Labor Market: Surprisingly Strong

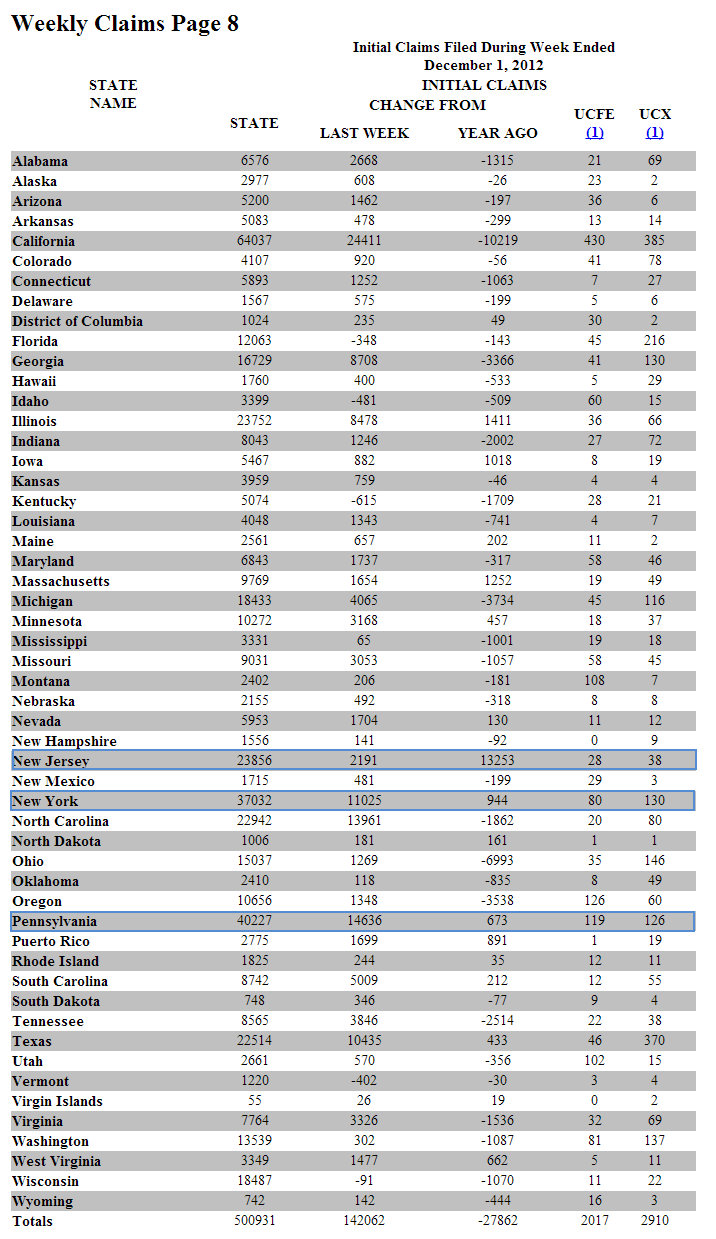

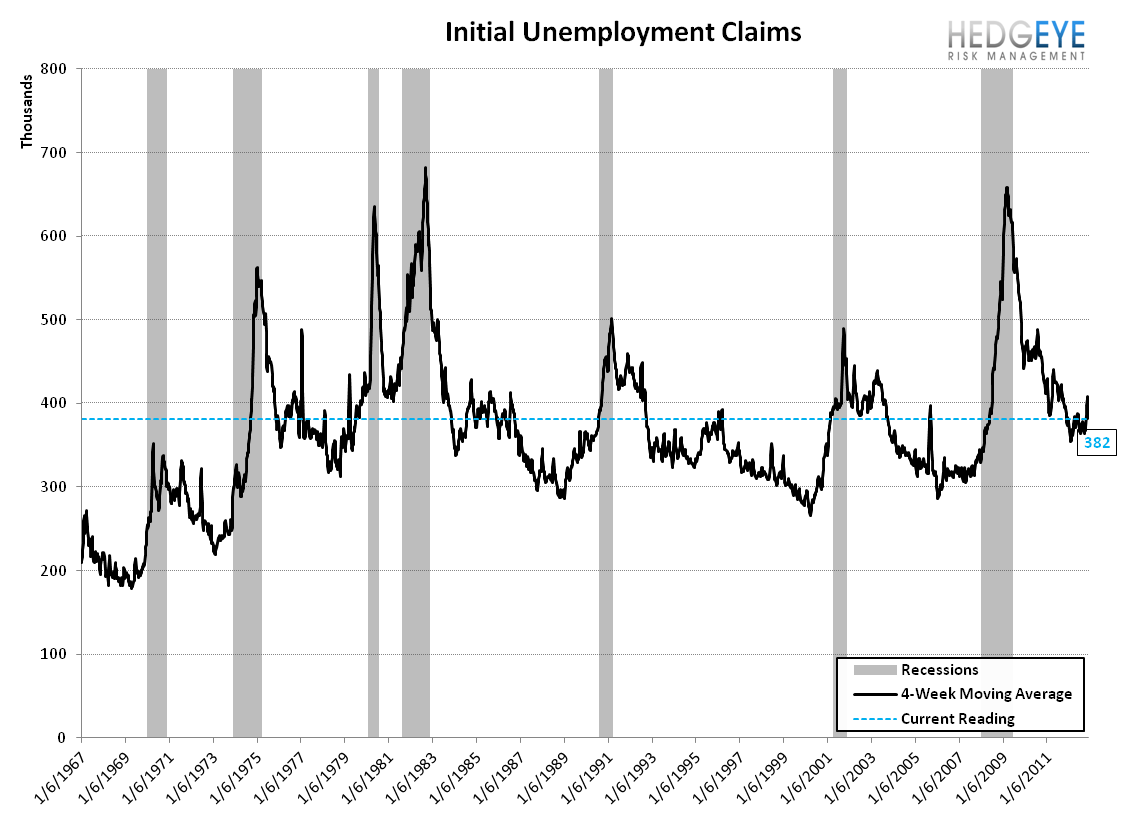

Last week was another surprisingly strong week of improvement for initial jobless claims. As we've been doing the last few weeks, we again ran the analysis to see whether over-representation by NY, NJ and PA is distorting the numbers. As a reminder, state-level data is released on a one-week lag vs. national data. As of two weeks ago, when national claims were 370k, NY, NJ and PA were still being over-represented in the series by 7.1% vs their normal proportional weightings. This suggests that the normalized run-rate in claims is actually 370 / 1.071 = 345k. Interestingly, that's almost exactly what we saw this week: 343k.

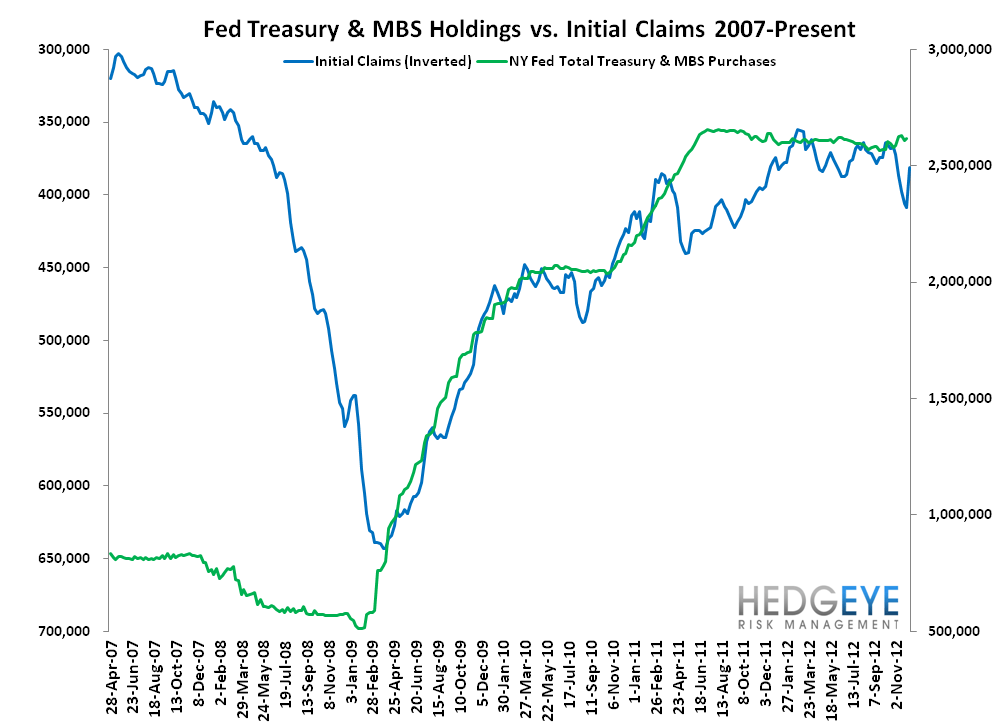

This week's claims print of 343k is significant for a few reasons. Foremost, it matters because it represents a new low in claims post the crisis. Second, it matters because it returns claims to the seasonal trajectory we've seen over the last three years. In other words, the seasonality mal-adjustment tailwind we've often called out is back in full effect, and will continue, as a reminder, through February. So, to reiterate, the jobs data is improving, but the perception of the rate of improvement will be stronger than the underlying reality for the next two and a half months. This, coupled with momentum in the housing market, will provide a strong, ongoing tailwind to the sector.

Jobless Claims - The Numbers

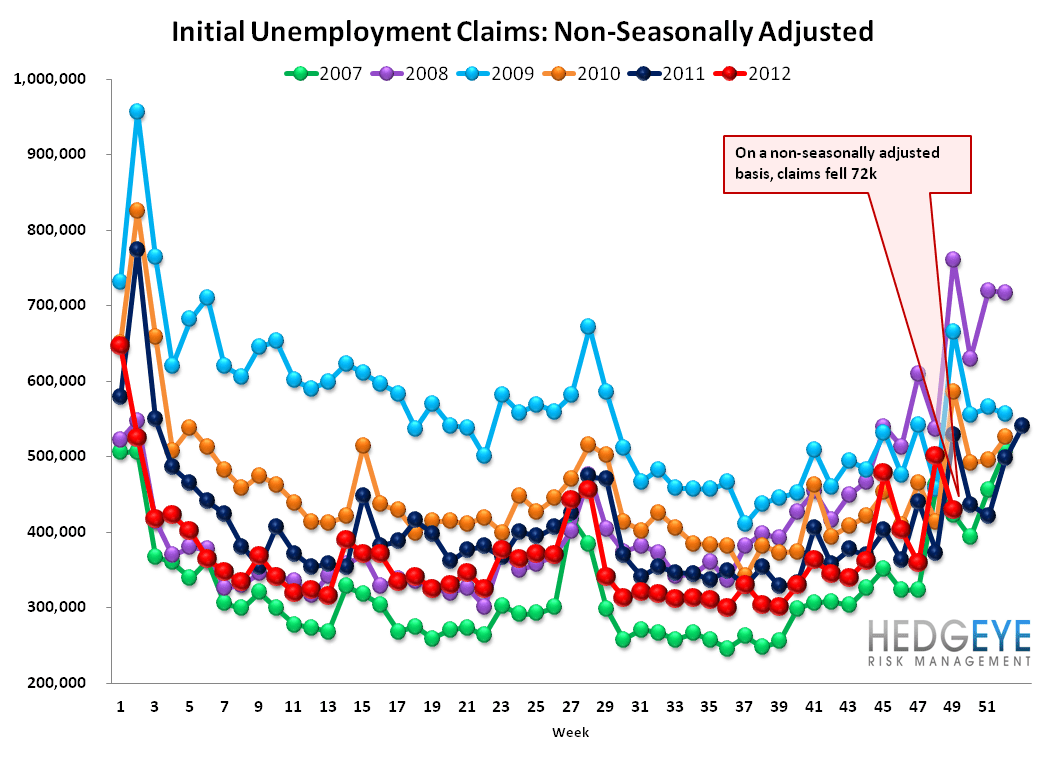

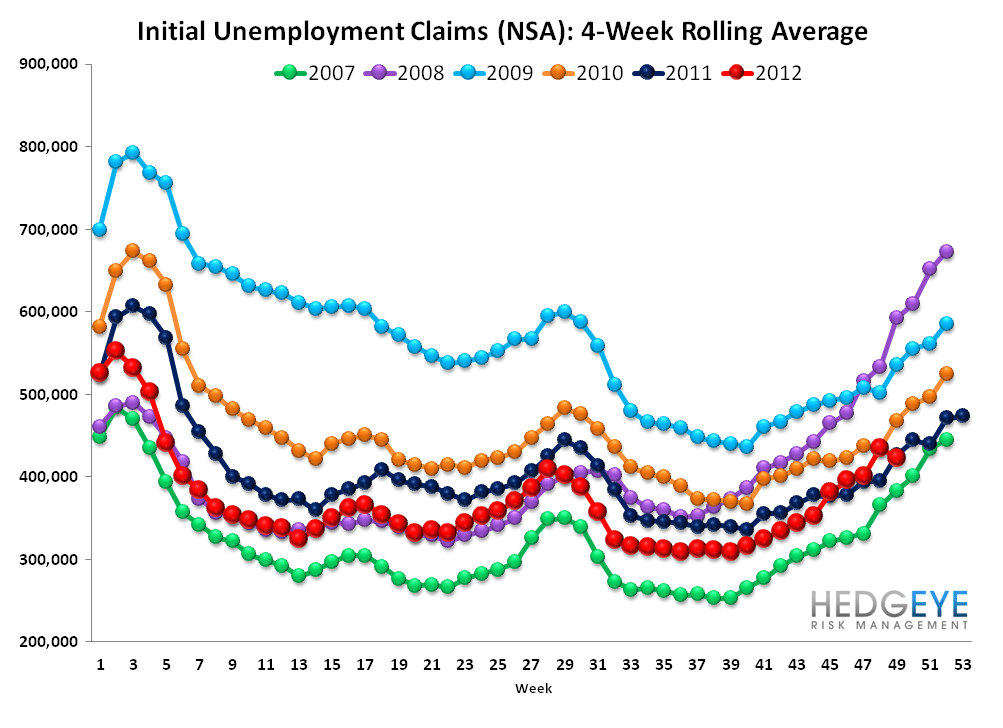

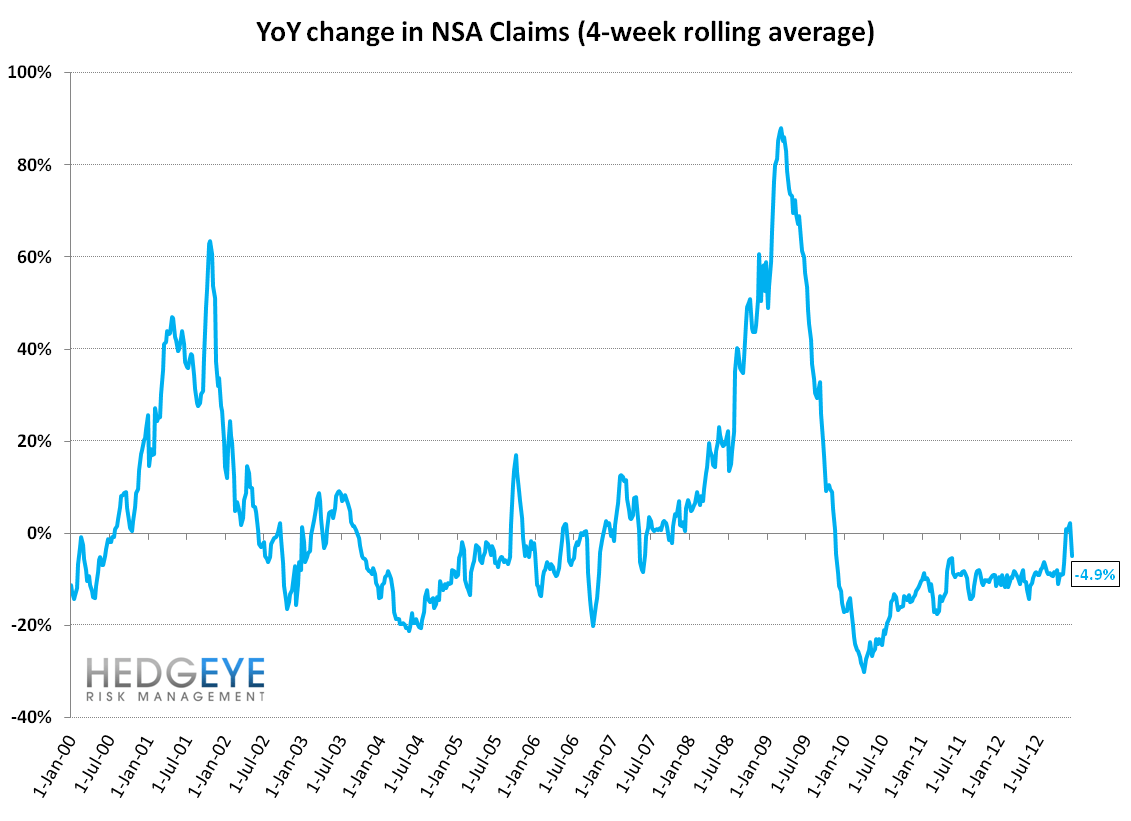

This week initial jobless claims fell 27k to 343k from 370k. The prior week's number was revised up by 2k to 372k. Incorporating this upward revision, claims were lower by 29k. Rolling claims, meanwhile, fell 27k WoW to 381.5k and non-seasonally adjusted claims fell 72k to 429k. Additionally, the NSA rolling year-over-year change, which we monitor because it excludes the effects of seasonality, was -4.9% YoY, down from +2.1% in the prior week.

September SNAP: Another 608k People on Food Stamps

While the trend in joblessness is improving, the number of people receiving government assistance to buy food in the U.S. continues to rise. In September, SNAP participation reached 47,7101,324, or 15.3% of the population. In terms of households, there are roughly 23 million households receiving assistance, or about 20% of all U.S households. In September, an additional 608k people joined the program. The number of people on food stamps has risen 79% since June of 2007.

If there's any silver lining here its that the rate of growth in the program has been slowing. In the first chart below, we show the total number of participants in the blue grey columns and the year-over-year rate of change in the black line. The current growth rate is 3.1% year-over-year. which is down from the 5.1% year-over-year growth rate we were seeing at the beginning of this year.

Yield Spreads

The 2-10 spread rose 10 basis points WoW to 145 bps. 4QTD, the 2-10 spread is averaging 141 bps, which is higher by 4 bps relative to 3Q12.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over multiple durations.

Joshua Steiner, CFA

Robert Belsky