“History rouses man to emulate the deeds of earlier generations.”

-Ludvig von Mises

This weekend I forced myself to watch the Sunday morning US political talk shows. While it was sad to watch, it did inspire some leadership thoughts. One was on class warfare. The only two classes I see developing are The Political Class and The Rest Of Us.

Politics is a big business. And I have never been more proud to be neither a Bush Republican nor an Obama Democrat. On economic matters, both parties are Keynesian now. Unlike the Austrian school (center right), Keynesians are center-left. There is no center.

There’s also the left of center-left (Paul Krugman). And these guys are really amping up the Marxist (way left) rhetoric. If you don’t agree with that, read Krugman’s Sunday piece in the New York Times titled “Class Wars of 2012.” #Scary.

Back to the Global Macro Grind…

In his preface to Classical Liberalism and The Austrian School, David Gordon recently wrote that, “Ideas do not, as Marxists imagine, reflect the interests of conflicting economic classes. The free market rests, not on irreparable class conflict, but on fundamental harmony of interests of people who benefit from social cooperation.”

I liked that. It’s progressive and collaborative as opposed to regressive and polarizing. On that score, the latter most definitely applies to our generational debate about the #KeynesianCliff. As far as I can see, the cliff debate has 3 big parts:

- DEBT

- SPENDING

- TAXES

This weekend, the left side of the Political Class was focused on 1 of the 3 (TAXES). Meanwhile, this is what Gene Sperling (Director of Obama’s National Economic Council) is actually asking for (he did the interview with Bloomberg TV this weekend):

- “a long-term extension of the legal debt limit”

- “some stimulus measures to support the economy”

- “a tax rate increase for the wealthy”

Got it on point #3 guys – you want to tax us. But what about points 1 and 2? Did some Democrats vote for social issues (that most Independents and socially liberal Republicans agree with), or did they vote for raising the US Debt and Spending levels? Or both?

The Political Class can obfuscate and demagogue all they want about this, but I am pretty sure that The Rest Of Us want to see an arrest of government debt and spending increases, not another moving of the #DebtCeiling goal posts and “stimulus” spending.

Back to the government’s math. In last week’s peculiar (but less than ironically inflated) pre-Election US GDP report of +2.67%:

- GOVERNMENT SPENDING contributed positively to “growth” for the 1st time in 9 quarters!

- At +0.67% in GOVERNMENT (G) contribution (versus -0.14%, -0.60%, and -0.43% in the last 3 quarters), spending is back!

- INVENTORIES contributed the rest of the positive delta, going from -0.46% in Q212 to +0.77% in Q312

Our GDP forecasting model (it’s a predictive tracking algo) couldn’t front run that. Government Spending (+0.67%) and an out of nowhere Inventory build (+0.77%) = 54% of US GDP “growth” in Q3 whereas the C (Consumption) in C +I + G + (EX-IM) = GDP fell to +0.99%. Consumption is 71% of the economy or, put another way, The Rest Of US, too.

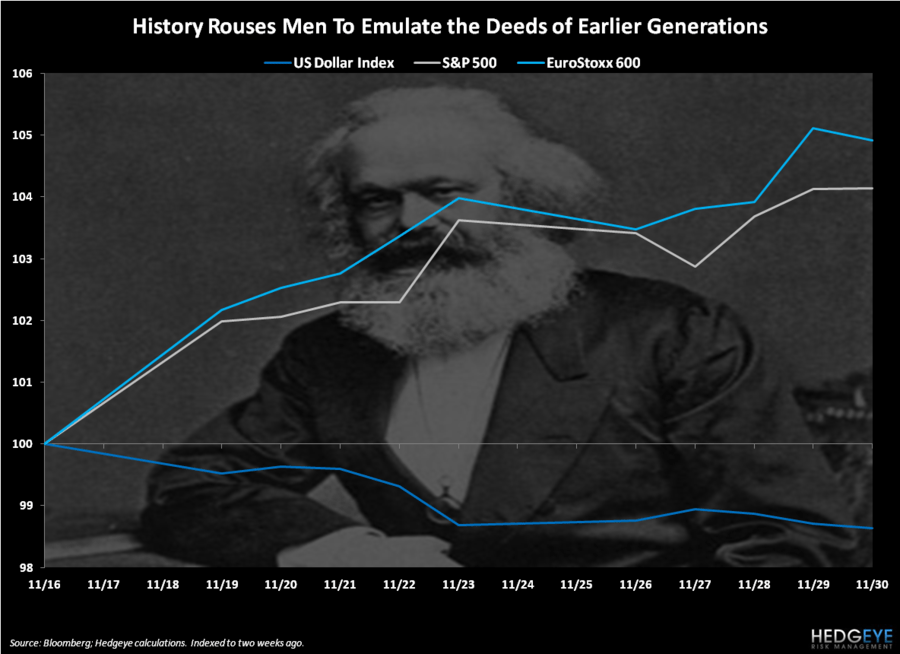

All the while, last week global currency investors took USA looking more and more like Italy on debt and spending and sold down the US Dollar for the 2nd consecutive week. Both European and US stocks liked that – they were both up for the 2nd consecutive week at +0.5% and +0.9% for the SP500 and EuroStoxx600 indices, respectively.

Centrally planned stock markets, however, are not the economy. What investors and day traders alike have been trained to do is play the Dollar Debauchery trade that’s in front of them. With the US Dollar under Geithner policy pressure:

- CFTC Futures/Options net long contracts jumped +9.8% wk-over-wk (best weekly gain in net long spec since August)

- Gold and Silver net long contracts jumped +13% and 12%, respectively (wk-over-wk)

- Wheat contracts spiked +35% wk-over-wk

But, if you don’t think rising government DEBT and SPENDING is causal to blowing up the credibility of a country’s currency, you probably think I am just telling you stories this morning.

Sadly, the growing number of class warfare demagogues out there who are emulating the “deeds of earlier generations” are starting to story-tell like Karl Marx did too.

Our immediate-term Risk Ranges (support and resistance) for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1, $110.07-111.58, $3.54-3.65, $79.81-80.36, $1.29-1.31, 1.58-1.67%, and 1, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer