TODAY’S S&P 500 SET-UP – December 7, 2012

The S&P 500 closed yesterday at 1,413.94 an increase from the prior day's trading of 33bps.

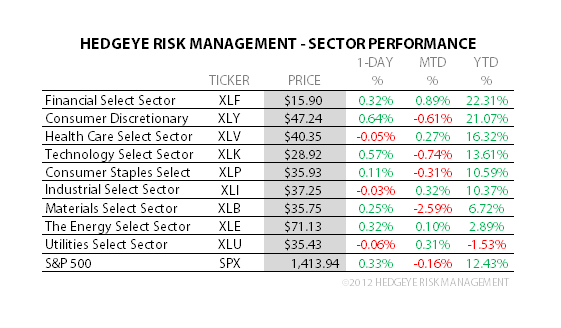

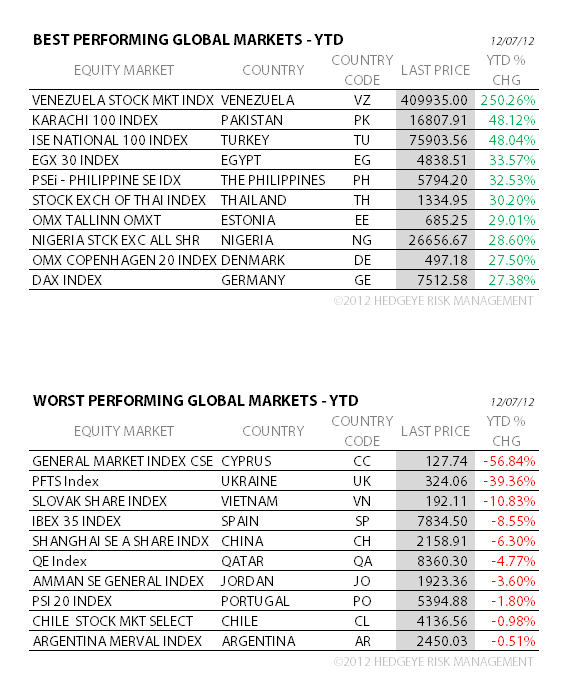

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.34 from 1.35

- VIX closed at 16.58 1 day percent change of 0.73%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Change in Nonfarm Payrolls, Nov. est. 86k (prior 171k)

- 8:30am: Unemployment Rate, Nov. est. 7.9% (prior 7.9%)

- 9:55am: UMichigan Confidence, Dec. P est. 82.0 (prior 82.7)

- 1pm: Baker Hughes rig count

- 3pm: Consumer Credit, Oct. est. $10.0b (prior $11.365b)

GOVERNMENT:

- Romney, Obama, allies spent more than $2b in campaign

- House meets in pro forma session. Senate not in session

WHAT TO WATCH

- Sandy probably dealt blow to U.S. labor market in November

- Japan reports little damage after 7.3-magnitude quake hits

- Samsung asks judge to reject Apple’s request for smartphone ban

- AT&T, Verizon to allow text-message 911 services

- Dodd-Frank rules governing derivatives may be delayed from implementation for 6 months

- Netflix, CEO receive Wells notices from SEC

- JPMorgan investment banking bonus pool said to contract by as much as 2% from year ago

- Pfizer’s Inlyta fails to win approval by U.K.’s health cost regulator

- Ford Hybrids don’t meet gas mileage target of 47mpg as set by automaker, Consumer Reports says

EARNINGS:

- Bank of Nova Scotia (BNS CN) 7:30am, C$1.19

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Copper Steady in London, New York Before U.S. Employment Data

- Gold Bulls Retreat as Goldman Sees Peak Next Year: Commodities

- Rebar Has Biggest Weekly Gain in Two Years on Improving Demand

- Oil Heads for First Weekly Drop in Five on German Growth Cut

- Bins Bulge With Grain as Low Water Threatens Mississippi Traffic

- Soybeans Approach Biggest Weekly Gain Since August on Exports

- Gold Extends Weekly Decline as a Stronger Dollar Curbs Demand

- Palm Oil Shipments From Indonesia Seen Falling to Five-Month Low

- Fracking-Study Conflicts Prompt Head of Texas Institute to Quit

- Chicken-Feet Exports Help Savannah Top U.S. Port Growth: Freight

- Swollen Lakes Mean Five-Year Low Nordic Power: Energy Markets

- Europe Copper Premium Said to Drop Over Month on Weaker Demand

- Storm Heads Toward China, Vietnam as Philippine Death Toll Rises

- Copper Gains in London Before China’s Production: LME Preview

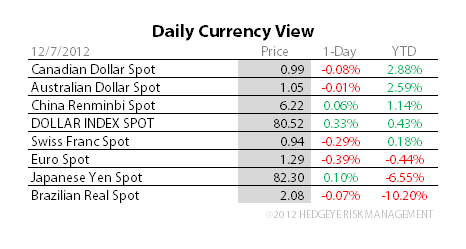

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

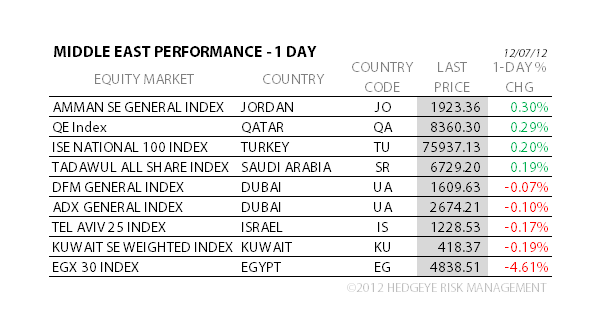

MIDDLE EAST

The Hedgeye Macro Team