“You can’t expect to have war all the time.”

-Winston Churchill

You can’t expect markets to keep going up or down all the time either. Especially in the middle of a Global Currency War, risk moves fast. So you have to keep moving out there. We call it managing the risk of the market’s range.

In addition to the aforementioned quote, in 1940, “Churchill told his War Cabinet that Roosevelt’s message came as near as possible to a declaration of war and probably as much as the President could do without Congress.” (The Last Lion, page 100)

After Paris fell to the Germans, that didn’t happen. Politically, Roosevelt wasn’t ready to commit. Militarily, America wasn’t yet ready either. Not unlike the FX War you are watching in markets today, timing and expectations matter. Ask the French.

Back to the Global Macro Grind…

After being on the sidelines (relative to the US and Europe) since 2006, the Japanese are going to engage in the FX War, big time. That’s what Abe’s LDP party win promised, but the timing of Japan’s engagement doesn’t happen all at once.

The Bank of Japan (BOJ) told the market that it will expand its bailout fund (asset purchase fund) to 76 TRILLION Yens last night (that’s a lot of Yens). But, from a market expectations perspective, that wasn’t enough to keep the Yen down!

All the while, Japan’s economy continues to head deep into the cesspool of Keynesian policy promises. Japanese Exports (it’s an export economy) were reported at -4.1% year-over-year for November. That’s right, despite their recent successes setting their currency on fire, “cheaper exports” are not reacting to the FX War Policy To Inflate.

Sound familiar?

Of course it does. Charles de Gaulle tried it. Failed. The British tried it in the 1960s. Failed. Nixon/Carter tried it in the 1970s. Failed. Japan tried it in the 1990s. Failed. Now they are all trying it, at the same time, and it’s failing.

And I mean failing from an economic perspective. Any buffoon with a money printing machine can inflate his stock market if he devalues the currency that market is priced in. Chavez devalued. The Venezuelan stock market is +305% YTD.

If the Japanese start to double and triple down on the 76 TRILLION Yens, just when the US and Europe feels safe from theirs, Japan may very well end up being the next sovereign credit crisis in 2013.

Follow the bouncy ball:

- Japan Real Estate and Stock Market Bubble implodes. Print “lots of money”, economy fails, stocks rally, fail, rally, fail.

- USA Real Estate and Stock Market Bubble implodes. Print “lots of money”, stocks rip, economy doesn’t; rally, fail.

- European Real Estate and Stock Market Bubble implodes. Print “lots of money”, yep – need to do more of that, rally!

This gargantuan experiment of Keynesian academic dogma (Bernanke calls it “innovation”) started with America advising Japan to “PRINT LOTS OF MONEY” in 1997 (Paul Krugman). So why can’t a lie that cannot live end where it started?

Every risk management exercise should start with a simple question that doesn’t have an answer (yet).

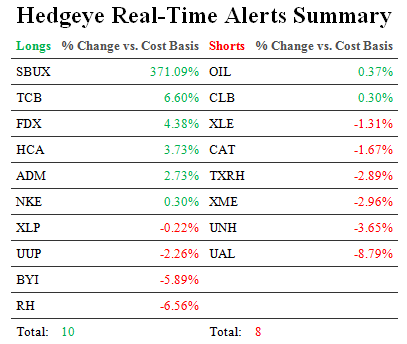

Back to our current positioning:

- Long US Consumption Stocks (bought Consumer Staples, XLP, on red yesterday)

- Short Commodities (re-shorted Oil yesterday on green)

- Out of the way on Fixed Income (cut our asset allocation to 0% last week)

Now maybe buying anything that’s been propped up by Policies To Inflate doesn’t make sense. Once every asset class that hasn’t been locked down (stocks, bonds, commodities) has been artificially inflated, isn’t the only risk that remains deflation?

Probably not. That’s the whole point about the FX War – you can’t have deflation all of the time. Ask the government.

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1, $105.95-110.02, 3.57-3.62, $79.15-79.91, $1.31-1.33, 1.73-1.85%, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer