To be clear, I said that housing would bottom in terms of sequential price declines and inventory growth in Q2 of 2009.

We are getting closer by the day!

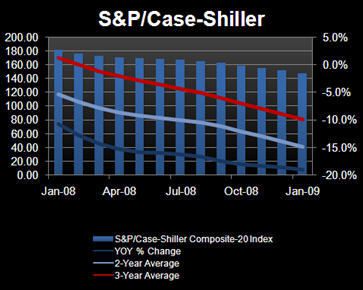

According to the S&P/Case-Shiller index, home prices in 20 U.S. cities fell -19% in January from last year. The decline was more than the -18.6% decline in December. The index has declined every month since January 2007.

There are two new incremental data points since the December S&P/Case-Shiller numbers were reported that support our call. First, while the glut of foreclosed homes will keep prices down, sales of new and previously-owned homes rose in February, indicating the housing slump could be at an inflection point. Second, Robert Shiller himself said on Bloomberg TV this morning that "the rate of decline of the rate of decline" will begin to turn shortly.

Arresting the slide in residential real estate should become the leading indicator that the worst of times is over; or at the very least, that the bottom is near. Increased confidence in the real estate asset class will allow the assets to obtain higher prices.

Howard Penney

Managing Director