JACK reported 4QFY12 EPS last night. The current climate is challenging for all restaurant operators but we remain confident in our tail thesis on Jack in the Box. We would highlight the gulf between consensus estimates for JACK revenue and the result last night as indicative of the risk there is in consensus estimates for this company. We think the headlines, which were largely misrepresentative of the reality of Jack in the Box’s 4QFY12 results, caused the sharp sell off after hours. We continue to see upside in this name to $40 over the next three years. Here is a quick run-through of what we will be focusing on during the earnings call at 11:30 ET.

Revenue:

- JIB SRS were a big upside surprise, will be interesting to hear on the call if marketing was ramped up significantly for the September quarter

- 2-year SRS trends accelerated for to 4.5% and 2.7%, for company and franchised JIB restaurants

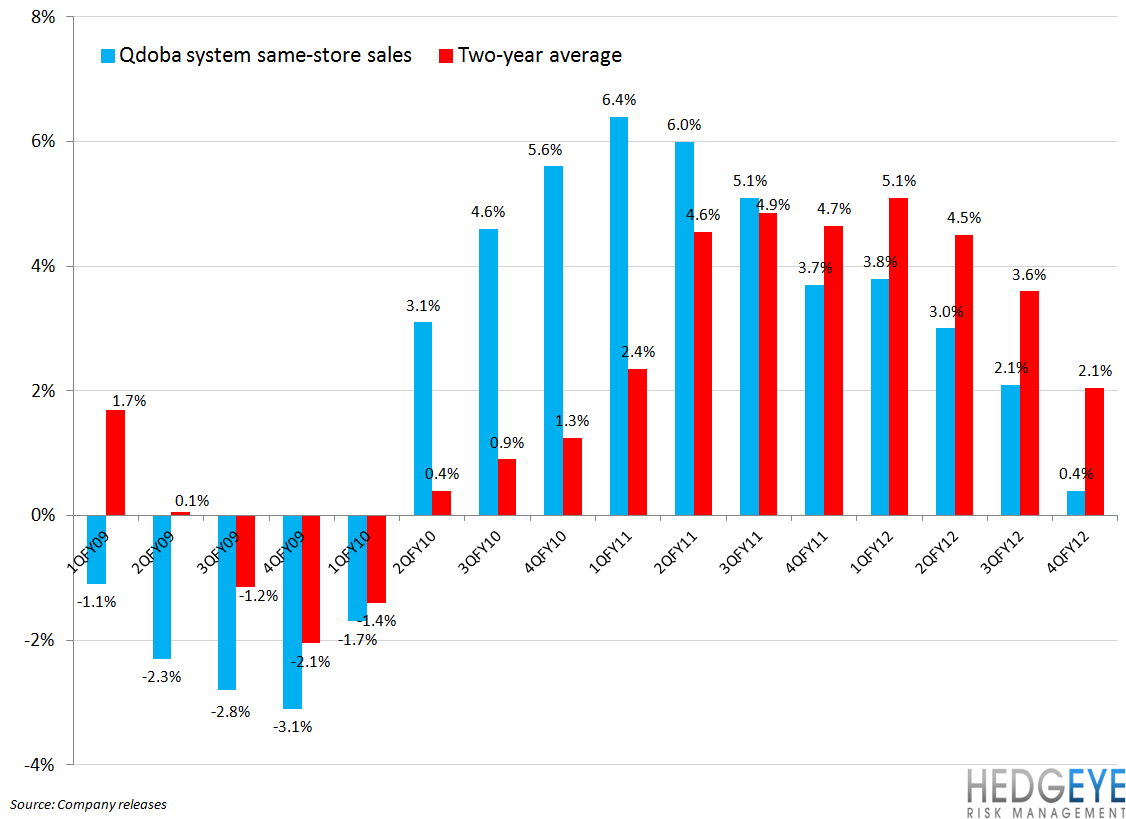

- Qdoba a big downside surprise at 0.8% and two-years trends slowing to 2.3%. Gary Breisler, President of Qdoba, left intra-quarter

- We will want to pay attention to growth expectations for Qdoba. If SRS trends remain at current levels it could lead to some growth being postponed

Margins:

- Cost of sales were higher than expected. I suspect that we will get a look into FY 2013 commentary on beef outlook on the call

- Labor costs were lighter than we modeled, due to lower labor trends at JIB. How sustainable is this and can we see more of this in FY2013.

- G&A a bit heavy once again. G&A has been trending higher for all of FY2012. Why?

Guidance issued for FY13:

- 1QFY13 SRS 1-2% at JIB co-op and Qdoba co-op.

- FY SRS at JIB co-op 2-3% (we think this is conservative guidance)

- FY SRS at Qdoba co-op 2-3% (we believe management is being cautious and will seek to prove Qdoba margin story in FY13)

- 1Q13 SRS seem to be below the current street expectations.

- Commodity costs up 2-3% (refranchising a good move but franchisees will feel burden of beef costs)

- Company will no longer provide guidance for refranchising gains as results will become cleaner

Howard Penney

Managing Director

Rory Green

Analyst