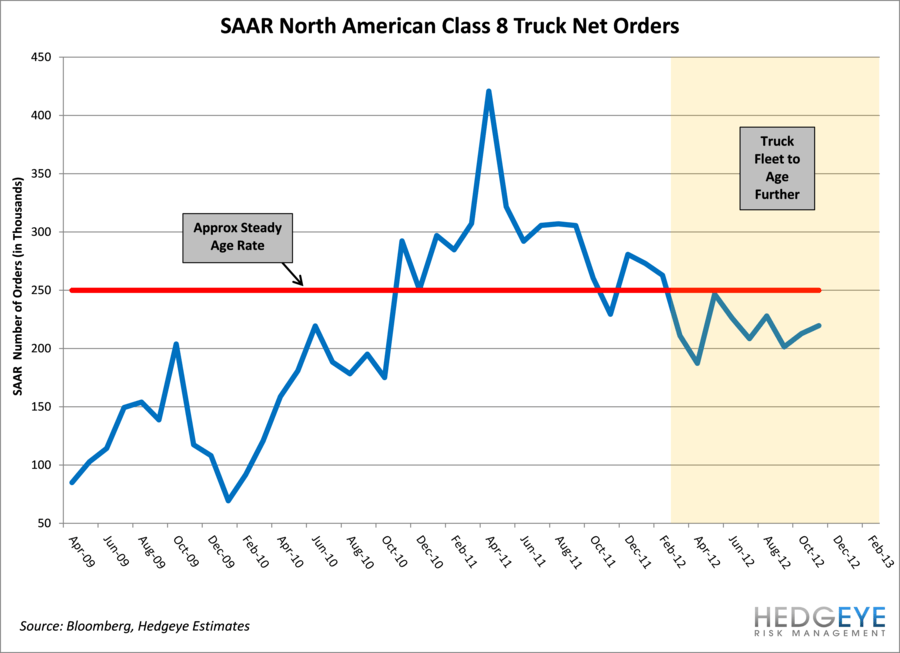

- Order Rates Below Replacement Demand: Truck owners appear to be hanging on to pre-2007 trucks because those trucks have fewer costly emission controls. Unless Class 8 trucks are leaving North American roads, order rates will need to rebound at some point.

- Navistar Share Loss: While industry metrics may still be weak relative to steady state demand, we expect PCAR and Daimler to perform better than the industry as they gain share from Navistar. Navistar has given up a huge amount of market share in Class 8. If sustained through 2013, Navistar’s loss should be a significant benefit to competitors. All else equal, share gains for PCAR could drive double digit 2013 growth in North American Class 8, PCAR’s most important market.

- PCAR a Top Long Idea: We continue to believe that PCAR is a top long idea in the Industrials sector. While the shares have outperformed since August 2012, our thesis appears to be tracking well. Near-term, PCAR should benefit from Navistar’s share loss. Longer-term, we expect a construction rebound, market entry in Brazil, a more stable truck demand environment and an aging truck fleet to benefit the firm’s bottom line.